Federal Reserve Vice Chair Richard Clarida gave an interesting speech today. His take on the current situation sounds very optimistic:

…This recession was by far the deepest one in postwar history, but it also may go into the record books as the briefest recession in U.S. history. The flow of macrodata received since May has been surprisingly strong, and GDP growth in the third quarter is estimated by many forecasters to have rebounded at perhaps a 25 to 30 percent annual rate. This development is especially noteworthy when set in relief against the surge in new COVID-19 cases that were reported this summer in a number of U.S. states and the coincident flatlining in a number of high-frequency activity indicators that we follow to track the effect of the virus on economic activity.

Although spending on many services continues to lag, the rebound in the GDP data has been broad based across indicators of goods consumption, housing, and investment…

Notable points include that 1.) Clarida reasonably thinks the technical recession is over (it is), 2.) his reference to GDP forecasts sounds on the pessimistic side; Atlanta Fed is estimating 35.2%, 3.) rising Covid-19 cases are impacting the high-frequency indicators but not traditional measures, suggesting to me that we need to be careful with the former, and 4.) unsurprisingly, the weak spot is now in services, particular those impacted by the need for increased social distancing.

Possibly more importantly is the optimism in his longer-term outlook:

…the COVID-19 recession threw the economy into a very deep hole, and it will take some time, perhaps another year, for the level of GDP to fully recover to its previous 2019 peak. It will likely take even longer than that for the unemployment rate to return to a level consistent with our maximum-employment mandate. However, it is worth highlighting that the Committee’s baseline projections summarized in the most recent Summary of Economic Projections foresee a relatively rapid return to mandate-consistent levels of employment and inflation as compared with the recovery from the Global Financial Crisis (GFC).

Yes, this is not the same as the expansion that follow the GFC. This is a different expansion. What does the overall outlook mean for policy in the context of the new policy approach? Clarida provides a cryptic answer:

It will take some time to return to the levels of economic activity and employment that prevailed at the business cycle peak in February, and additional support from monetary—and likely fiscal—policy will be needed.

He clearly says “additional” support from monetary policy “will be needed.” I take this as a hint that the Fed is gearing up for something new in the coming months. Given that they have dismissed yield curve control, he might be thinking of shifting the composition of asset purchases further out the yield curve.

Also, note that Clarida says that additional support for fiscal policy is only “likely” needed, a downgrade from Federal Reserve Chair Jerome Powell’s consistent requests for more fiscal stimulus to support the economy. Why might Clarida be more cautious? First, his optimistic take on the data flow as noted above. Second, this via MarketWatch:

“We have a lot of accumulated saving and I think that will be a tail wind for the economy when we get to the other side of this,” he said.

It’s starting to sink in that not only is the economy on a sustainable upward path, much of the stimulus money was saved and is available to support demand when confidence rises.

Tomorrow we get the initial claims data. Last week I argued that the initial claims data likely overstated the weakness in the labor market. Today we received this via Bloomberg:

California’s numbers on unemployment claims are set to remain frozen at prior levels in Thursday’s national report and potentially longer, extending distortions that some economists were expecting to subside after the state ended a two-week pause on filings…

…But the state’s claims will continue to be estimated in national figures — using the numbers from the week before the pause in mid-September– until the figures normalize, which could take two to three weeks, the Labor Department said in response to questions from Bloomberg News.

Approach the claims data with caution.

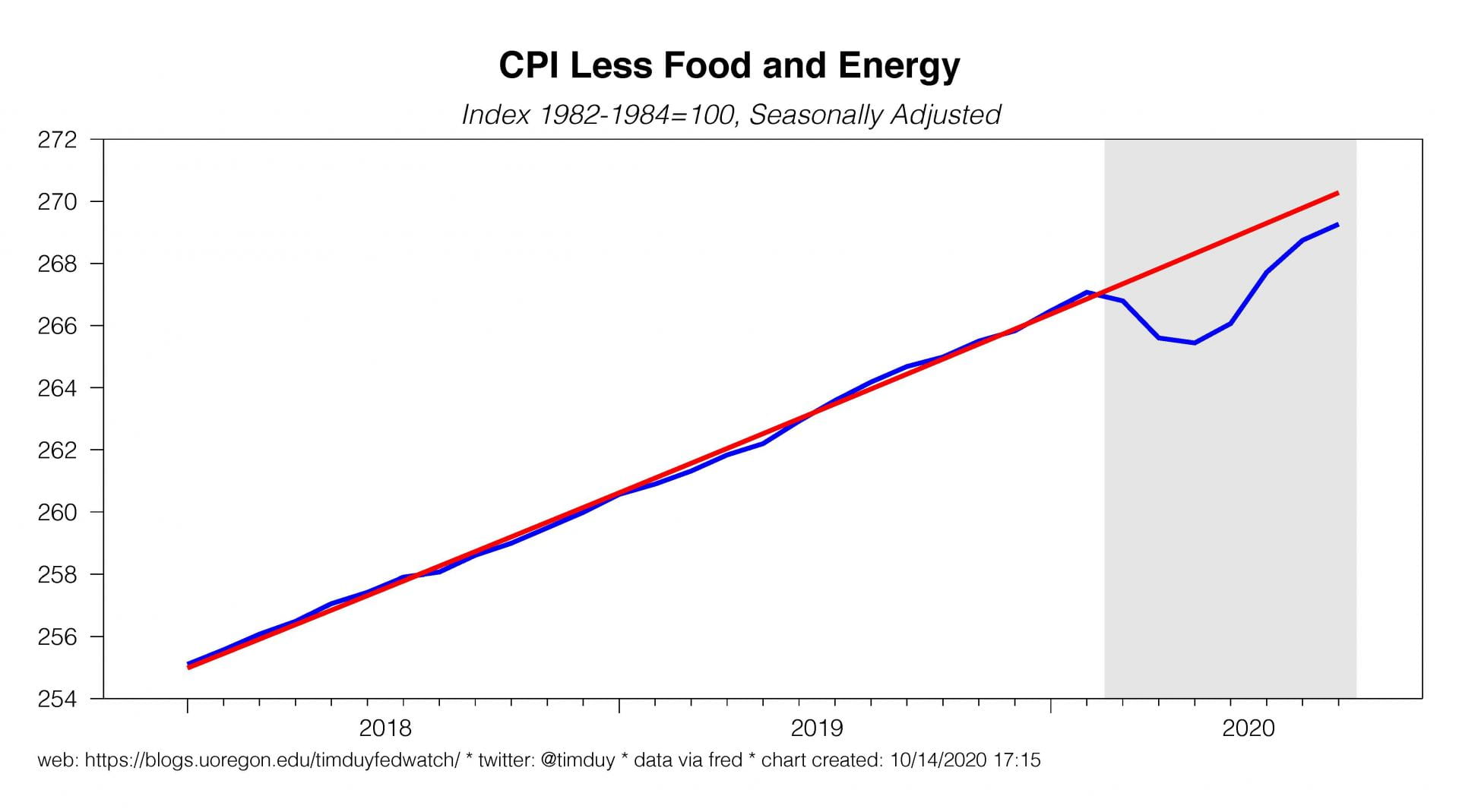

From earlier this week, CPI inflation moderated further, falling to a more typical 0.2% month-over-month gain:

If it settles back into the pre-pandemic trend, the level won’t regain its previous trend:

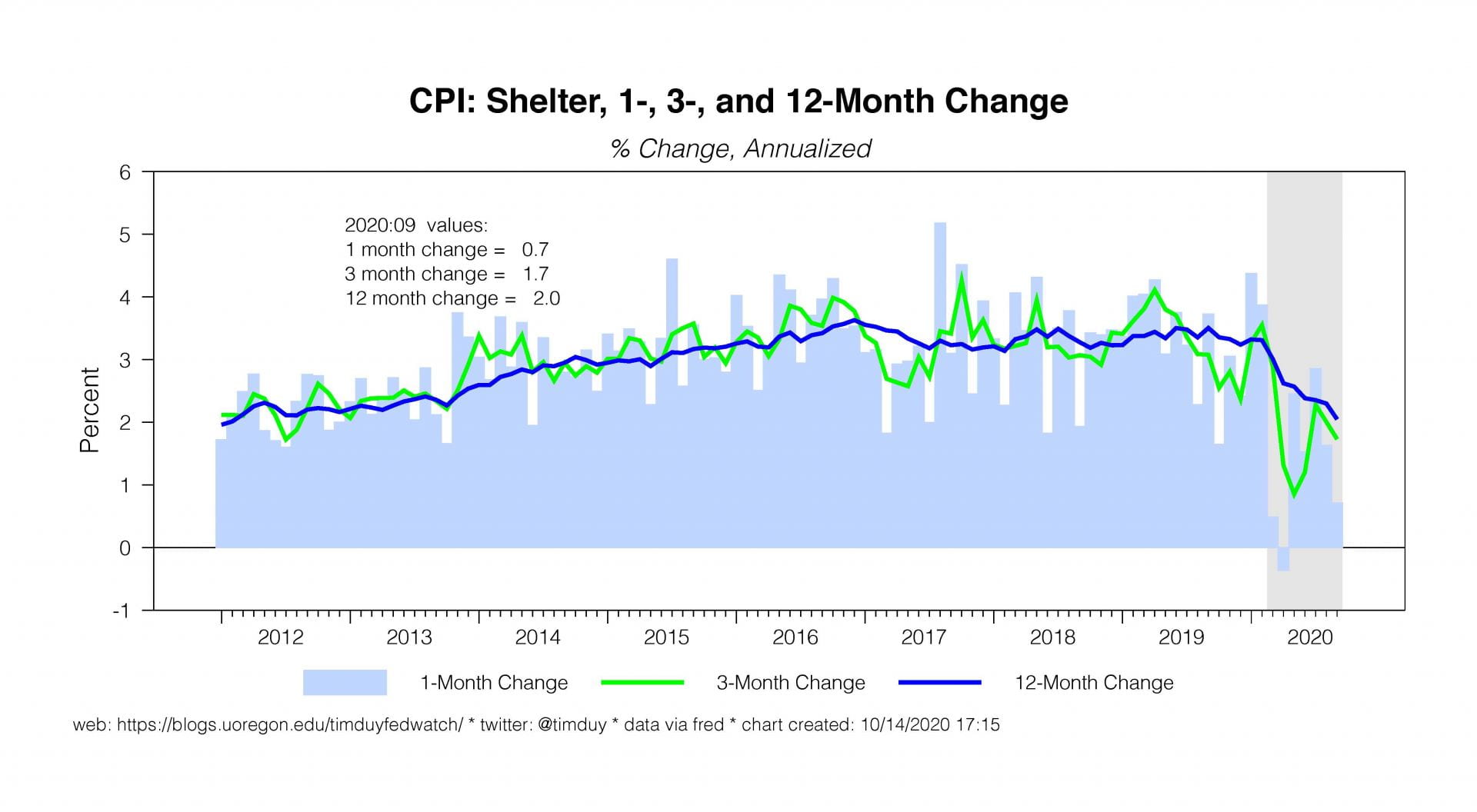

It’s tough to see a substantial acceleration with shelter inflation still weak:

This is the kind of data that keeps the Fed committed to low rates for the foreseeable future even as the economy gains ground.

Finally, this week we get the retail sales report for September. Keep your expectations realistic. In aggregate, retail sales have already returned to trend:

Will retail sales push above trend? One risk here is the headlines scream “Retail Sales Slowing as Economy Falters.” The reality is that growth will slow if we regain the previous trend line and it has nothing to do with a faltering economy. An alternative risk is that you can tell a story of how retail sales rise to persistently above trend if the supply-side of the pandemic that still encumbers part of the economy pushes demand into the retail sales sector.

That’s it for today. Good luck and stay safe!