Hopes for a big rate cut at the upcoming FOMC meeting took a hit after today’s data releases. To be sure, the game is arguably not over as we still have tomorrow’s employment report ahead of us. Realistically though it is not likely to be sufficiently weak to drive the Fed to a 50bp cut. And, considering sentiment, there is arguably a case to be made that a sufficiently strong report would cast doubt on any rate cut at all.

In contrast to the soft manufacturing ISM report, its service sector cousin was more upbeat. The index rose more than expected on the back of strong gains in the new orders and activity components. The employment component fell but remains above 50. It looks like the service sector of the economy is diverging from the manufacturing side of the economy much as we saw in 2015-16:

To be sure, that story could change. Still, it continues to be that case that the global growth and trade shocks are primarily striking the manufacturing side of the economy. That side of the economy may now be too small to easily transmit recessionary shocks to the rest of the economy. And if these shocks are not sufficient to generate a recession, then the Fed will not be taking rates back to zero anytime soon.

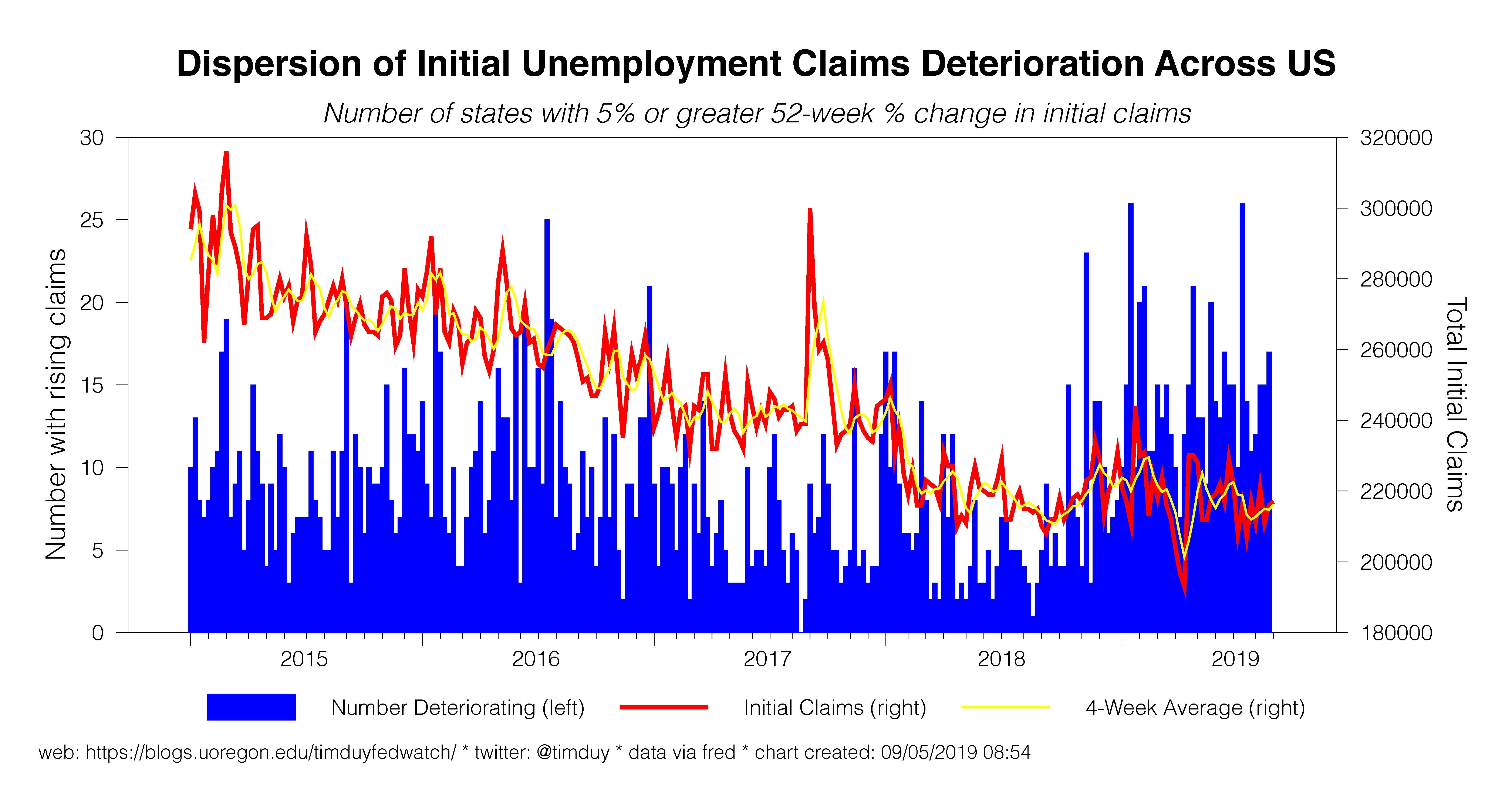

Initial unemployment claims continue to move sideways:

while ADP reported that the private sector added 195k jobs in August. My estimate for job growth is 155k, basically the same as the consensus of 158k:

Two notes of caution though. First, the headline might be higher than expected due to Census hiring, so adjust accordingly. Second, August might be revised upward. See Calculated Risk on both topics.

As of this moment, CME reports odds of 95.8% that the Fed cuts rate 25bp while a 4.2% chance that they hold steady. Earlier in the week the choice was cut 25bp or 50bp but flipped on today’s data. It is reasonable to believe that a solid employment report with upward revisions to August further raises the odds of no cut this month.

I believe the Fed will cut 25bp even if the employment picture remains bright. The risks to the outlook remain, business investment has not yet rebounded, upcoming revisions to employment data indicate the economy had less momentum than believed, market participants anticipate further easing, and another rate cut would help address the yield curve inversion. Still, ongoing upside surprises to the data would encourage the Fed to take a more hawkish stance beyond this next meeting.

Bottom Line: Fed will likely cut 25bp this month. The data is not screaming for 50bp. Some might argue that it is not screaming for 25bp either, but it still looks like cheap insurance against the possibility that watching the data now is too much of an exercise of driving through the rear view window.