Keeping the Fed on the sidelines means having enough positive data to keep their forecast near one consistent with trend growth but not enough positive data to make them think they need to reverse last year’s rate cuts. It’s hard to see the latter situation happening anytime soon with Federal Reserve Chairman Powell looking for either actual, significant inflation or a real risk of significant inflation before raising rates. Instead, incoming data looks to be closer to trend growth; the employment report is expected to conform with that outlook.

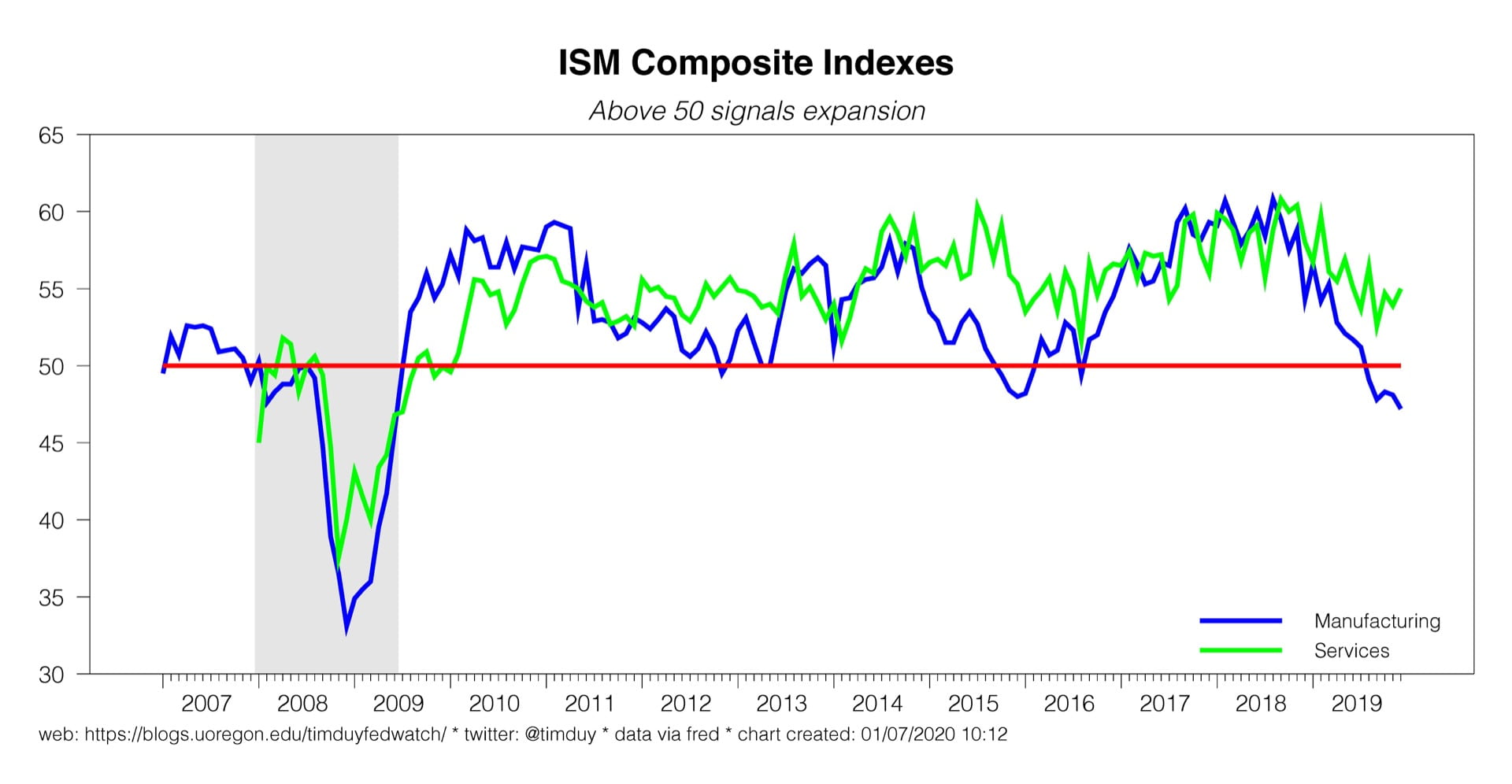

Last week, the ISM manufacturing index disappointed, stubbornly refusing to match the more optimistic PMI story. Manufacturing, however, is only a part – an increasingly smaller part – of the economy. A manufacturing recession no longer guarantees an economy-wide downturn, a lesson learned in 2015-16. As far as recessions are concerned, we should be on the lookout for economy-wide shocks that pull down the services sector along with manufacturing. So far though the services sector remains resislient as seen in this week’s ISM services report:

This kind of divergence is what we saw in 2015-2016; note the contrast with 2007-2009 when both measures move in virtual lockstep deep below 50. That’s what we would expect with an economy wide shock and aren’t seeing now.

I have been on this soapbox before, but I will get on it again: If the manufacturing cycle is less tied with the overall cycle than it has been in the past, a lot of analysis is going to be upended. We need to be very careful when telling economy-wide stories with the manufacturing data.

As far as the Fed is concerned, the softness in manufacturing and associate economic risks were enough to justify last year’s rate cuts. The resiliency of the rest of the economy prevents any further cuts. Friday’s employment report is expected to confirm that resiliency. Wall Street expects a Goldilocks report with nonfarm payrolls growing by 164k, unemployment holding steady at 3.5%, and wages up 3.1% over the past year. Those are numbers that the Fed will see as consistent with solid but not spectacular trend-like growth with no reason to believe the economy is overheating or will soon overheat.

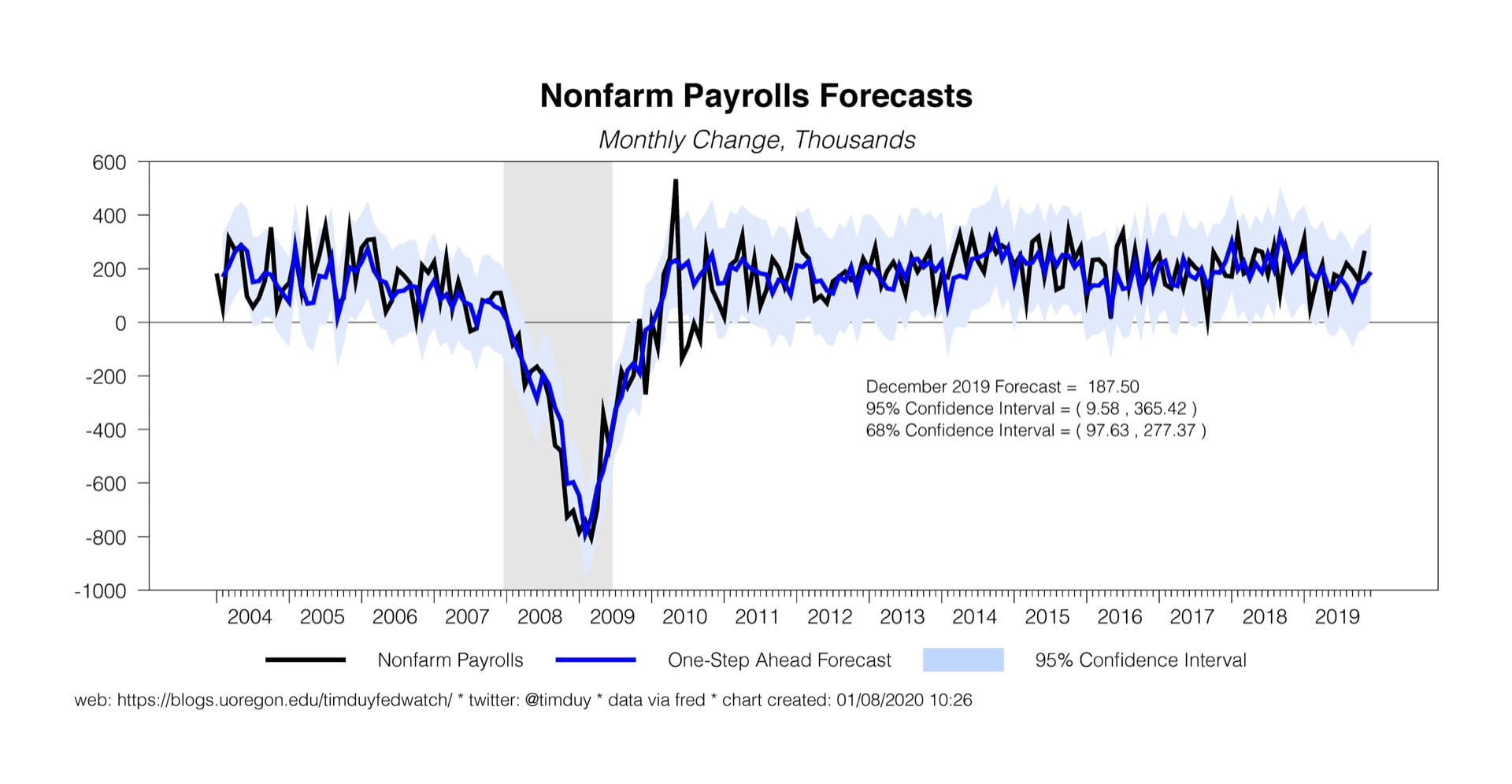

Today’s ADP number surprised on the upside with a 202k gain in private employment and thus provides for the possibility of an upside surprise Friday. My payrolls estimate for the report is a tad higher than Wall Street at 188k:

Anything in that zone would be consistent with the Fed’s basic story. What about outside that zone? Realistically, the data is sufficiently noisy that no single data point would change the overall story. We should instead be looking for patterns of data that threaten to send unemployment higher to justify a rate cut. So a single weak report would likely not do that in any meaningful way; two or three consecutive weak reports would be more interesting.

Bottom Line: Fed on hold until the tenor of the data meaningfully shifts.