Incoming data on the manufacturing and services sectors as well as the job market continue to support a narrative of strong growth that will encourage the Federal Reserve in its campaign to push policy rates to the neutral level. Will they push beyond? The anecdotal stories in the ISM reports hint at an economy on the verge of overheating, but until that overheating shows up in wages or prices, stories are all they are.

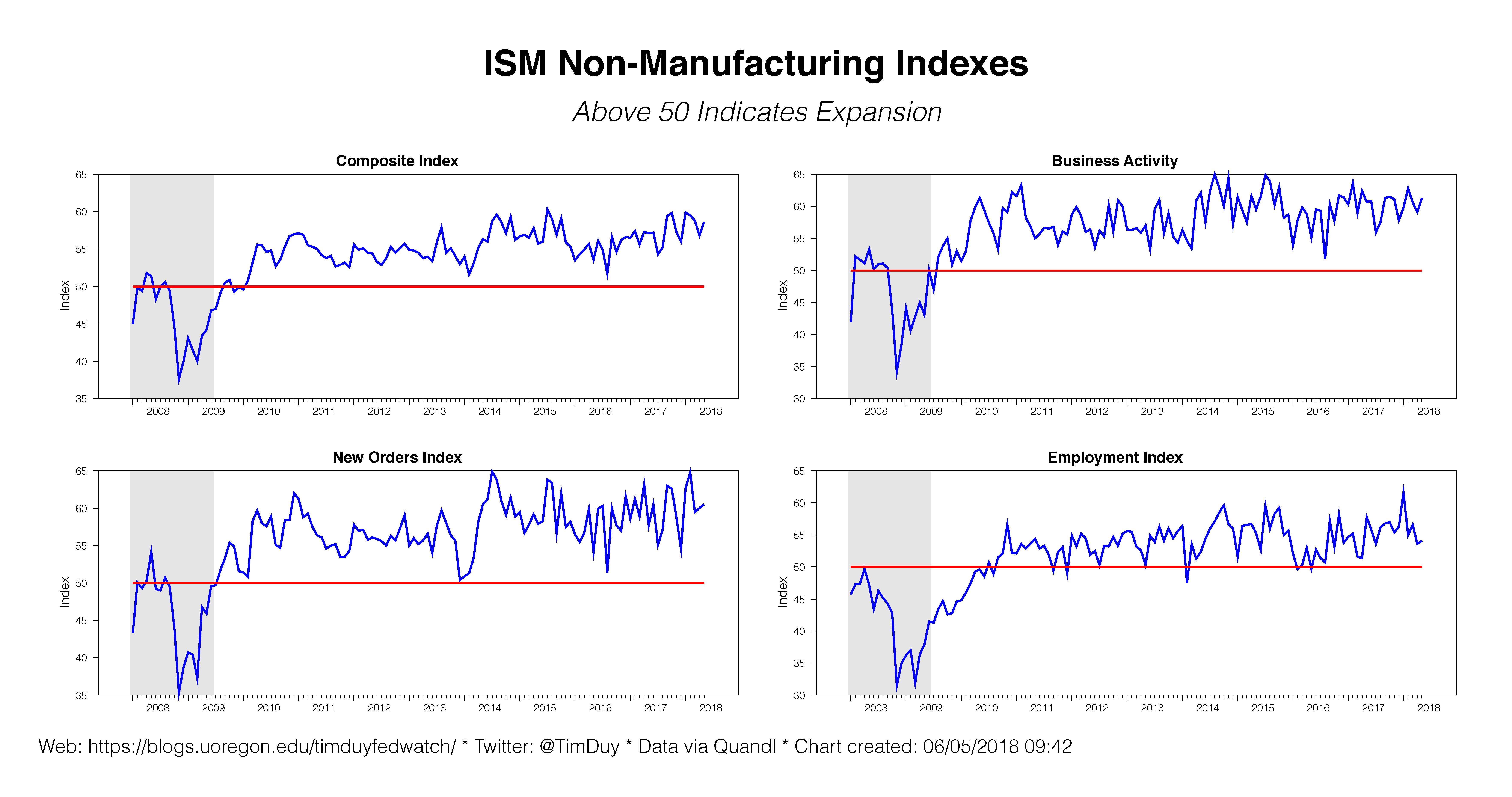

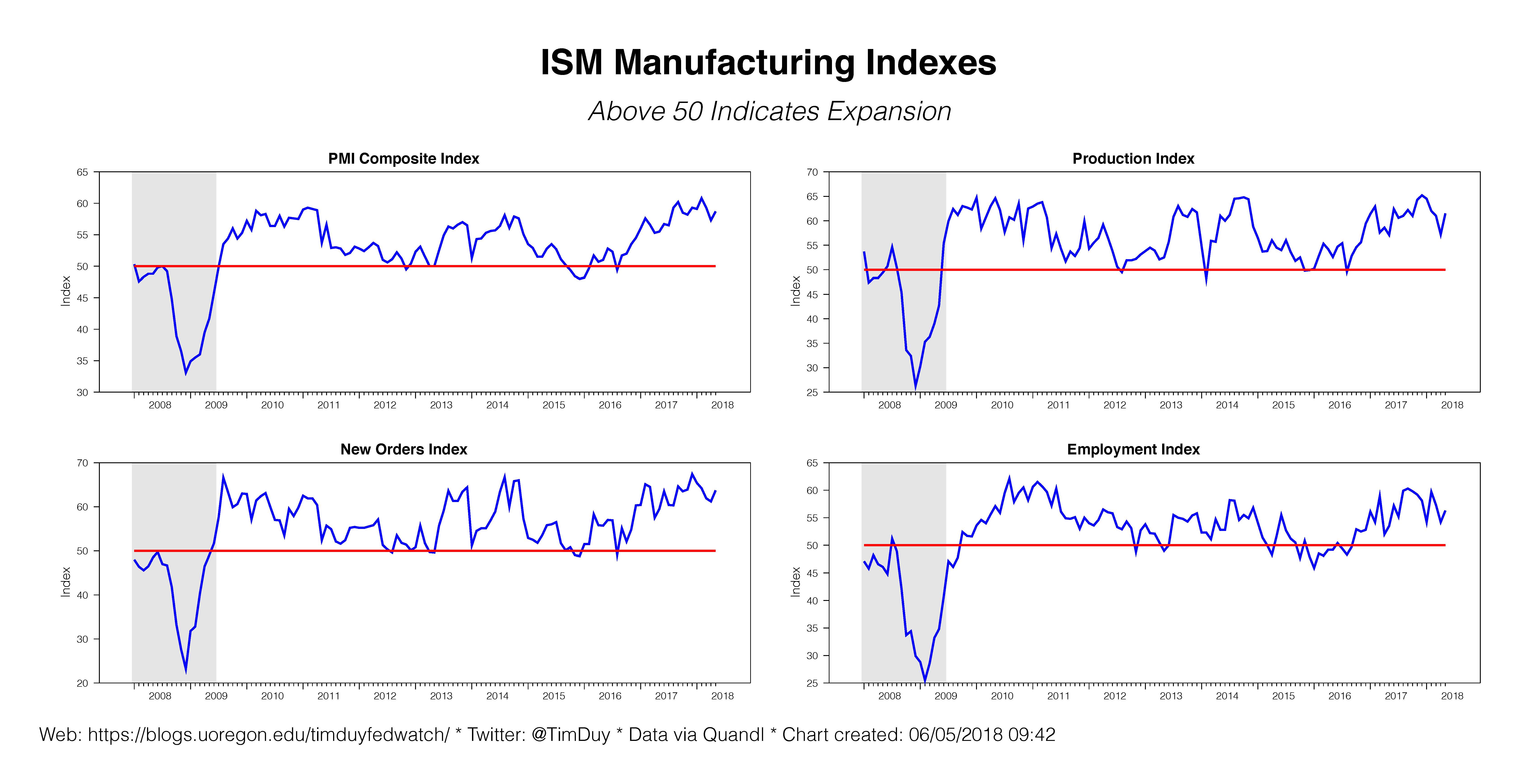

The ISM reports on the manufacturing and services sector were solid for May, both for headline and internal numbers. Particularly noteworthy were the rising supplier deliveries times as firms are unable to keep up with demand due either to production or shipping issues. These concerns are evident in the anecdotal evidence from respondents which largely speak to material and labor shortages. Concerns about tariffs also figure prominently as the resulting uncertainty and higher costs only exacerbate the problems of already tight supply chains.

While the prices paid measures in both the manufacturing and services sectors remains high, it is important to remember that these measures are not a strong indicator of consumer inflation. Still, the economy is heading into a zone not seen in decades – really, since the late 1960’s. In many ways, we really don’t know what comes next or which of the old lessons apply to the new economy.

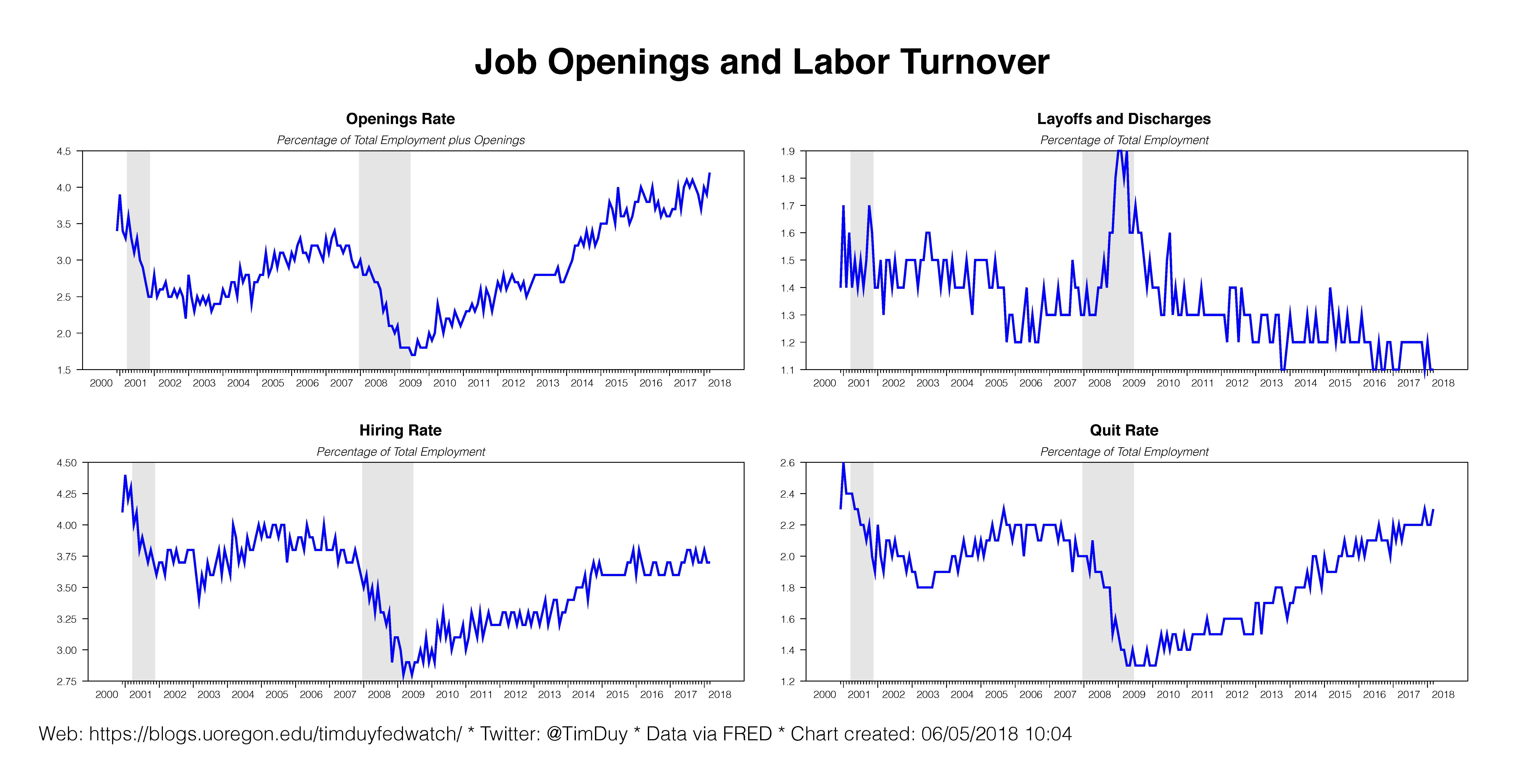

Similarly, job openings in the JOLTs report climbed higher, helping the labor market reach a new milestone in April as the ratio of unemployed workers to jobs fell to 0.95, the lowest since January 1970. That means there is more than one job available for each unemployed person. One would think that this should lead to faster wage growth, yet show far the wage gains remain fairly anemic. But perhaps a switch will actually flip and employers will lose the ability to control wage gains.

Bottom Line: The data flow continues to speak to an economy that grows increasingly tight with each passing month. That will keep the Federal Reserve in play; they will not easily bring rate hikes to a halt with the economy marching forward and threatening to blow well past full-employment. But has the economy exceeded full employment? Maybe, and there is a chance that wages and prices are only lagging the rest of the data. If so, the second half of this year will get interesting if the Fed faces a combination of ongoing strong growth and actual inflation. To be sure, they won’t get nervous about a modest overshooting of their inflation target. But if they see inflation moving sustainably toward 2.5%, they will feel compelled to act by pushing rates past neutral.