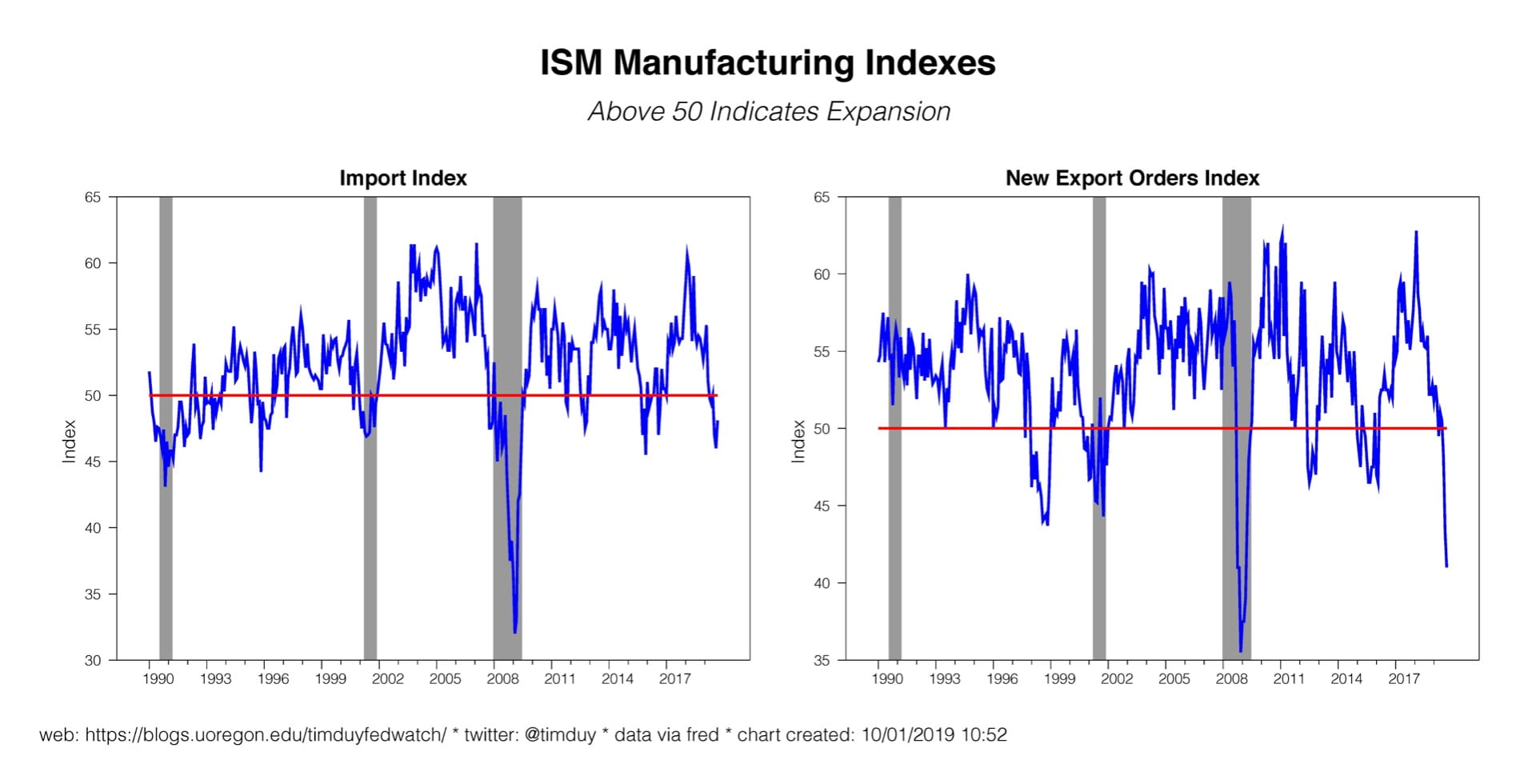

October began on a weak note with a fresh drop in the ISM manufacturing report. It remains at levels that foreshadowed past recessions while those same levels have also been false alarms:

The mid-90s are notable examples of false alarms. The period around the Asian Financial Crisis is particularly interesting given the sharp drop in the new export orders that occurred in the absence of a U.S. recession:

The export orders index, which reflects external conditions, slipped past the 1998 low, indicative of the current severe slump in global activity. The current slump in the import orders index, which is more reflective of internal conditions, is more severe than during the Asian Financial Crisis. This pattern makes sense to me as there exist two factors weighing on U.S. manufacturing. The first and likely dominant force is the global slump. The second force is the deleterious impact of U.S. trade policy. The latter is obviously a self-inflicted wound.

From the Fed’s perspective, the data suggests that the risks to the outlook are increasingly realized in weaker data. As the Fed was positioned to cut rates further if the data continued to weaken, today’s ISM report argues in favor of an October rate cut. CME odds moved accordingly as the chance of a rate cut rose to 65%, up from 40% on the last day of September.

Still, 65% is not nearly a sure thing. The lack of commitment is understand given that we have a busy week of data still ahead with Friday’s employment report of particular interest. It also likely reflects some lingering concern about a possible revolt against another rate cut by the hawkish contingent of FOMC participants. The latter is effectively a non-issue; the core of the FOMC voters is inclined to cut rates if the data does anything but improve. That meant there was a better than 50% chance of a rate cut regardless of any griping by the hawks. And, realistically, if the employment report reveals further downward momentum in job growth, a rate cut in October is pretty much a lock.

Bottom Line: October begins on a weak note, strengthening the case for a rate cut at the end of the month. Still much data ahead, but it needs to on net show improvement to keep the Fed from cutting again. Those ISM false alarms in the 1990s were likely false because, like now, the Fed cut rates proactively. It remains to be seen if the Fed can pull off that trick a third time. The fact that housing responded quickly to lower interest rates suggests that they can.