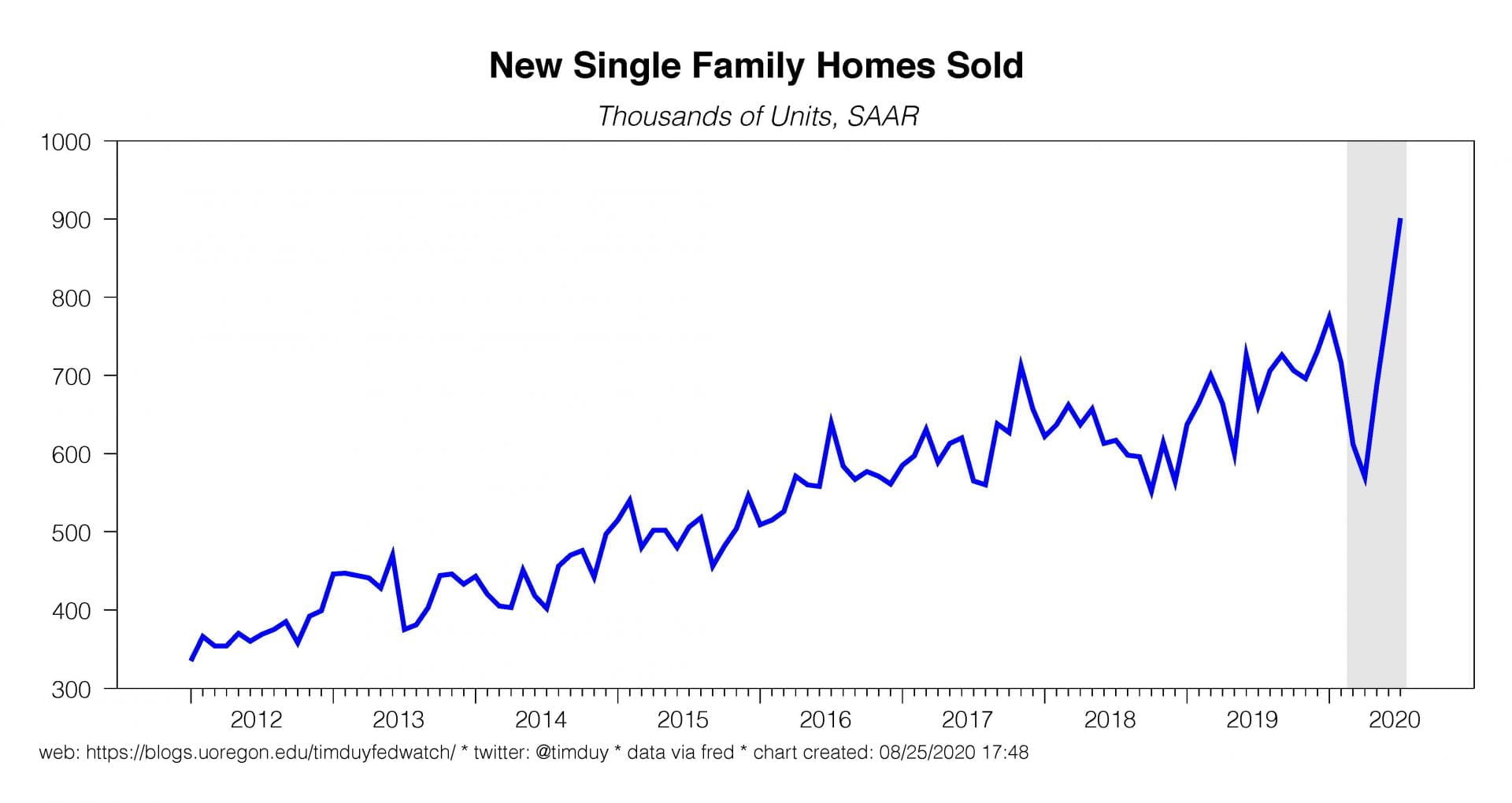

New single family home purchases came in ahead of expectations:

Basically not just a V-shaped recovery, but blowing through the pre-pandemic trend. The longer view:

People get upset when you say this sort of thing, but housing is a solid leading indicator. You just don’t see a recession when housing is on the upswing; you have to be wary about upside surprises in the overall data flow.

Separately, Federal Reserve Chair Jerome Powell speaks this Thursday morning. It is widely expected that he will reveal the outcomes of the Fed’s policy review and indicate that the Fed will be adopting some form of average inflation targeting. The Fed’s objective under such a scheme will be to allow inflation to rise above the 2% target to at least partially compensate for below target outcomes. The given rational will be that this will allow the Fed to more quickly meet its employment mandate and will help firm up inflation expectations in the low inflation, low interest rate world. Operationally, the Fed will lean more heavily on actual inflation than inflation forecasts derived from Phillips curve-based models and will pursue a lower for longer interest rate policy.

There is a temptation, which I share, to think Powell’s speech will be of little consequence because the Fed has already telegraphed these outcomes. The historian Peter Condi-Brown offers this alternative take:

I think a move to a monetary regime that would have substantially changed the course of 2015-2018 is a pretty big deal. I don’t know how markets will react*, but as a historian I think this is in the ballpark of the October 1979 press conference.

* always true https://t.co/kasmGrurBa

— Peter Conti-Brown (@PeterContiBrown) August 24, 2020

Those of us following the story may want to see Powell’s speech as little more than a formalization of what we already knew. Arguably, this is because we are too close to the topic. Had the Fed adopted this approach in the last expansion, it would not have raised rates so early nor as high. It would have been a significant difference relative to the actual outcomes.

Bottom Line: The strong housing market is a solid indication that we should not too heavily discount the possibility of a more robust expansion than currently anticipated. At the same time, Powell is giving a speech that can only be effective if it leaves no doubt that the Fed is absolutely, certainly locked into the current policy path or an even easier policy path. That combination has some fairly positive implications for the outlook.