Jackson Hole came and went with little reason to believe the Federal Reserve will do anything other than raise interest rates in September and again in December of this year.

Bloomberg has a quick rundown of the action here. My quick summary to start the week is that the Fed potentially has two big decisions ahead of it in the upcoming months. The first is whether or not to deliberately invert the yield curve – already nearly flat with a 10-2 spread of just 20 basis points as of Sunday night. The battle lines on this issue are already well defined. Some, like St. Louis Federal Reserve President James Bullard see an inverted yield curve as a fairly clear warning of recession (via Reuters), while others like Cleveland Federal Reserve President Loretta Mester tends to fall into the “it’s different this time” camp.

Last week Atlanta Federal Reserve President Raphael Bostic appeared to take a firm stand on the issue, claiming that he would not vote for any policy action that would “knowingly” invert the yield curve. Apparently he thought that with that comment he was writing a check he couldn’t cash because he quickly followed up with a blog post on the topic in which he chooses his words more carefully:

I believe the yield curve gives us important and useful information about market participants’ forecasts. But it is only one signal among many that we use for the complex task of forecasting growth in the U.S. economy. As the economy evolves, I will be assessing the response of the yield curve to incoming data and policy decisions along the lines I’ve laid out here, incorporating market signals along with a constellation of other information to achieve the FOMC’s dual objectives of price stability and maximum employment.

This is where I think most central bankers will find themselves if the yield curve inverts in the near future. Absent a financial crisis, a 10-2 inversion would most likely happen well before a business cycle peak. It will be just one out of a “constellation of other information” that will look fairly solid if not downright frothy. It would be hard for the Fed to ignore everything else in favor of the yield curve.

The second issue facing the Fed is to pause or not when the Fed reaches estimates of the neutral interest rate. The idea is that once they hit neutral, they should assess the impact of past rate hikes before moving toward a restrictive policy stance.

Interestingly, the question of a pause at neutral is not unrelated to the first debate. Given the median policy maker estimate of the neutral rate is 2.9% and the 10 year Treasury is hovering around 3%, a neutral policy stance implies a flat yield curve. So pushing past current estimate of neutral would be inverting the yield curve unless long rates suddenly begin to move higher (think quantitative tightening, fiscal deficits, rising term premium).

Powell’s contribution to the Jackson Hole conference did not give much guidance on this point. He basic point was that central bankers should not take estimates of such policy metrics as the neutral interest rate too seriously. Policy needs to be based on good analysis but also good judgement. My takeaway is that he isn’t putting much faith into the Fed’s estimates of the neutral rate. If they get to those estimates and the job market continues to churn away, Powell & Co. might reasonably conclude that their neutral rate estimate is too low – just as they concluded that their initial estimates of the natural rate of unemployment was too high.

That said, I think a reasonable baseline remains that the Fed hikes rates three maybe four more times and then the data gives them reason to pause. But if the data doesn’t give them reason, they will be hard pressed to pause simply because they have reached their estimates of neutral.

Speaking of data, manufacturing activity keeps cranking away according to the industrial production report and manufacturer’s survey:

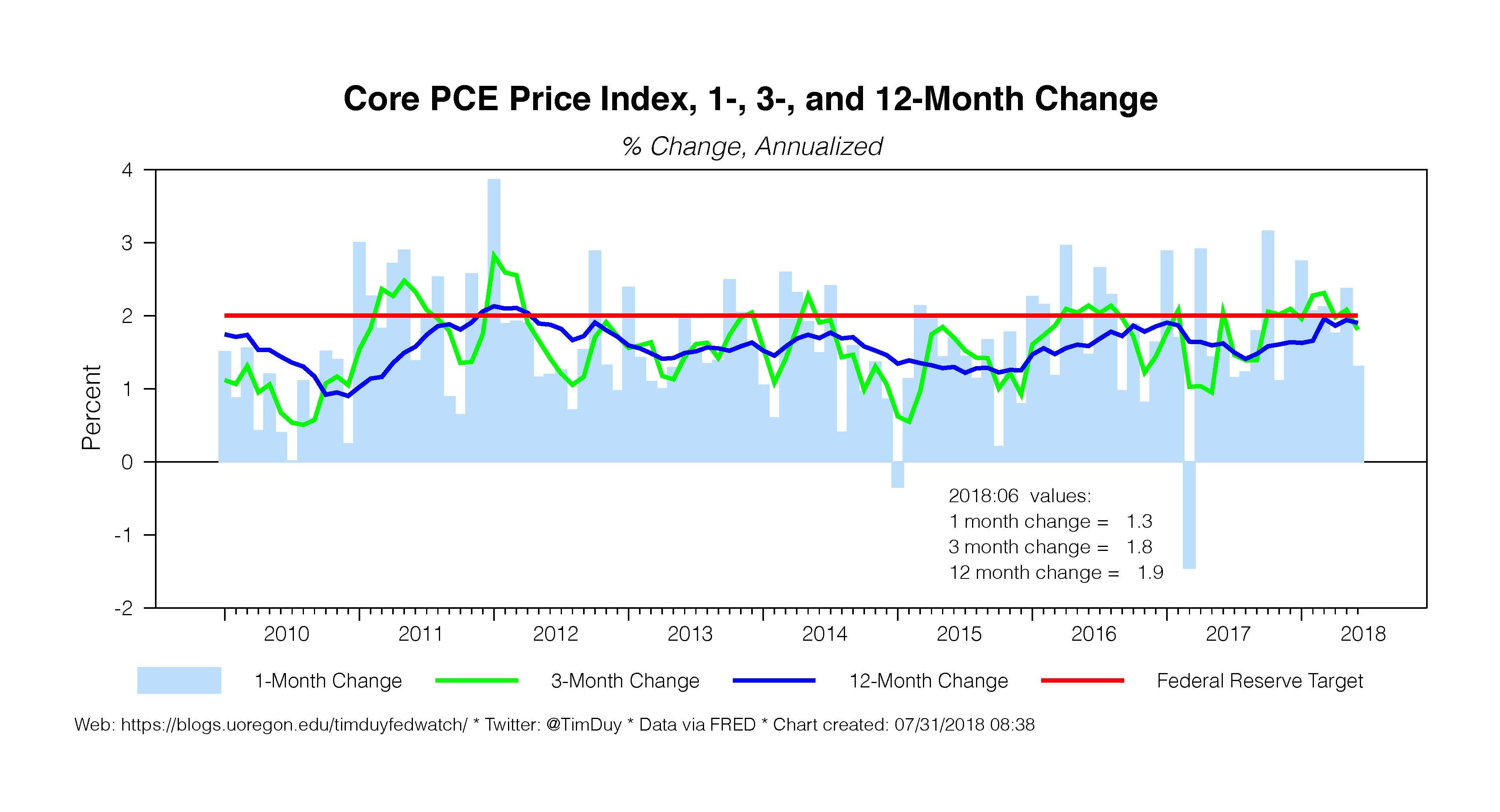

The Atlanta Fed currently estimates third quarter growth at a whopping 4.6%. To be sure, it is still early, but it is hard to see the Fed stopping if the numbers are even well below that at say 3%. Look this week for personal income and outlays report with its read on consumer spending and of course inflation.

The Atlanta Fed currently estimates third quarter growth at a whopping 4.6%. To be sure, it is still early, but it is hard to see the Fed stopping if the numbers are even well below that at say 3%. Look this week for personal income and outlays report with its read on consumer spending and of course inflation.

Bottom Line: The rates hikes keep coming. It is hard for me to argue that December isn’t pretty much already a lock, as is of course a rate hike next month.