If You Don’t Have Any Time This Morning

It will be a busy week for data. The Fed will continue to paint a dovish picture of the economy. I am watching four other stories right now: Delayed fiscal policy, rising inflation expectations, a weaker dollar, and a potential leveling off of Covid-19 infections.

Bloomberg Opinion

My Bloomberg column last week:

The Federal Reserve has come around to the conclusion that inflation isn’t going to be a problem. So now it’s time to start wondering if inflation is going to be a problem. The Fed has a tendency to fight the last battle, which could lead policy makers to miss what may be the “Great Inflation” era.

Continued here.

Key Data

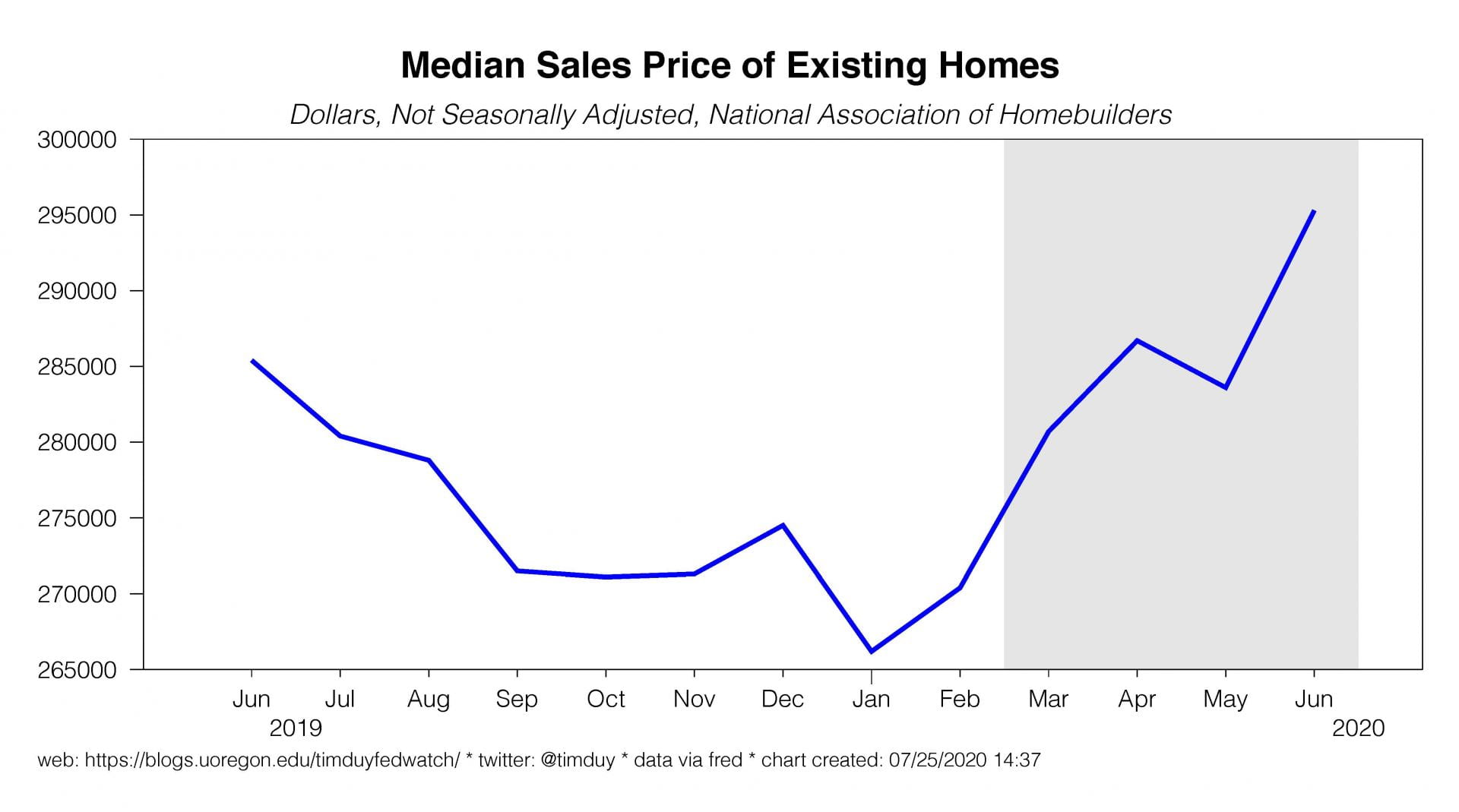

The U.S. housing market remains remarkably resilient. New single-family home sales rebounded to an annual rate of 776k, their highest level since 2007. Existing home sales continue to recover lost ground; I anticipated they will come closer to full recovery in the July numbers. Median sales price also rose and is 3.5% higher than a year ago.

The strength of housing appears inconsistent with a recession, but the pandemic comes at a time of structural strength for the sector. Aging millennials provide demand for housing after a long period of low levels of construction. Low mortgage rates create further incentive to buy. And those boomers you thought were ready to leave their homes and open up some supply? That’s going to be delayed again. Seriously, if you are 60 years old and watching the news, you probably think that retirement communities and nursing homes are basically death traps. To me, that argues for people working harder to stay in their own homes for longer.

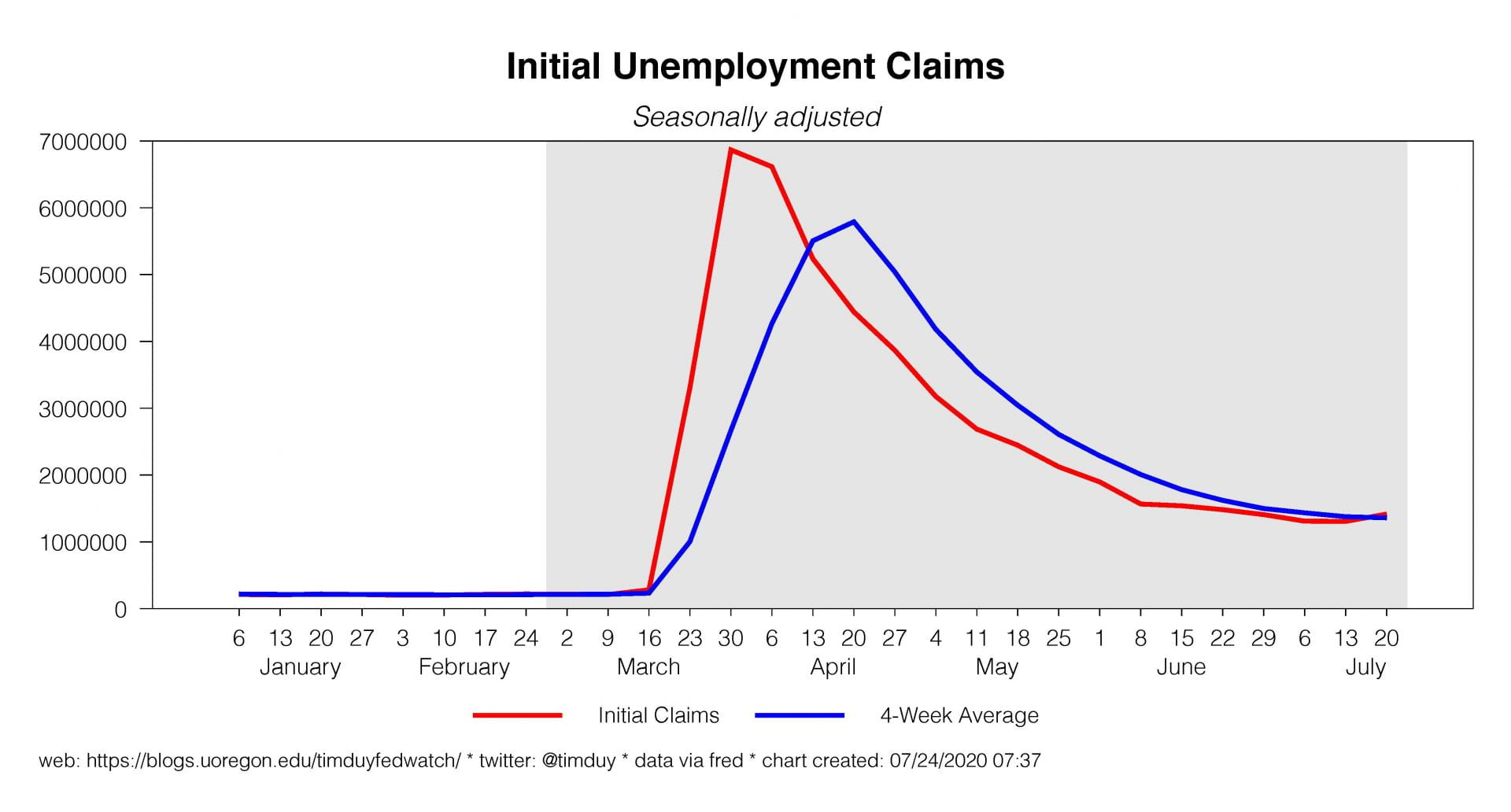

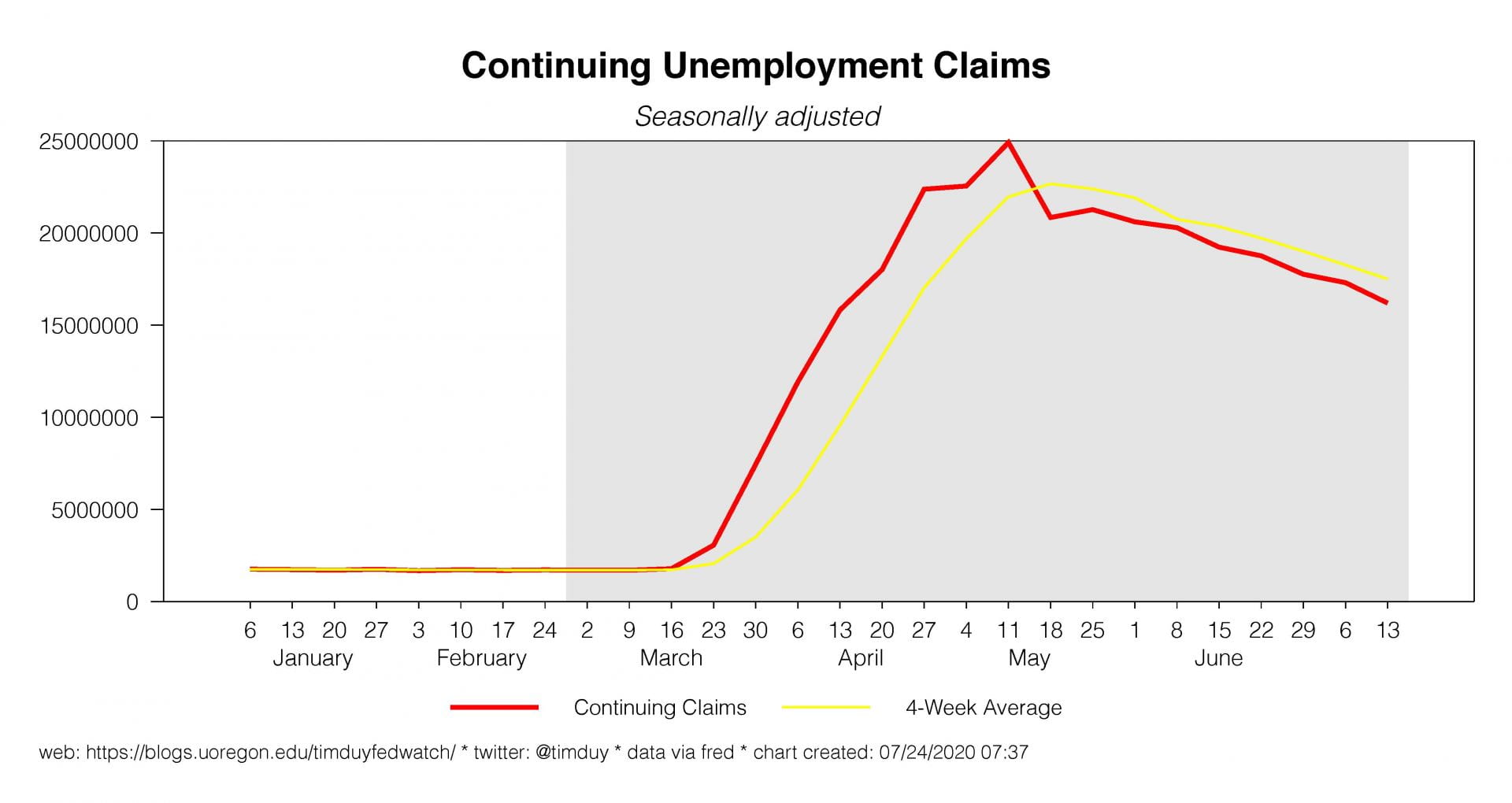

Initial unemployment claims edged higher; continuing claims continue to fall slowly. Slower activity and renewed firm closures in the worst-hit pandemic regions will likely put some upward pressure on claims in the coming weeks. The labor market simply will not heal easily until the pandemic is contained.

The IHS Markit flash report for July improved to a six-month high but also indicated headwinds to growth from rising Covid-19 cases. The Eurozone version posted the strongest numbers in two years. Almost as if a credible response to the pandemic was important for the economy.

Fedspeak

Blackout week ahead of this week’s FOMC meeting, so thankfully we could all take a break.

Upcoming Data

Busy week ahead as the data flow picks back up. Monday we get durable goods orders with core orders excluding defense and air are expected to be up 2.3% in June. These numbers have held up better than expected given the depth of the downturn; stronger investment now would help mitigate some of the negative long-run impacts from this recession. Conference Board consumer confidence comes on Tuesday; it is expected that virus-pessimism drags down the number to 94.5 from 98.1 in June.

Wednesday is FOMC day plus press conference; no policy changes expected but the overall event will have a dovish feel. Also Wednesday is pending home sales for June. Watch for more signs of a V-shaped recovery in this sector.

Thursday will be exciting! Be ready for a historic collapse in the GDP numbers over the second quarter, expected to be down 34% on an annualized basis (block anyone who says output dropped by a third). We are all prepared for the worst so I am a little cautious that there is room for an upside surprise. Also on Thursday we get the usual initial claims report.

Friday brings the household spending and income numbers for June although we should have a pretty good idea of the outcome from the GDP report the previous day. Pay attention to the core-PCE numbers as all of our dovish Fed bets hinge on that staying weak. Likewise, we get the University of Michigan sentiment numbers for July. I am watching the inflation expectations numbers in particular.

Discussion

I discussed the Fed last week, and nothing much there has changed. The Fed is stuck between the emergency actions of this past spring and the next steps to bolster the recovery that will come later this year. The most likely outcome for this week is no policy change but a dovish tone to the statement and the press conference.

Aside from the Fed, there are four stories I am watching right now. The first is fiscal policy. The enhanced unemployment benefits – a critical lifeline for the economy – are coming to an end. Republicans in the Senate are rushing to cobble together their own package two months after the House Democrats passed theirs. I find this delay hard to believe given that with each passing day the Republicans look to be suffering more in the polls and this would have been an easy way to get ahead of at least the economic concerns. Instead, the Republicans look like they were hoping that if they didn’t do anything, the virus would just disappear on its own. In the very near-term, the delay could weigh on spending and consumer and investment sentiment. That said, the delay may have shifted the bargaining strength to the House Democrats; if so, the ultimate package will be larger.

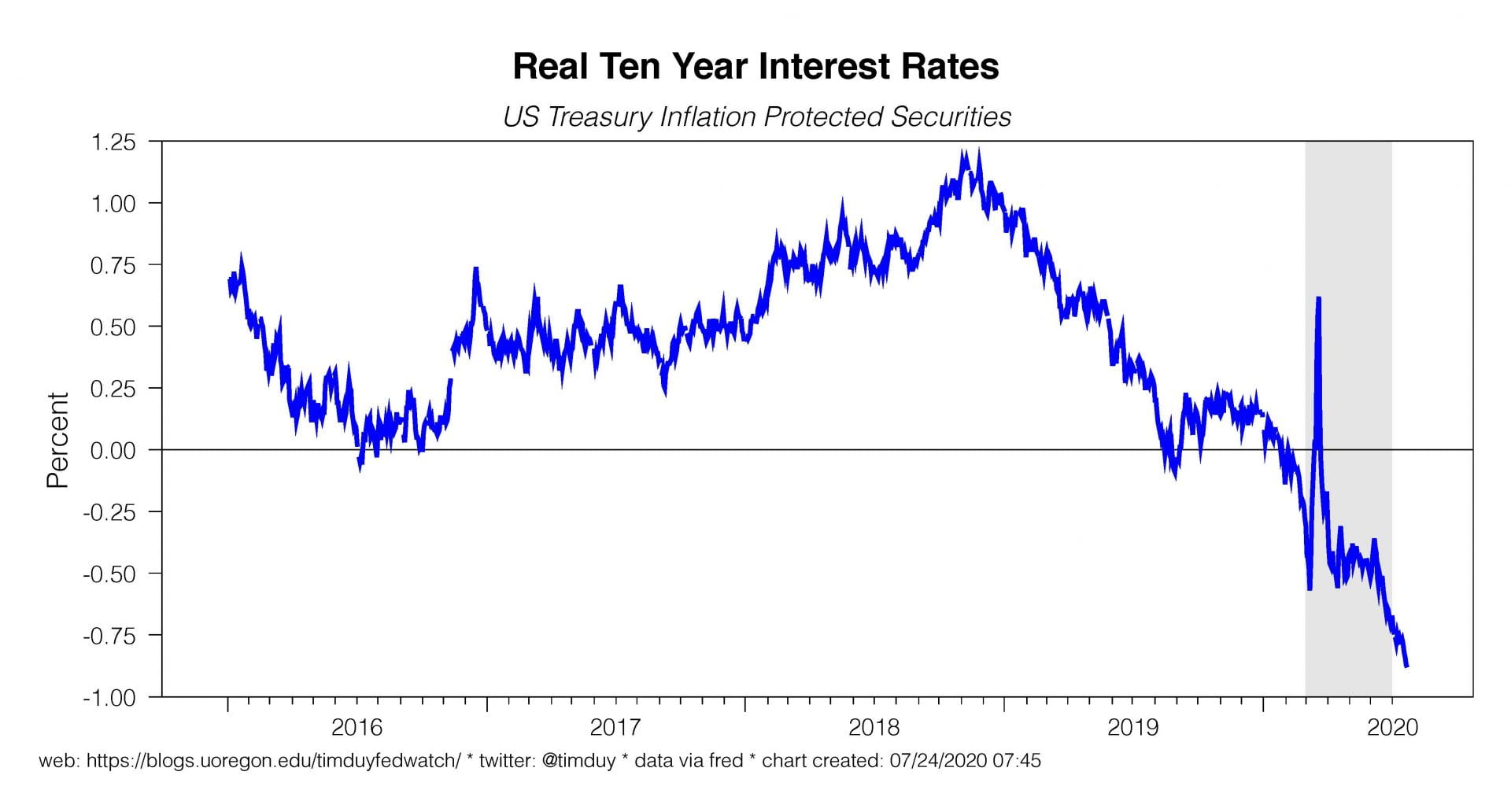

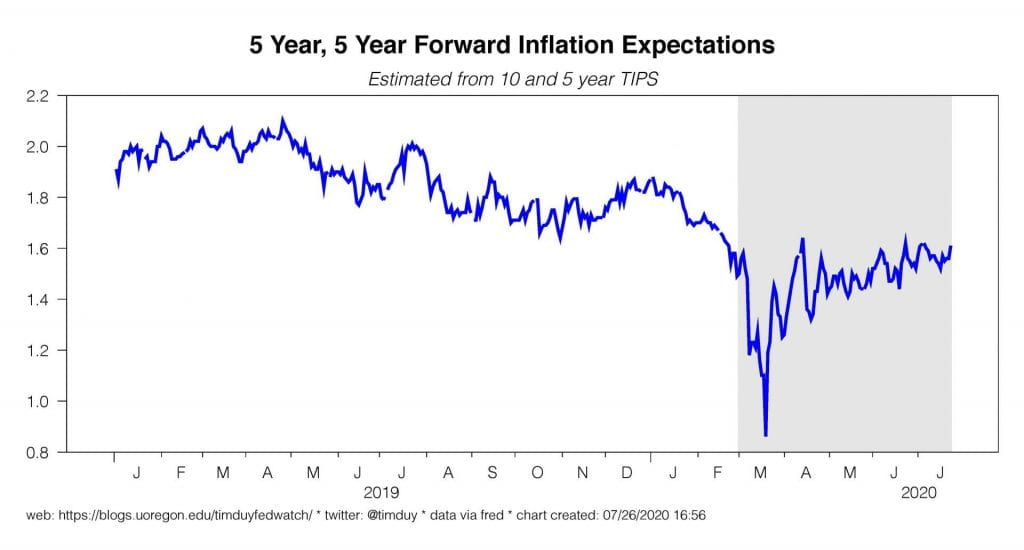

A second area is inflation and inflation expectations. Interest rates on TIPS are down as investors look to secure protection from inflation. Or maybe not. Roberto Perli from Cornerstone Macroeconomics argues that this is not the case:

(4/4) As liquidity normalizes, the TIPS liquidity premium drops. This pushes TIPS yields down and spot breakevens up. There is no inflation story, just a liquidity story. pic.twitter.com/u3ocFeKDnH

— Roberto Perli (@R_Perli) July 24, 2020

The TIPS market is known for being less liquid; you have to expect you might have a hard time selling a position and thus would need to protection in the form of a lower price/higher rate. If liquidity in the market is now improving and you can more easily find a buyer, prices should rise and rates fall, but this is not about inflation expectations.

I wonder if we can so clearly separate liquidity conditions from inflation expectations. If I think that other investors are worried about inflation, then I might reasonably conclude that market conditions would improve. Likewise, if I think the tail risks of deflation have lessened, I might think there were more potential buyers. I have in my head the idea that a market for inflation protection would be more liquid if participants were actually worried about inflation (or at least no longer worried about deflation). Also, is you think the Fed will via financial repression hold nominal rates flat, you would think there would be a bias towards TIPS.

Regardless, narratives matter and the story around inflation is one worth watching. I have said before that inflation is not likely a problem given the size of the negative demand shock and, consistent with that observation, the rise of inflation expectations doesn’t yet approach a level that would be concerning from a policy perspective. But there is also room to rise between here and where there might be some policy implications. So I am just keeping an eye on these next few inflation numbers and how they might feed into this story.

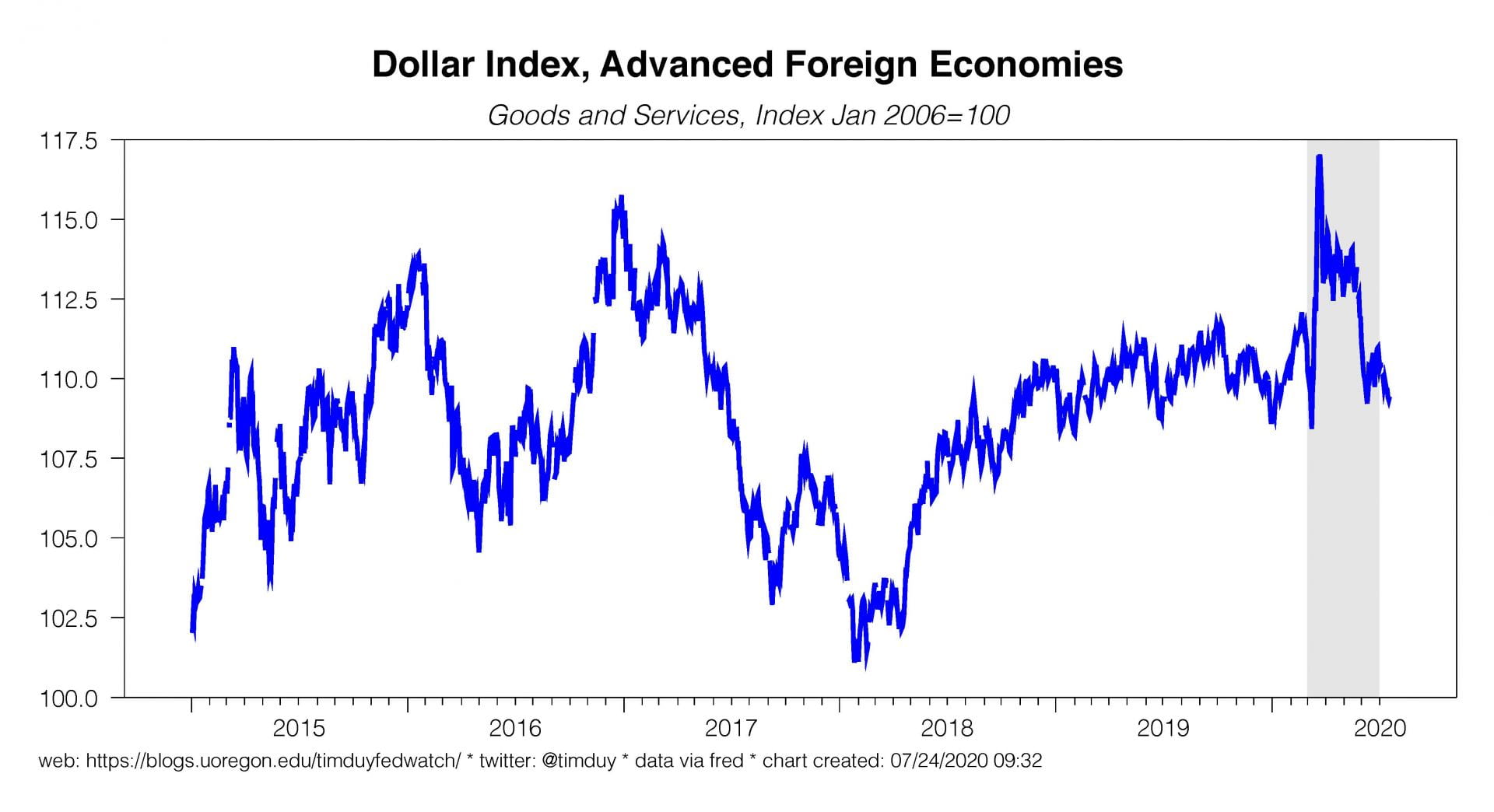

A third and related story is the dollar, which looks to be vulnerable. As noted earlier, the Eurozone looks to be recovering from the Covid-19 shock more rapidly than the U.S. This coupled with a Fed looking to ease further is dollar negative, at least for now. And, as you know, once a narrative takes hold in currency markets, it can be sticky and trigger a big move. Which interestingly would put upward pressure on core inflation and thus create some interesting dynamics on that issue.

The final story is the possibility that Covid-19 infections in the U.S. are leveling off. This thread from Jens Nordvig of exante data is important:

Most likely, the US will now stay in an odd greyzone, with more stable, but still very elevated case growth into August. And each state will have to worry about importing cases from others states with bigger outbreaks (as domestic travel bans are unrealistic)

— Jens Nordvig (@jnordvig) July 24, 2020

Stabilization of Covid-19 cases would be good in that it might short-circuit more pessimistic scenarios of further shut-downs but bad in comparison to the Eurozone. That too could be on net dollar negative.

Bottom Line: Housing is a stand out sector, but can’t carry the U.S. economy all by itself. The inability of the U.S. to manage the pandemic leaves the economy struggling in absolute terms and relative to its peers. Delays in the next fiscal support picture negative in the very near term but might lead to a big package. Fed will stay dovish.