Federal Reserve Chairman Jerome Powell delivered the Fed’s Semiannual Monetary Policy Report Tuesday morning. Powell smoothly and confidently responded to – or deflected – questions as if he were already seasoned in the role of Chair. As to the content of his remarks, they were hawkish. More hawkish than I anticipated and arguably signaled a significant change of focus for the Fed.

My focus fell on this in the written testimony:

In gauging the appropriate path for monetary policy over the next few years, the FOMC will continue to strike a balance between avoiding an overheated economy and bringing PCE price inflation to 2 percent on a sustained basis.

This is a crucial sentence that marks a change in focus. Compare this with the previous version of this testimony, delivered by former Federal Reserve Chair Janet Yellen in July of last year:

The Committee continues to expect that the evolution of the economy will warrant gradual increases in the federal funds rate over time to achieve and maintain maximum employment and stable prices.

And then her appearance before the Joint Economic Committee in November:

We continue to expect that gradual increases in the federal funds rate will be appropriate to sustain a healthy labor market and stabilize inflation around the FOMC’s 2 percent objective.

In both of these of these occasions, Yellen described the policy path explicitly in terms of the dual mandate in both sustaining a healthy labor market and meeting the inflation objective. Now compare that to Powell. The emphasis is no longer on sustaining a healthy labor market. It’s on avoiding an “overheated economy.”

That is a clear shift in policy focus. The policy objective went from attempting to achieve maximum employment to sustaining maximum employment to avoiding overheating. That runs counter to claims in the FOMC statement that the risks to the outlook are roughly balanced. Sustaining maximum employment suggests a balanced outlook. An objective of preventing overheating, suggests the risks are tilted toward inflationary pressures. Among the denizens of Constitution Avenue, the fear of falling behind the curve thus looks to be considerably higher than believed.

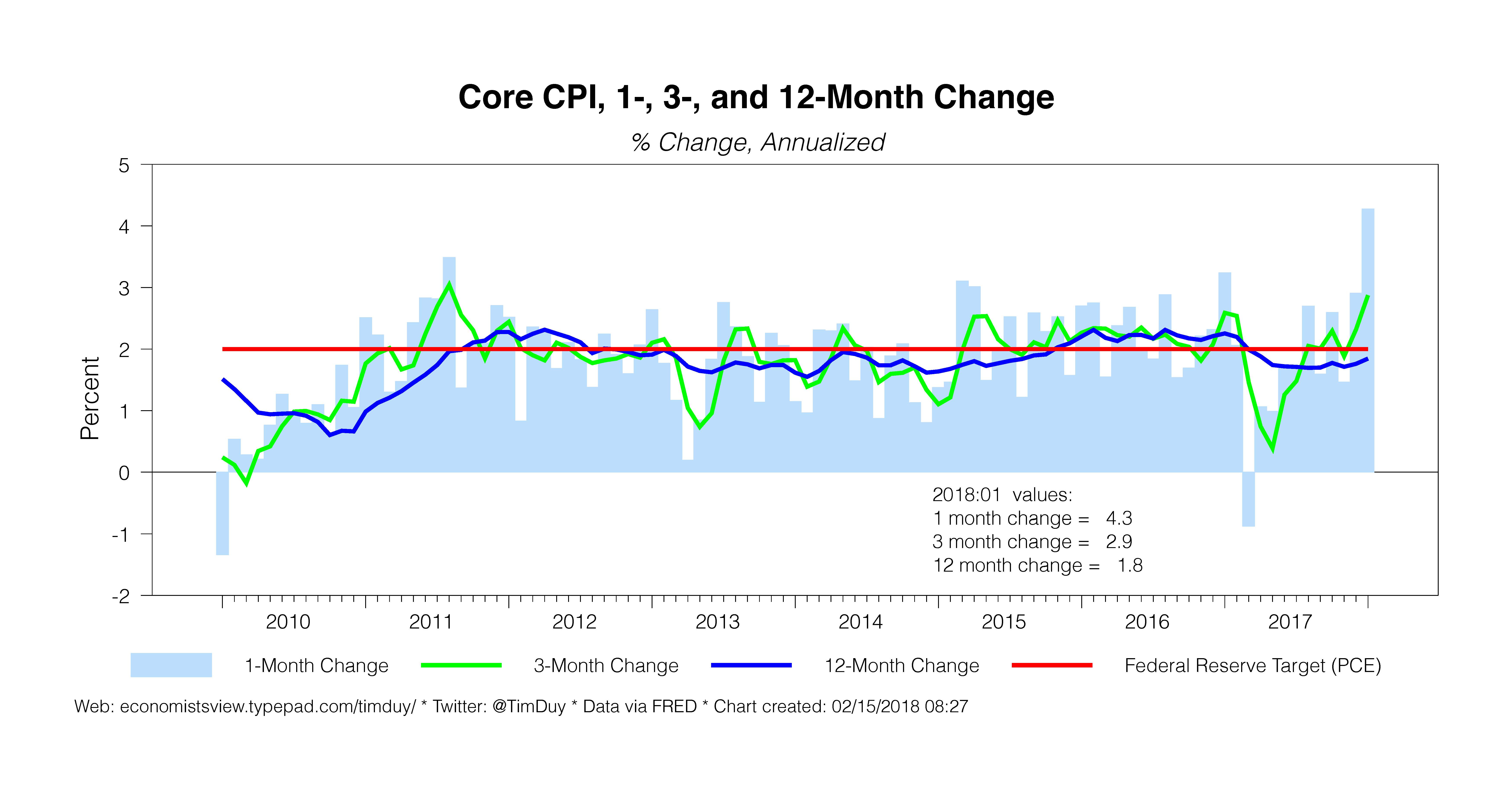

This shift to a focus on overheating is surprising given that inflation has yet to hit the Fed’s target. Apparently their confidence in reaching 2 percent or so this year has translated into fears of a substantial overshoot.

That said, even with this change, the testimony reiterated the commitment to further gradual rate hikes. Gradual had come to mean three hikes this year, but with a risk of four. That risk is clearly higher now. That fourth rate hike, however, is not my primary concern at this point. My primary concern now is that the Fed’s focus is on preventing overheating, the shift to an even more accelerated pace of rate hikes could occur very quickly.

Also note that the testimony is written from the point of view of the FOMC. Hence, the shift to a focus on an overheated economy should reflect a consensus viewpoint. I don’t that recent Fedspeak reflects such a shift. I am thinking there was an internal decision to let Powell raise the overheating concern so the new Chairman could anchor policy expectations. I think we should be looking for other Fed officials to be using the overheating language, and I ask that financial journalists push on this issue further.

The alternative is that Powell went rogue and is ahead of the FOMC. This is possible, but think it unlikely. Still, it did not go unnoticed that Powell was fairly clear about his own position during questioning. In particular, regarding fiscal policy changes:

“I think our view — my personal view — would be that there will be a meaningful increment to demand, at least for the next couple of years.”

and

“My personal outlook for the economy has strengthened since December.”

and

“I wouldn’t want to prejudge that new set of projections, but we’ll be taking into account everything that has happened since December.”

Powell revealed the movement of his own “dot” today. Now, we can all infer the likely movement, to be sure. But his predecessors avoided revealing much information about their own dots in fear that market participants would place a heavy weight on that dot.

Powell appears to be less concerned about such influence. He must know that market participants will shape their expectations on his statements over all others. And that setting those expectations helps set policy outcomes. That suggests three possibilities to me. The first is that Powell intends to shape policy more directly. The second is that Powell is taking more control over the messaging. The third is that Powell revealed more than he intended and will be more circumspect in the future.

I am not going to prejudge any such shift. I have long lamented that Yellen did not take a more public stand on her policy leanings and that the Fed would benefit from a stronger communications anchors. At this point, I only raise the issue that Powell’s approach to his role will differ from his immediate predecessors, perhaps more so than expected.

Bottom Line: What of the implications for policy in the wake of Powell’s visit to Capitol Hill? If the testimony reflects the views of the FOMC, and the FOMC’s concern has shifted to overheating, then the odds are high that enough dots shift up in the next Summary of Economic Projections that the median dot shifts to from three to four (I may have been too sanguine on this issue). Second, the median dot for 2019 will likely shift up to a firm three. But most important is that policy may now be on a hair trigger more than I anticipated.