Federal Reserve Chair Jerome Powell reiterated that the Fed is in it for the long haul:

We remain committed to using our tools to do what we can, for as long as it takes, to ensure that the recovery will be as strong as possible, and to limit lasting damage to the economy.

The Fed’s lack of clarity on asset purchases may have caused some market participants to question the Fed’s willingness to maintain easy financial conditions, but Powell is saying that’s not the case. The willingness of the Fed to act is not the risk. The risk is that the economy improves more quickly than anticipated and catches the Fed off-guard. Maybe though not completely off guard. Powell does acknowledge that the economy is showing signs of life:

Economic activity has picked up from its depressed second-quarter level, when much of the economy was shut down to stem the spread of the virus. Many economic indicators show marked improvement.

That said, Powell remains focused on downside risks:

Both employment and overall economic activity, however, remain well below their pre-pandemic levels, and the path ahead continues to be highly uncertain… A full recovery is likely to come only when people are confident that it is safe to reengage in a broad range of activities. The path forward will depend on keeping the virus under control, and on policy actions taken at all levels of government.

That last line refers to the fiscal support for the economy, or the lack of continued fiscal support. Another coronavirus package, which I once thought was political no-brainer, looks very unlikely now that the battle for the next Supreme Court justice is heating up.

Powell attempts to get ahead of any criticism of the Fed’s credit facilities, particularly the Main Street Lending Program:

Many of our programs rely on emergency lending powers that require the support of the Treasury Department and are available only in unusual circumstances. By serving as a backstop to key credit markets, our programs have significantly increased the extension of credit from private lenders. However, the facilities are only that—a backstop. They are designed to support the functioning of private markets, not to replace them. Moreover, these are lending, not spending powers. Many borrowers will benefit from these programs, as will the overall economy, but for others, a loan that could be difficult to repay might not be the answer. In these cases, direct fiscal support may be needed.

Powell is making clear that many firms need grants, not loans, and that is the job of Congress to provide.

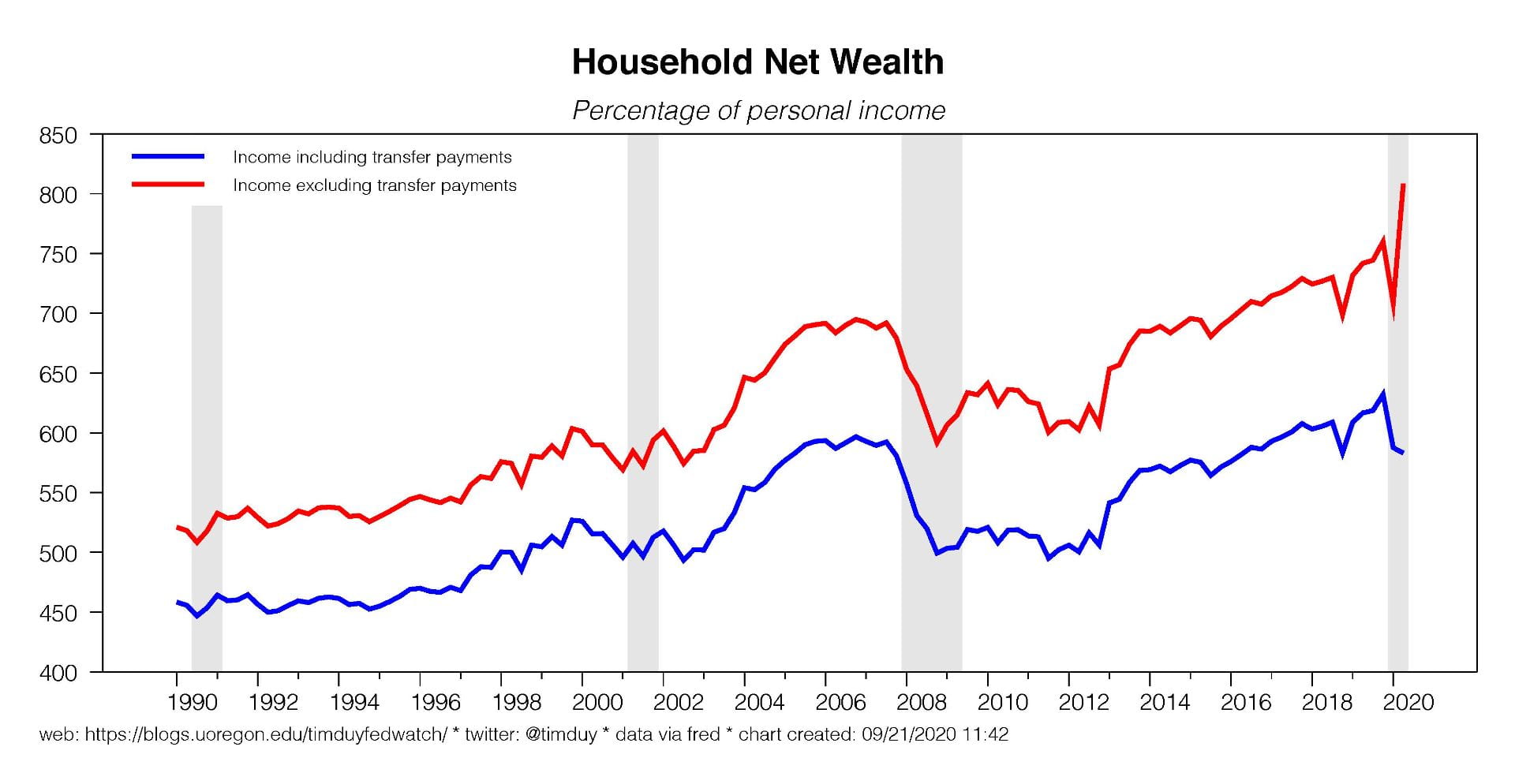

In other news, household wealth rose to a record in the second quarter as fiscal stimulus and rising house and equity prices boosted household balance sheets. Wealth is also at a record high as a percentage of personal income excluding transfer payments:

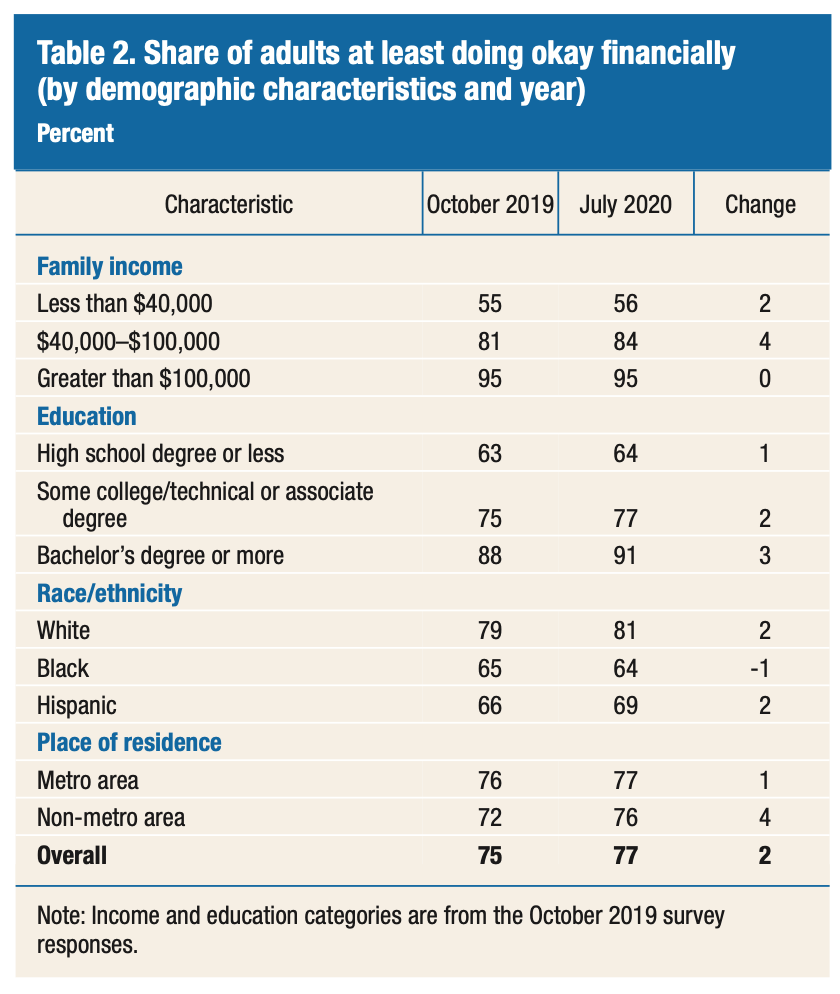

I know that there will be complaints that only the wealthy are better off, but the Fed’s recent report on the Economic Well-Being of Households suggests otherwise. I thought it fairly notable that households broadly believed that they were doing OK financially at the same or better rate than prior to the pandemic:

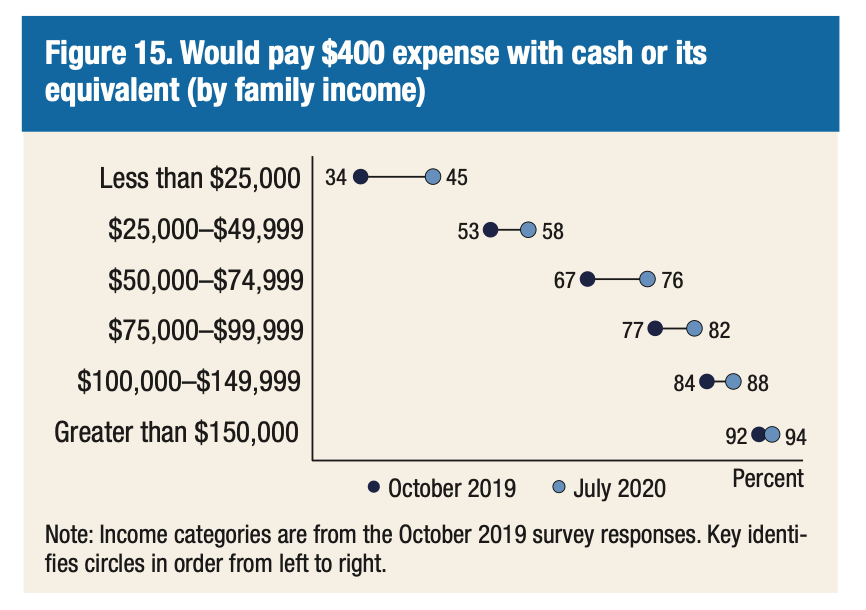

That’s pretty impressive given the economic hit suffered by many households. Also note the improvement in the percentage of households able to cover a $400 emergency expense with cash:

I guess not only the wealthy saved some of that stimulus money. The broader lesson is that fiscal policy works

Dallas Federal Reserve President Robert Kaplan explained his dissent. Via the Wall Street Journal:

Federal Reserve Bank of Dallas leader Robert Kaplan said Monday the U.S. central bank’s new guidance on the future of interest rates may complicate officials’ future decision making and stoke risk-taking in financial markets.

I don’t find this argument compelling. Tying its hands a little tighter to the new strategy is exactly what the Fed should be doing. Plus, they aren’t tied down by a commitment to QE, so they still retain room to work. In addition, the Fed could always use concerns about financial stability to change the policy stance; the new strategy elevated that option.

On a final note, equity markets have hit a bit of a rough patch. The declines are not sufficient to generate concern from the Fed especially as credit markets appear to be functioning normally. The Fed is arguably relieved for the market to pull back a notch as it will help alleviate any lingering financial stability concerns (looking at Kaplan).