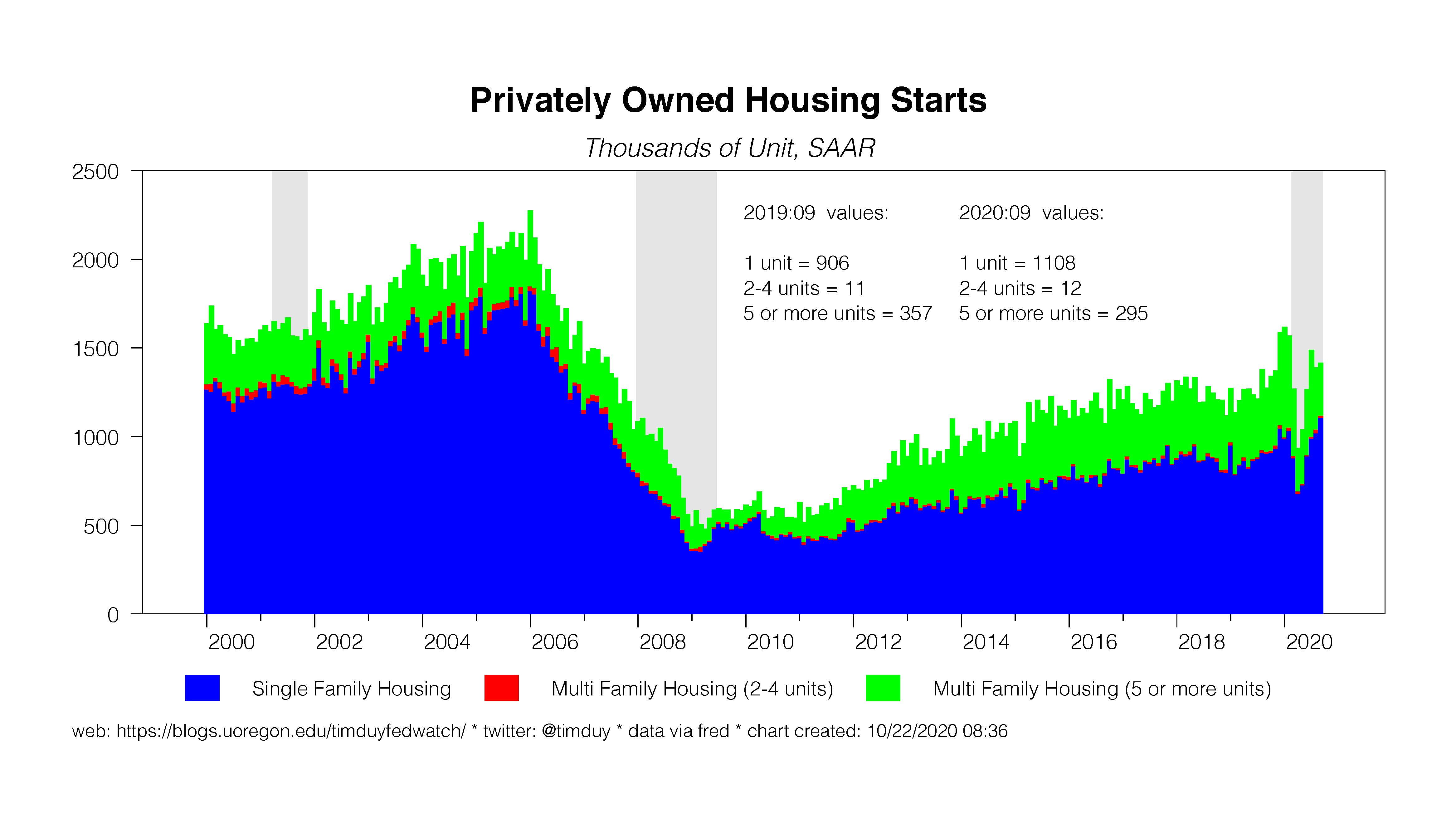

The U.S. housing market continues to steam along on the back of demographic trends and low interest rates. Single family starts rose in September, compensating for a decline in multi-family:

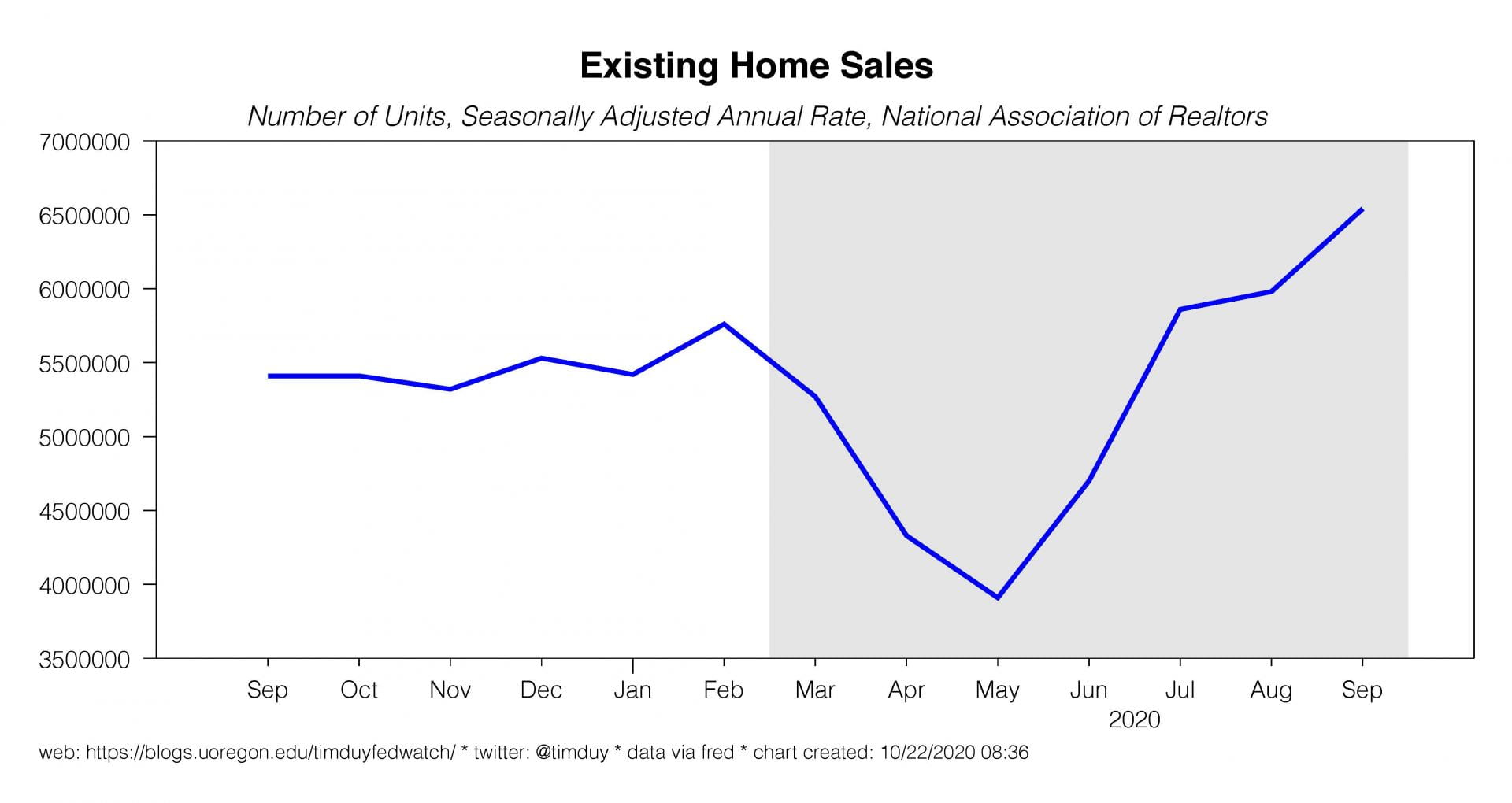

The primary support for this market is Millennials aging into their home buying years; the pandemic and low rates are just pushing the marginal buyers over the edge. Existing home sales also moved sharply higher:

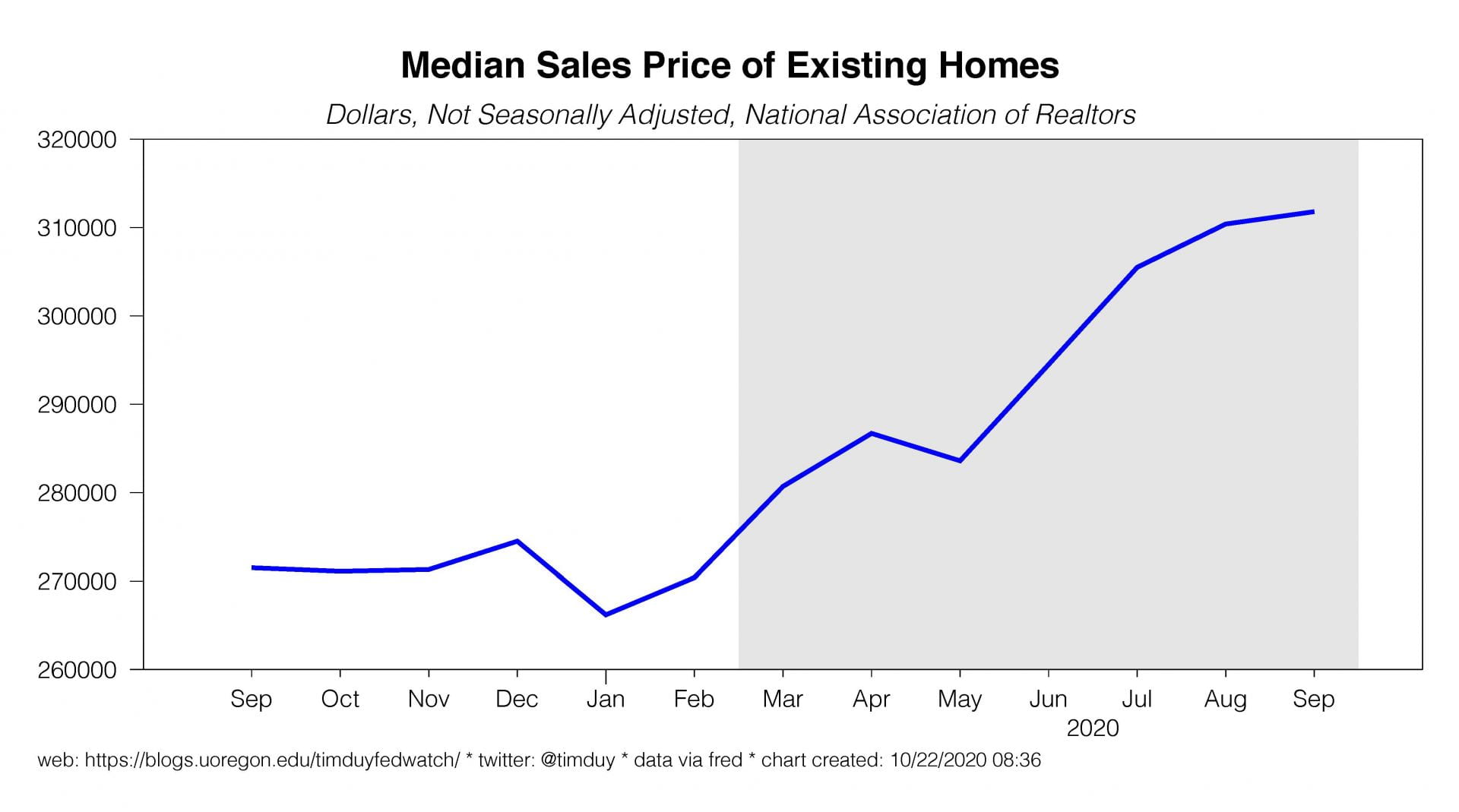

Remember that even existing home sales create a downstream impact on durable goods consumption and residential investment (remodeling). With inventory tight (just 2.7 months of supply), prices continue to climb, up 14.8% over last year:

Household wealth will continue to rise. Speaking of tight markets, the Wall Street Journal has a fun story on the crazy contingencies in housing contracts now occurring:

In central Oregon, real-estate agent Chris Sperry has also played peacemaker. Ms. Sperry represented a buyer and seller in a transaction where the buyer insisted she wanted the seller’s cat along with the house. The seller balked.

“It really got into a heated argument on both sides,” she says. The seller finally agreed to leave her cat, and Ms. Sperry bought her a replacement kitten.

This week we get the third quarter GDP report. Expectations are high with Wall Street expecting a 31.9% gain and the Atlanta Fed expecting 35.2%. I am not inclined to agonize over the exact number as it is all too easy to lose sight of the forest for the trees. The wild swing in the data tell us that U.S. economy shut down in the second quarter and reopened in the third. This isn’t new information. The rebound in activity will still leave the economy operating below pre-pandemic levels. Part of this can’t be helped due to the nature of the pandemic, another part is self-inflicted due to lack of preparation on issues like opening schools. Presumably the latter could still be addressed but won’t be until (hopefully) after the election. We know this story at this point.

We have already turned the page on the third quarter. What we really care about is the pattern of recovery going forward as the after-effects of the start-stop dynamics play themselves out. Can the economy sustain upward momentum? Is the recovery self-sustaining even without additional fiscal stimulus? To get at those questions we need to start thinking about the October data.

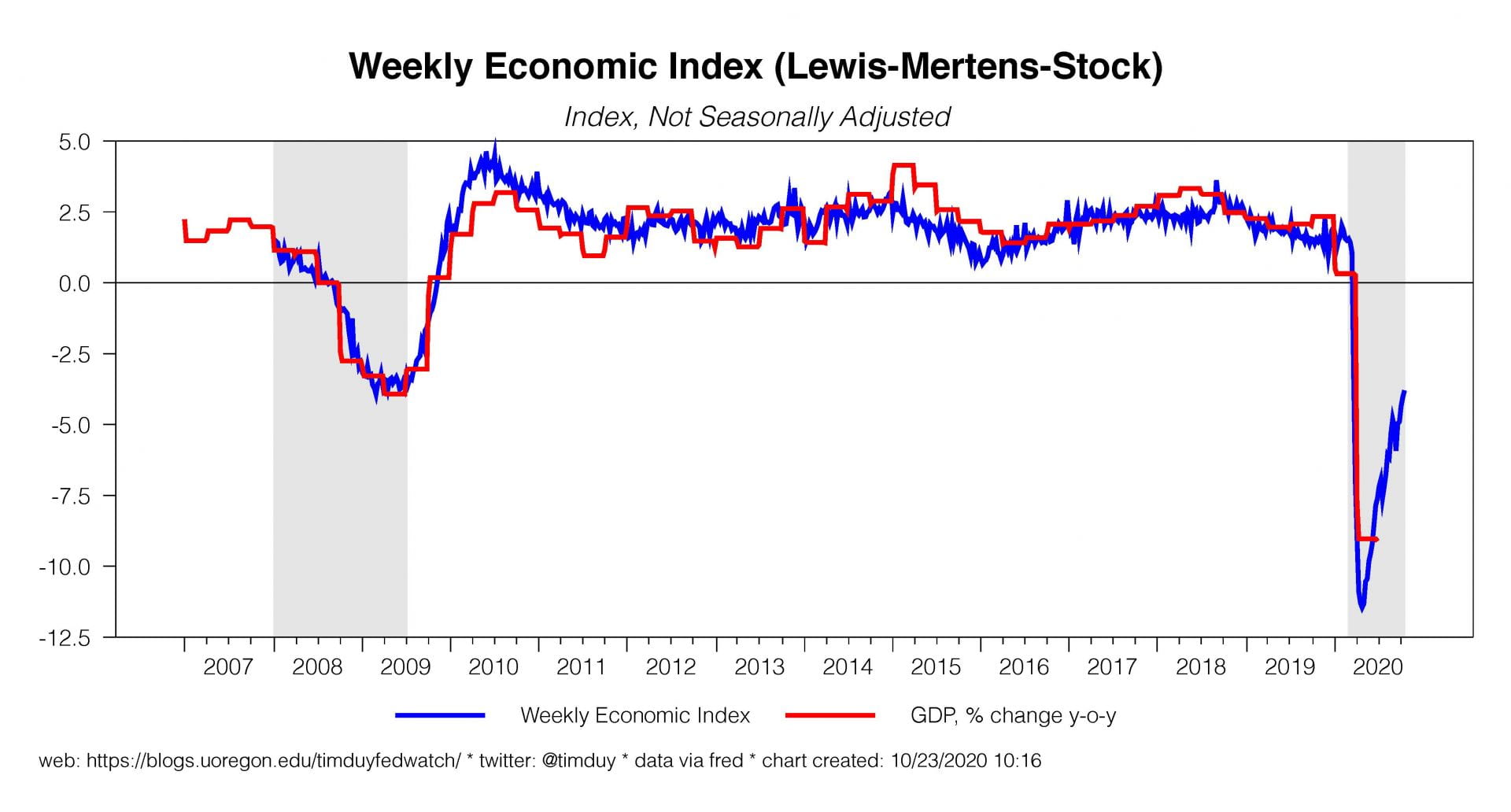

One metric that has traditionally tracked year-over-year trends in GDP growth fairly well is the New York Fed’s Weekly Economic Index (WEI):

I tend to care about the year-over-year GDP trends more than the quarterly growth rates; the latter are subject to excessive noise that can overwhelm the underlying signal. The WEI regained its momentum in October. This is important for two reasons. First, it indicates that the general upward trend in the economy continues into the fourth quarter. Second, note that the index accelerated in October despite now going on the third full month since the end of enhanced unemployment benefits in July. This suggests that the expansion remains resilient to the reduction in fiscal support.

Similarly, the IHS/Markit PMI flash report for October indicates that the fourth quarter is getting off to a solid start:

U.S. output growth regained growth momentum in October, as business activity rose at the fastest rate for 20 months and business optimism improved markedly. The upturn was largely driven by service providers, though manufacturing firms also reported a further solid increase in production.

That said, watch for another trend: Slower job growth:

Reflecting softer pressure on capacity, firms increased their workforce numbers at a slower pace in October. The rate of employment growth was faster than the series average, but dipped to a three-month low…

… manufacturers registered a slower rise in employment in October. Some firms, however, stated that difficulties finding suitable candidates weighed on their ability to hire.

I am not going to start in on the lack of suitable candidates; from such random comments I can’t tell you what is firm specific, industry specific, a broader structural issue, or just a firm looking for a “unicorn” employee. I need more information. The slower job growth though is relevant and matches this from Ernie Tedeschi:

Meanwhile, my attempt to forecast payroll employment with UI claims as well as data from Homebase and Kronos suggests employment rose by +1.1 million in October not-seasonally-adjusted. That’s consistent with the HPS. That should be consistent with ~+360K seasonally-adjusted https://t.co/FDnQKPCCfV pic.twitter.com/mNK6oLiDHG

— Ernie Tedeschi (@ernietedeschi) October 23, 2020

The September job growth number was 661k overall, 877k private. The slowdown in job growth would be consistent with a baseline expectation that this recovery follows the patterns of recent cycles in which job growth settles into a pace that closer to 200k/monthly until the economy can be freed from the pandemic.

I find this particular interesting in light of the fiscal support to households this year. I am still in shock by the magnitude of the support:![]()

My prior was that a fiscal shock of that magnitude would have had much longer legs; I would not have anticipated the dramatic accumulation of savings given the initial severity of the downturn. Seems like that prior was just wrong. This suggests to me that the support was not particularly well targeted (I would prefer state and local aid over tax rebates). That’s fine, we were faced with a unique event deserving of the kitchen sink. But the lack of effective targeting would explain why the economy seems to have weathered the July fiscal cliff.

And then there is the next big question. How well we weather the surge in Covid-19 cases? There is no national leadership at this point. A new cluster of cases has been reported in the orbit of Vice President Mike Pence, the supposed head of the coronavirus task force. White House Chief of Staff Mark Meadows admitted the administration is no longer trying to contain the virus (my belief is the Trump administration is just hoping to leave Biden with as big a mess as possible). Cases are surging across the Midwest. Utah hospitals are close to rationing care. Europe is careening out of control. Remember when Europe was the model? Good times. Even China has a fresh outbreak.

In the U.S., the lack of national leadership suggests a national lockdown is unlikely; I anticipated rolling increases and decreases in the level of restrictions on a local level. I doubt indiscriminate lockdowns are politically feasible, especially for a population struggling with virus fatigue. My experience is that the fatigue cuts across political lines at this point.

We have a busy week ahead, even before the already mentioned GDP report on Thursday. Monday we get another reading on the housing market with new home sales for September; expectations are for 1,025k compared to 1,011k the previous month. Durable goods orders come on Tuesday; to date, core manufacturing orders have exceeded expectations and are expected to be up another 0.5% in September. Note that that the series has considerable monthly volatility; keep focused on the underlying trend. Friday we get some follow up to the GDP report with the September income and outlays report which also contains PCE inflation for the month. Also arriving is the employment cost index for the third quarter and the final Michigan consumer sentiment numbers. Blackout week for the Fed.

That’s it for this morning. Good luck and stay safe!