Do not become obsessed with recent Fed speak pointing in the direction of early tapering or rate hikes. The Fed is not shifting gears absent a clear justification from the data and that justification is still lacking. That said, given the changing political landscape, the accelerating pace of vaccinations, the most recent fiscal bridge, and the surplus of pent up savings, it is completely reasonable for market participants to prepare for a more widespread shift in sentiment among Fed speakers regarding the asset purchase program. That shift likely won’t happen until the second half of the year.

Let’s start with the baseline, again: No tapering this year, no rate hikes before 2023. Is there widespread support for the baseline among Fed officials? Yes. Kansas City Federal Reserve President Esther George today said:

Clearly, in the current environment where the economy continues to heal, an accommodative policy stance is appropriate. It is too soon to speculate about the timing of any change in this stance.

As of now, George lacks reason to believe the Fed needs to consider a new policy approach. That though doesn’t mean the path is fixed:

As the data come in, and the economy evolves, the public and markets should be able to adjust their expectations regarding the policy path.

That’s where I am trying to keep the focus – how might the data evolve and what does it mean for policy? Similarly, consider this from Cleveland Federal Reserve President Lorretta Mester, via Reuters:

“I think it’s very premature to think that we’re getting to the point to change our policy stance,” Mester said. “I think we have to get through this surge.”

This syncs with the general view within the Fed that later this spring – after the Covid-19 numbers are on the way down and vaccinations increasingly widespread – will be the time to revisit policy options. St. Louis Federal Reserve President James Bullard had nearly identical comments, via Bloomberg:

“We want to get through the pandemic and sort of see where the dust settles, then we will be able to think about where to go with balance-sheet policy,” Federal Reserve Bank of St. Louis President James Bullard said Tuesday during an online interview with the Wall Street Journal.

That’s the baseline story coming from the Board of Governors as well. In general, speakers tend to avoid speculating too specifically on how the Fed might react to data that deviates substantially from the forecast. In contrast, Atlanta Federal Reserve President Raphael Bostic captures the news cycle because he does entertain scenarios substantially different from the current forecast. Via an interview with the Atlanta Constitution Journal:

If (the economy) comes back super-strong, it’s warranted to start having a conversation about how we get out of our more emergency position stance in terms of providing support and get back to a more normalized asset purchase stance and interest rate stance…That conversation will happen over a longer period of time, but I think our experience has been that we should signal that we are talking about these things well before we’re planning on actually making the move. As I see evidence that the economy is coming back a bit stronger and we can pull back on the some of the stimulus that we’ve put into the economy, I am going to want to start having that conversation.

Bostic sounds as if he is expecting strong data, and he is:

I am fairly optimistic that the rebound is going to be fairly strong and I want people to understand that, if we see that strength, then the natural progression from that is to say, what’s our trajectory from that to move to a more neutral position.

Bostic’s optimism may be excessive, particularly on inflation. He has pondered the possibility of a rate hike in late 2022 which, under the Fed’s new framework, implies sustainable inflation in excess of the Fed’s target to emerge sometime in the first half of next year. That seems premature. Possible, but premature.

I wonder that Bostic has become the focus of attention because his economic outlook of surprising strength later this year matches the growing sense among market participants that the year will be much stronger than the median Fed meeting participant anticipates. Market participants are rightly looking past this winter and seeing many tailwinds on the horizon. Bostic is telling you that those tailwinds materialize, you should be expecting a healthy Fed debate about the path of policy latter this year.

It’s not really a secret that I am optimistic on the path of the economy this year. That said, I don’t anticipate it will be sometime in the third quarter before the Fed has the data to justify considering a policy shift. I would expect Bostic’s colleagues to mimic his policy outlook should that optimism be realized.

I view Bostic’s comments as very different from these by Dallas Federal Reserve President Robert Kaplan, via Bloomberg:

“My concern is if we get to 2023, for example, and we have unemployment rates below 4%, in the 3s, and we still haven’t quite reached our 2% inflation objective, I might well be supportive at that point of being accommodative or even highly accommodative, I don’t know that I’ll think it’s appropriate to be keeping the fed funds rate at zero, though,” Kaplan said.

I can put Bostic’s comments into the context of the Fed’s new policy strategy. Kaplan, however explicitly states that possibility of hiking rates before the Fed reaches the 2% inflation target. That is a very minority position on the Fed and likely requires some substantial financial stability risks that could not be managed via regulation.

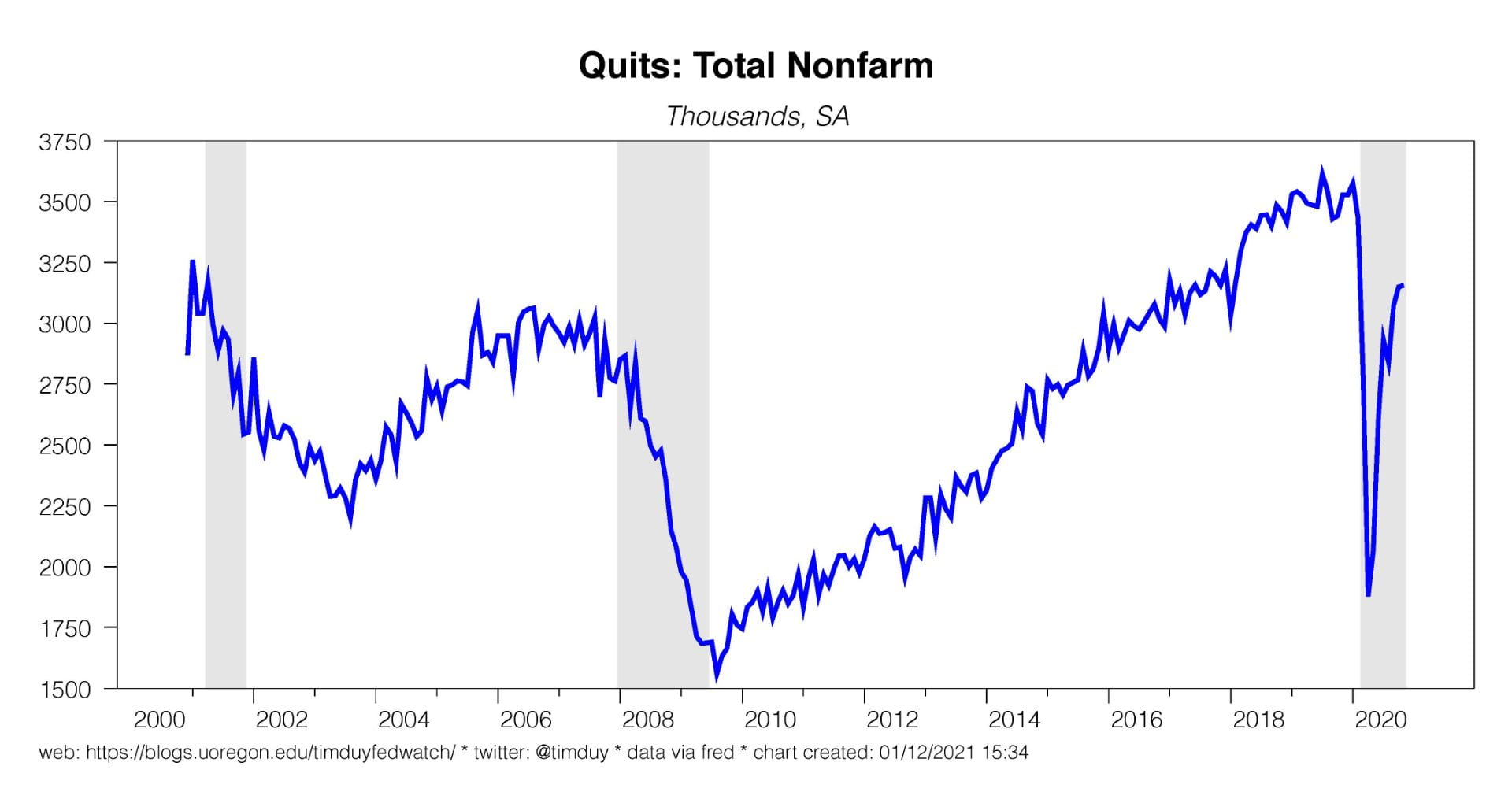

Separately, JOLTS data for November showed little change in opening or quits:

The story of this report is the resilience in the job market in comparison to the last recovery

Bottom Line: Fed policy is on autopilot for now. Bostic’s comments don’t change that. Bostic’s comments, however, are a preview of what’s to come if his optimistic forecast comes to pass.