Click here for newsletter!

Thursday’s data told a familiar story – the US economy continues to chug along at a solid pace while inflation remains quiescent. This provides room for the Fed to continue their march toward a neutral rate, but little reason to push beyond that rate without careful thought. That said, at least one key policy maker has eyes set on exceeding the neutral rate, even at the expense of inverting the yield curve.

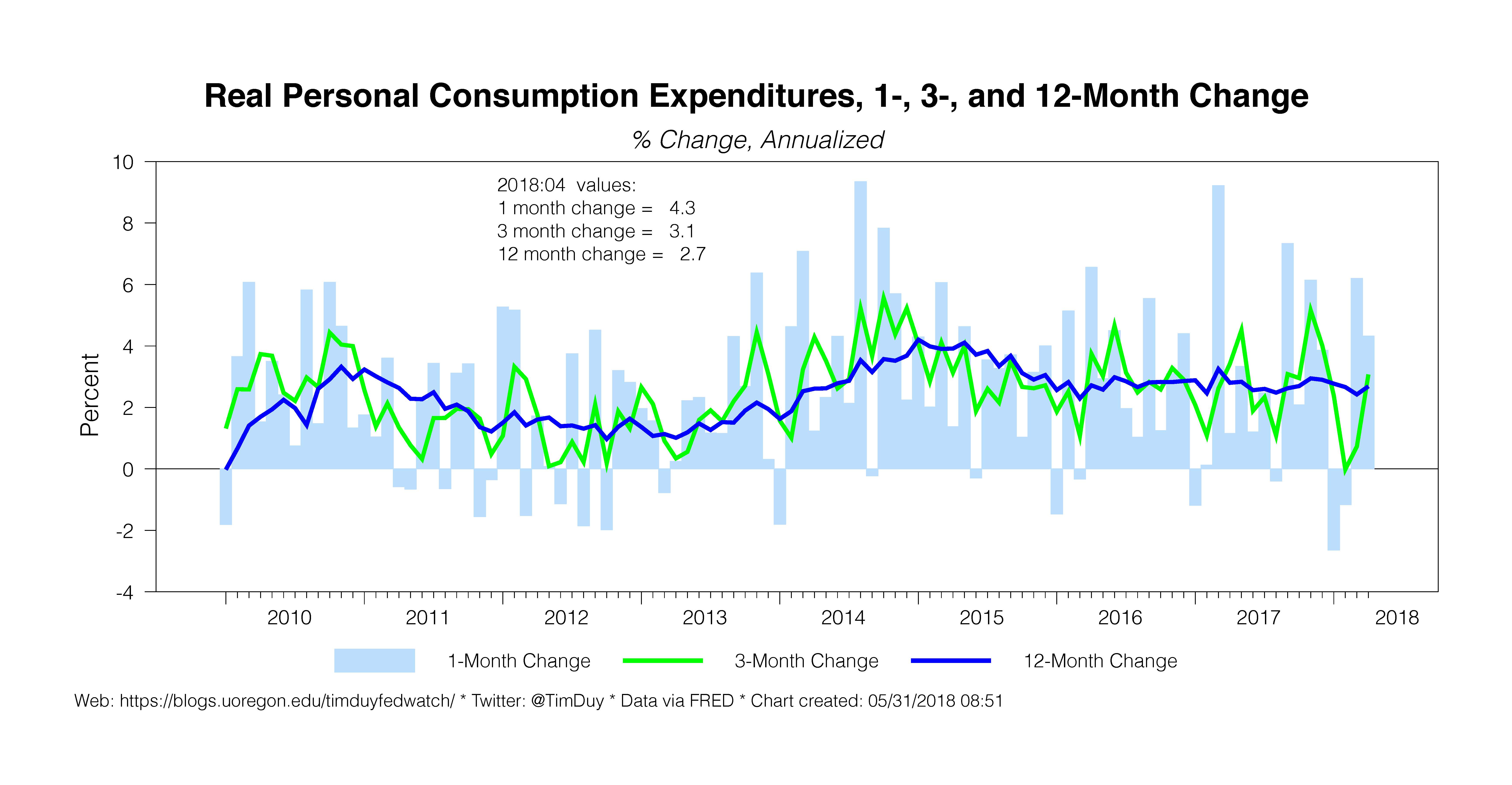

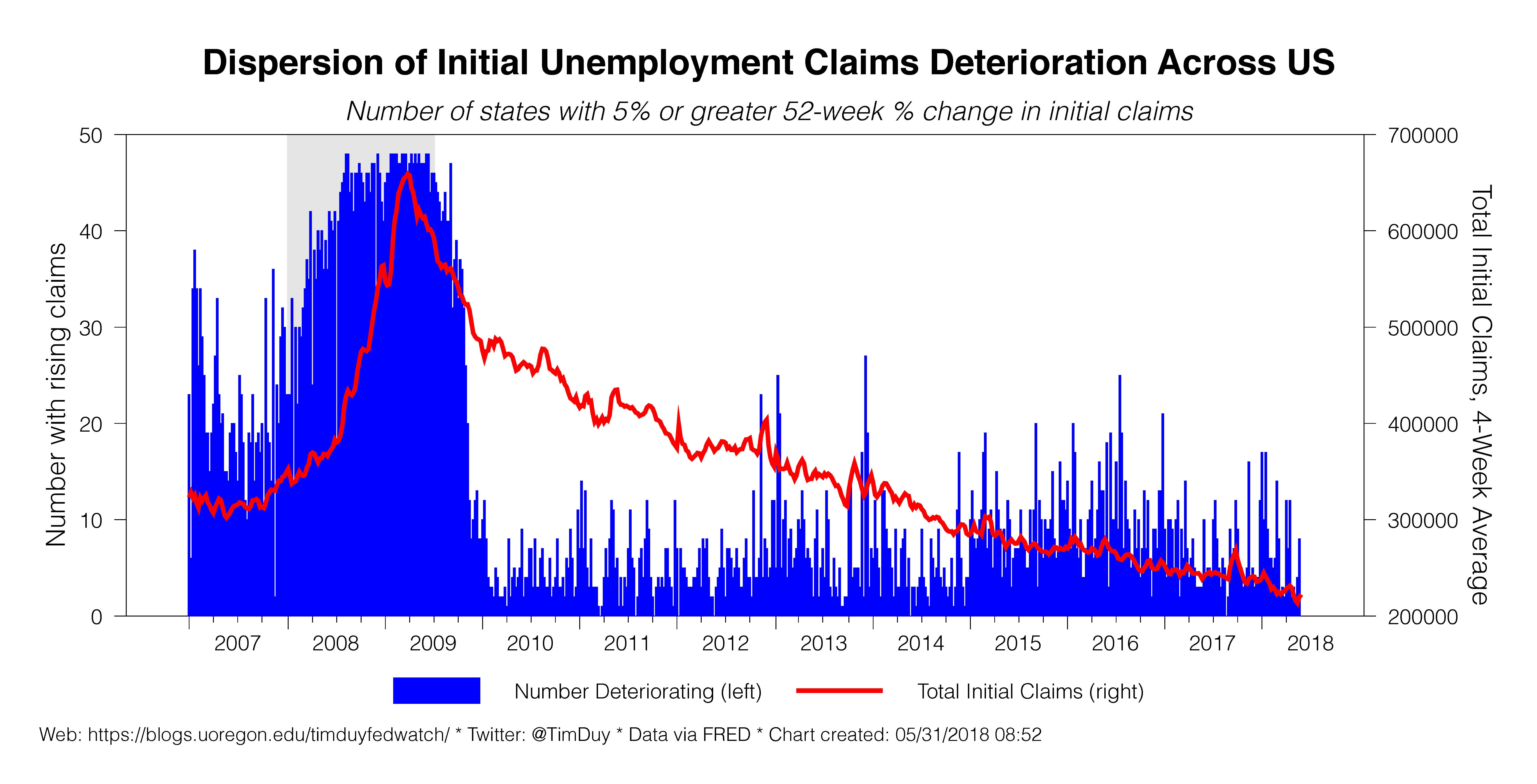

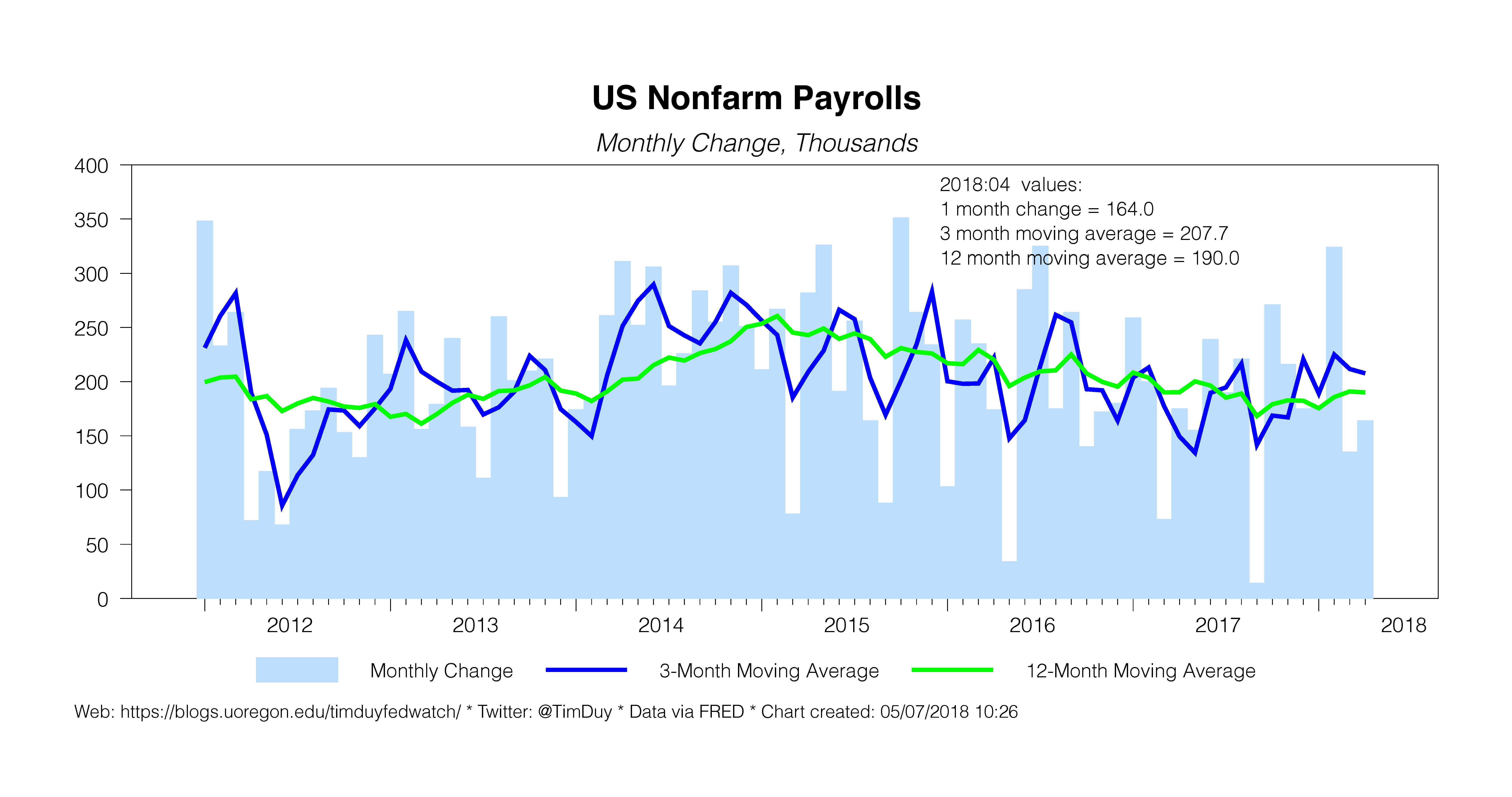

Consuming spending bounced back in the second quarter from a weak showing earlier in the year. The underlying trends remind us to remain wary of reading too much into the monthly or quarterly volatility. Real spending has been growing at a fairly steady pace of 2.5-3.0% for over two years now; any fears of a consumer slowdown continue to prove unfounded. That story probably won’t change until the labor market drops into a lower gear. We get a fresh employment report Friday morning; until then, we can take comfort in the initial claims numbers, which show no signs that the labor market has hit a wall.

Inflation appears to be firming around the Fed’s 2% target with the annualized one, three and twelve-month changes sitting at 1.9%, 2.0%, and 1.8%, respectively. The larger monthly gains of January and February have waned in subsequent months, leaving little worry that inflation will soon overshoot the Fed’s target. And even some overshooting won’t cause Powell & Co. to panic as they will tolerate inflation numbers modestly above target. My thinking is that they will let inflation drift as high at 2.5% as long as they can reasonably forecast a return to target assuming current rate projections. But if it looks like inflation is rising to that level on a sustained basis, they will step up the pace of rate hikes.  Friday morning we also get a read on the manufacturing sector with the ISM report. That number should be solid, following the trend of recent regional reports. For example, Thursday’s Chicago PMI number for May came in above expectations. Of course, the ongoing trade frictions pose a risk for the manufacturing sector. Today the U.S. implemented steel tariffs on key allies; this kind of action will like disrupt already tight supply chains and, more importantly, creates uncertainty by setting the U.S. against the rest of the world.

Friday morning we also get a read on the manufacturing sector with the ISM report. That number should be solid, following the trend of recent regional reports. For example, Thursday’s Chicago PMI number for May came in above expectations. Of course, the ongoing trade frictions pose a risk for the manufacturing sector. Today the U.S. implemented steel tariffs on key allies; this kind of action will like disrupt already tight supply chains and, more importantly, creates uncertainty by setting the U.S. against the rest of the world.

Federal Reserve Governor Lael Brainard reads the tea leaves in this speech and concludes that further gradual rate hikes remains the appropriate policy path”

This outlook suggests a policy path that moves gradually from modestly accommodative today to neutral–and, after some time, modestly beyond neutral–against the backdrop of a longer-run neutral rate that is likely to remain low by historical standards.

Brainard does identify some fresh downside risks to the outlook – divergent monetary policy across major economies, an emerging markets pull back, and global trade tensions – these are still just risks. Moreover, they are offset by upside risks from fiscal policy.

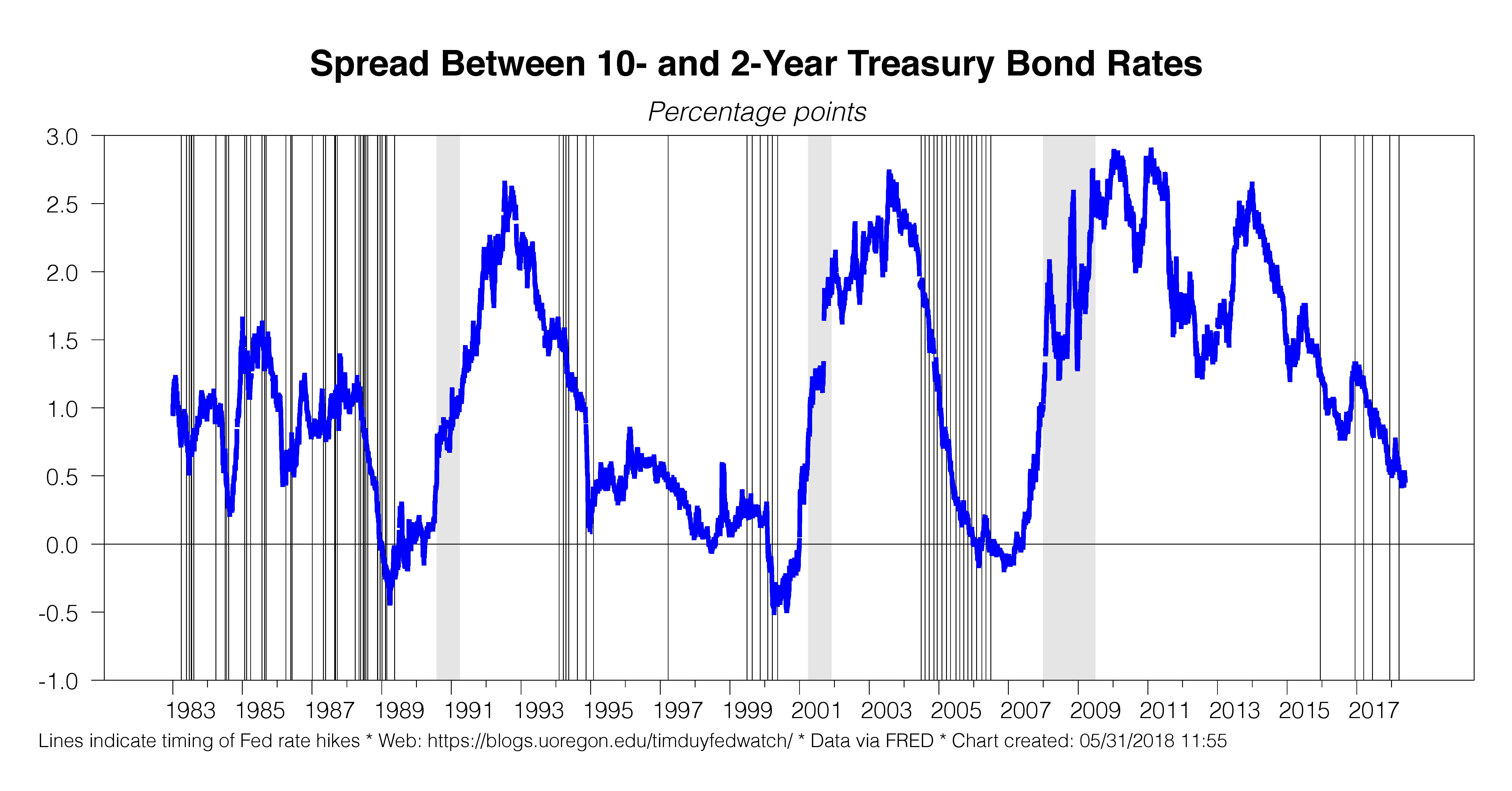

Most interesting to me were Brainard’s comments on the yield curve. She acknowledged the flattening yield curve and the recessionary signal of past inversions. But she then argues the “this time is different” story, claiming that the yield curve may be sending a weaker signal than in the past due to factors depressing the term premium.

What does this mean for policy? Brainard:

In the median outlook in the FOMC’s Summary of Economic Projections (SEP), the federal funds rate is projected to reach its longer-run value by 2019 and exceed it in 2020. If the 10-year term premium were to stay very low, that path would likely imply a yield curve inversion. But for the reasons I just noted, if the term premium remains low by historical standards, there would probably be less adverse signal from any given yield curve spread.

It is important to emphasize that the flattening yield curve suggested by the SEP median is associated with a policy path calibrated to sustain full employment and inflation around target. So while I will keep a close watch on the yield curve as an important signal on how tight financial conditions are becoming, I consider it as just one among several important indicators. Yield curve movements will need to be interpreted within the broader context of financial conditions and the outlook and will be one of many considerations informing my assessment of appropriate policy.

This is a clear willingness to invert the yield curve. Remember, a yield curve inversion is a very long leading indicator, perhaps signaling a recession more than a year in the future. Thus, when the yield curve inverts the economy will still be well below the peak of the business cycle. In other words, all of the data the Fed uses to assess the outlook will be strong. There will be a strong tendency in such an environment to ignore the signal of the yield curve and keep hiking rates. This has been the story in the past.

Of course, it is worth noting that a sizable contingent of the Fed appears to be concerned with inverting the yield curve. But these concerns may be overruled by key leadership at the Board. This is a space to keep watching closely.

Bottom Line: A solid US economy keeps the Fed focused on raising interest rates. I think that they will become more cautious when they get closer to the neutral rate, but Brainard’s comments suggest policymakers will be less cautious than I have been thinking. I still anticipate rate hikes in June and September. December still fuzzy.

{kind=link}