This keeps going from bad to worse to even more worse. We cannot get around the simple fact that we lack the cornavirus testing capacity to learn the extent of the challenge in the U.S. and implement effective containment and mitigation strategies. That combined with the abject failure of leadership from the Trump administration to begin to develop a comprehensive humanitarian and economic plan to deal with the crisis increases the likelihood of widespread economic damage in the months ahead.

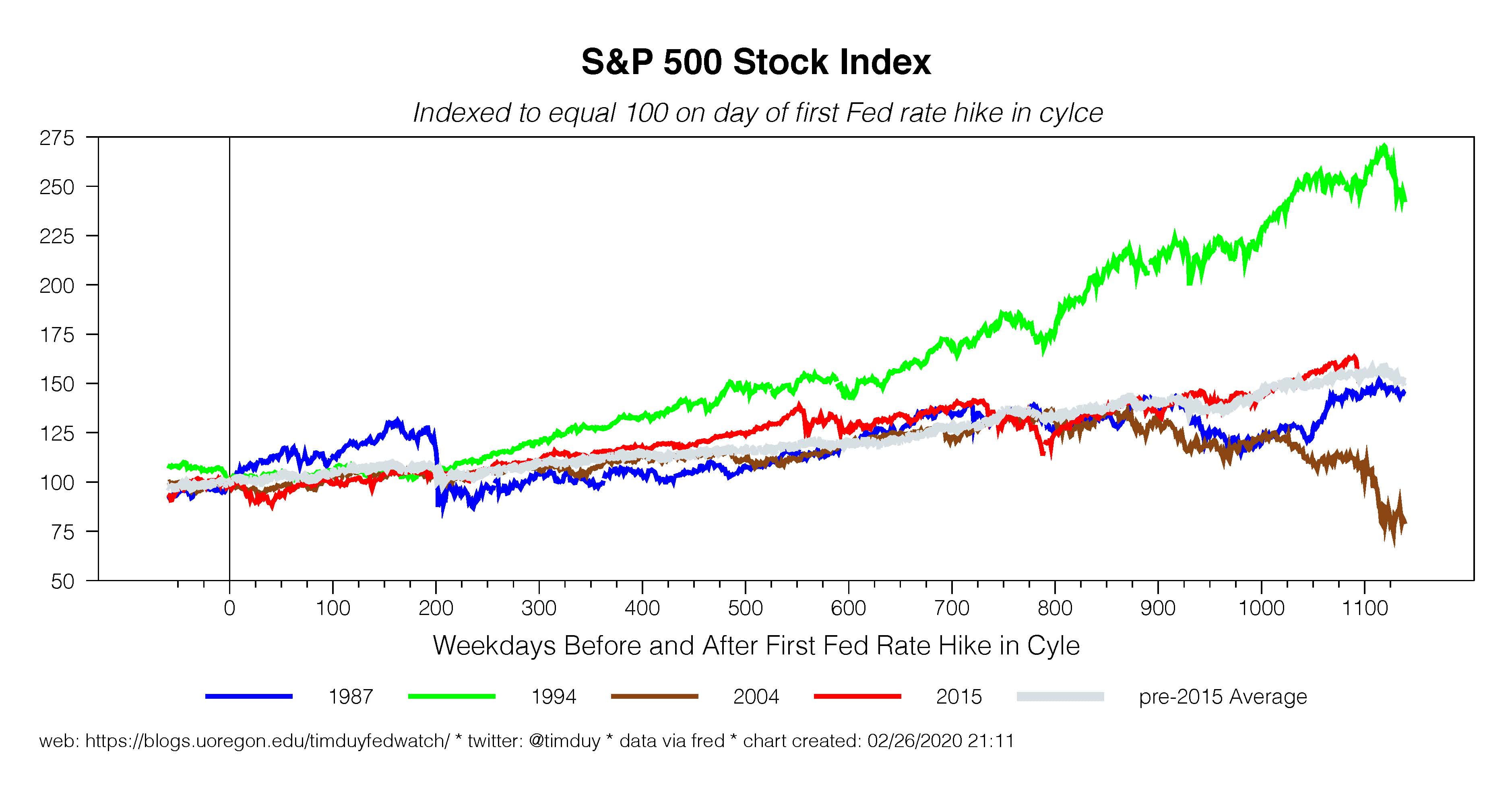

In a resounding vote of “no confidence” in response to President Donald Trump’s Tuesday night address to the nation,equity markets continued to slide on Wednesday with the S&P500 down 9.5%, the worst day since the 1987 crash. Stocks were only briefly supported by the New York Fed’s announcement of expanded market support to include $1.5 trillion of one- and three-month repo offerings across Wednesday and Thursday as well expanding the range of securities included in the monthly $60 billion reserve asset management program. The Fed has yet to cut interest rates again, but will almost certainly lower rates by the end of next week’s FOMC meeting. They should just take rates to zero and get it over with.

The Fed’s actions were intended to “address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak” according to the New York Fed. In other words, they are trying to ensure that the sell-off on Wall Street remains orderly in the sense that market functioning does not become impaired and lead to broad credit contractions. Preventing the turmoil from triggering a systemic crisis is the Fed’s number one goal right now. Eventually, easier policy will support demand more generally, but not until the crisis abates.

Distressingly, futures are red again tonight. It is not realistic to expect the Fed’s action will quickly reverse the slide in equities. The Fed can keep the financial markets functioning, but they can’t make investors buy what they don’t want to buy. Until market participants gain some confidence that they can see the other side of this crisis, they will remain risk averse.

Sadly, we are not yet seeing events that would bolster market confidence and apparently prices have yet to drop to a point where they incorporate all the possible bad news. The most pressing issue is that the virus is out in the wild and time is growing short in many nations to prevent illnesses from overrunning their health care systems as happened in Italy.

The rising acceptance of social distancing measures is a promising sign with corporations and sporting leagues taking the early and bold steps. State and local efforts are lagging. The slow decisions to close schools, for example, may prove disastrous in many communities. As Italy and Wuhan have proved, letting the problem fester only raises the overall costs of responding to the virus.

Markets may get some relief from fiscal policy, but I wouldn’t anticipate sustained gains just yet. The administration continues to dither while House Democrats push forward a fiscal policy response. Some combination of paid sick leave, increased unemployment benefits, Medicaid funding, and free testing appears to be in the works; we don’t yet know what will be acceptable to the Senate and the White House. This is likely to be only the initial package; I suspect (hope?) more direct cash aids to households will be coming.

Bottom Line: At the moment, market participants can’t see beyond the immediate crisis and continue react rationally to the flow of bad news. The Federal Reserve will do what it can to support markets and the economy – it’s the only game in town at the moment – but we all know it in the longer term it is playing a supporting role. The leading role falls to the fiscal authorities to craft a response to the humanitarian crisis and the economic cost. So far, the response has been woefully lacking.