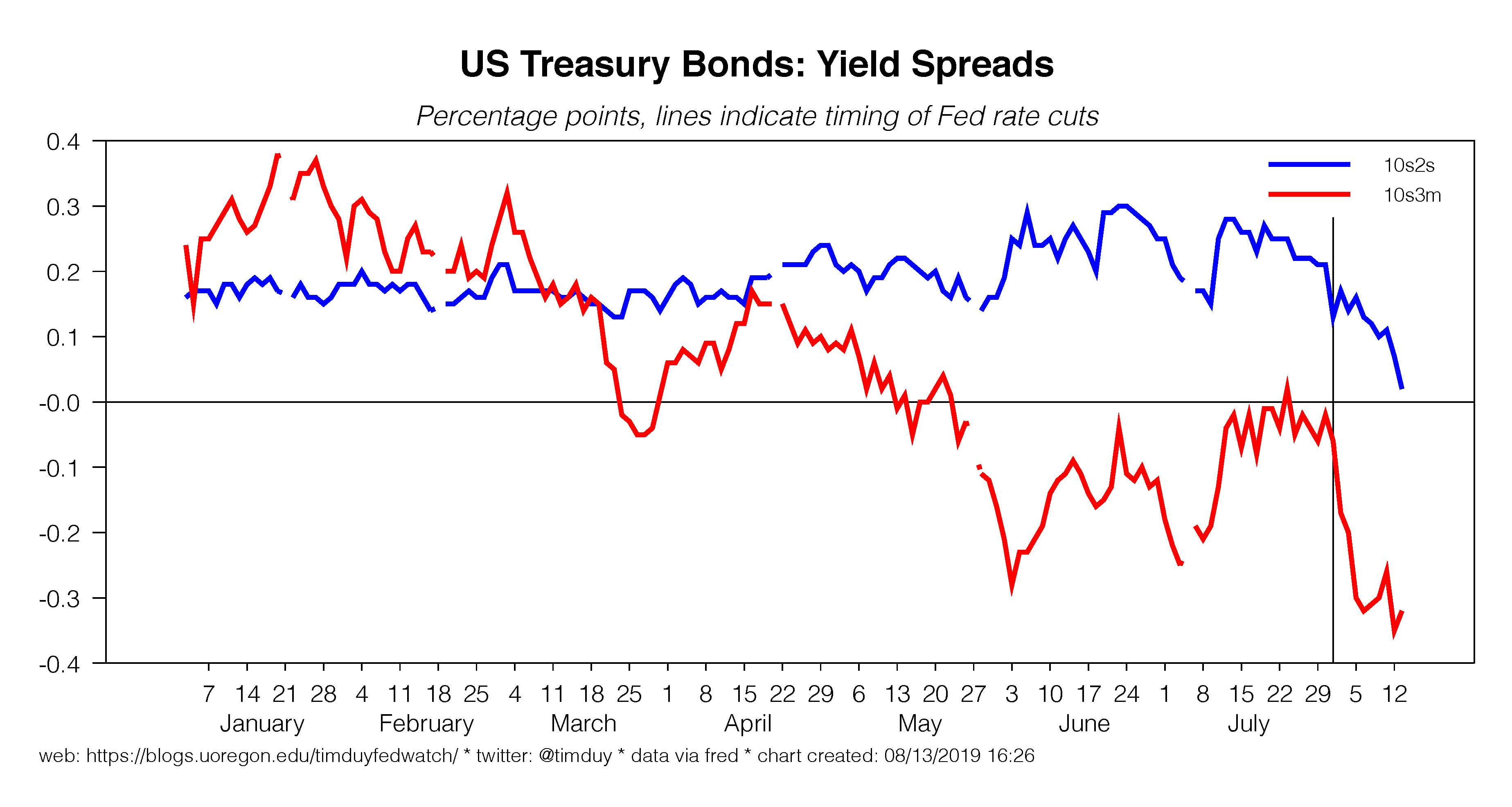

Stocks rallied and bonds fell as President Donald Trump blinked first on his latest round of threatened tariffs. Tariffs on many consumer goods are now delayed until December to prevent upward pressure on prices during the holiday shopping season. Although this in theory should relieve some uncertainty about the outlook, the yields on the shorter end of the curve rose less than on the longer end, pushing the 10s2s spread closer to outright inversion:

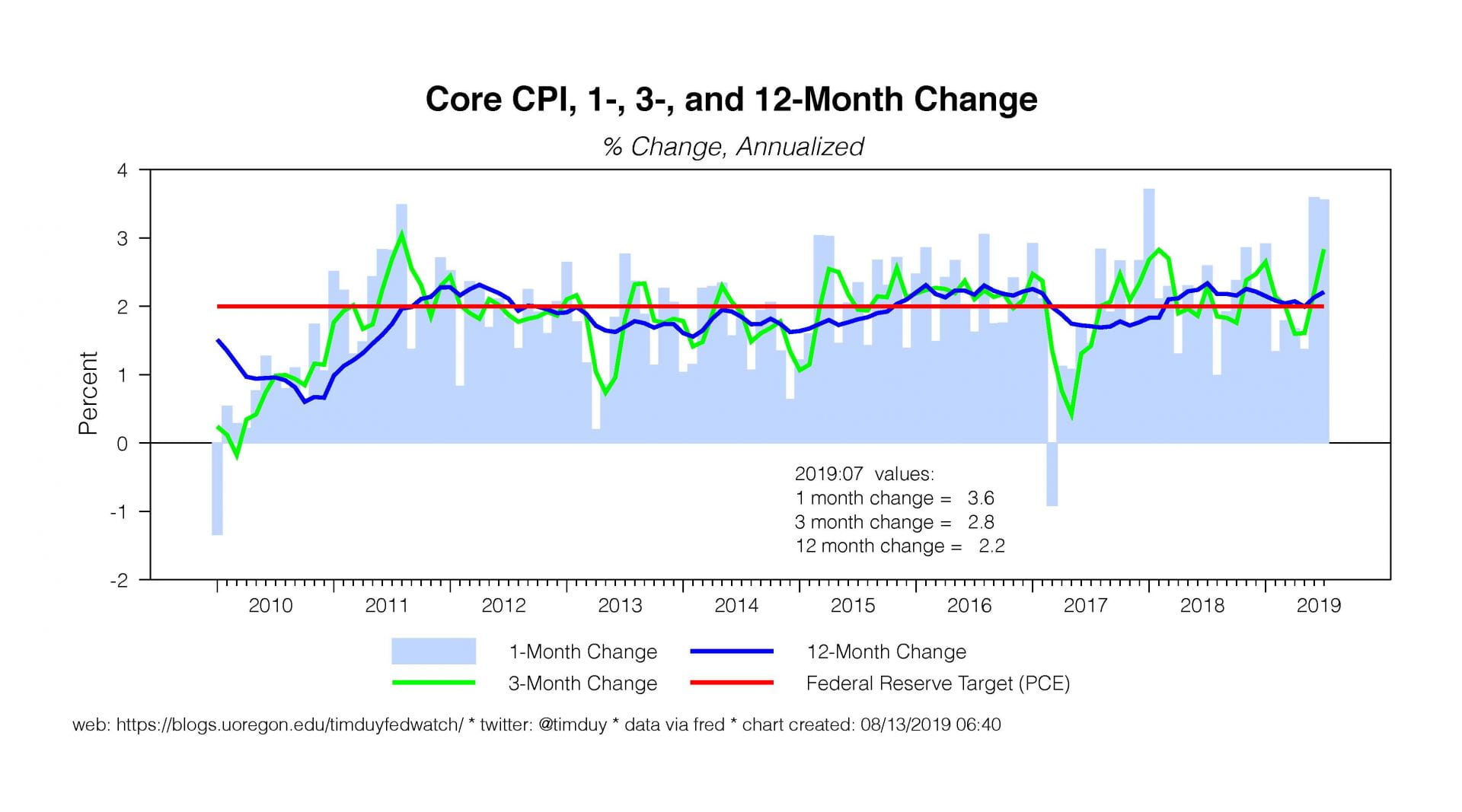

My instinct is to interpret this as indicating that the Fed is expected to be less likely to ease sufficiently to avoid a recession. Why might this be? One explanation is that since the Fed has tied trade tensions to rate cuts, the easing of those tensions in turn reduces the magnitude of expected cuts. A second explanation might be found in the other news of the day, the inflation numbers. Core-CPI inflation came in high for a second month:

If this keeps up, the low year-over-year numbers won’t be low for too long. Market participants may be thinking that the Fed’s dovish shift won’t last long if inflation ticks up. Fed policy makers can say that their inflation target is symmetric, but they have yet to prove it is symmetric. We need some consistently above-target outcomes for the Fed to prove itself.

As far as easing trade tensions are concerned, I doubt the Fed will take much comfort in the latest developments. Yes, Christmas may have been saved, but that wasn’t the big problem. The Fed sees only small impacts on the aggregate economy from the mechanical impacts of tariffs; it’s the confidence effects on business investment that most worries the Fed. Those haven’t gone away and, if anything, are magnified by Trump’s flip-flopping. This anecdote via Bloomberg reveals the underlying problem:

“It’s too late and it’s not enough,” said Peter Bragdon, chief administrative officer for the Columbia Sportswear Co. “There’s continued chaotic policy making and incoherence coming out of Washington that makes it very hard for businesses in the United States to plan.”

Firms still face continued Trumpian uncertainty and consequently there is really no reason for the Fed to shift gears and think the associated risks have been mitigated.

As far as inflation is concerned, at least part of the firming inflation numbers are attributable to tariffs which, by themselves, should be viewed as one-time price shocks. Or, in the Fed’s preferred language, they have only transitory impacts on inflation. This is a very clear test for Powell & Co. They have quickly embraced inflation shortfalls as transitory. Will they do the same analysis if inflation exceeds target? I think that the Fed will error on the dovish side. That at least is what the Fed has been signaling.

Bottom Line: Neither of the today’s developments – “easing” trade tensions or higher inflation – should prevent the Fed from easing at next month’s meeting. I suspect though that they make it hard for the Fed to justify a 50bp cut in September. If the economy needs a more aggressive Fed response up front to prevent recession, then a lower chance of that outcome (now priced about 0%) should induce the longer end of the yield curve to flatten further and then invert.