Another week with slow progress in the initial claims data. Via Bloomberg:

The number of Americans seeking unemployment benefits fell for a second week while remaining elevated, as the labor market makes scant progress amid risks of further weakness without additional federal stimulus.

The general reaction is like this via the Wall Street Journal:

“It’s more of the same, but it’s also still jaw-dropping that we have that many new claims even now as we’re six, seven months into this whole recession and recovery,” said Eliza Forsythe, an economics professor at the University of Illinois, Urbana-Champaign.

Yes, the claims data is jaw-dropping. But is it right? That’s an important question. A considerable amount of analysis is hanging on the initial claims data, including the prediction that these numbers prove the economy is heading for collapse now that the enhanced unemployment benefits have expired. If the claims data is just broken, those predictions are just wrong.

We should be more skeptical about the initial claims data. Notice that the economy went off the fiscal cliff more than two months ago and yet still seems to be recovering. We went off the fiscal cliff yet auto sales and housing are booming? Doesn’t that just seem wrong? And shouldn’t the data from California be more of a red flag than it has been? Via Bloomberg:

The report came with the same major caveat as last week: The figures from California, the most populous state, used numbers identical to the previous week because the state temporarily halted acceptance of new applications for two weeks to improve its systems and address a backlog of filings.

We know that the states were completely unprepared for the wave of claims that hit this spring. We don’t know however how deeply that damaged the data. The overwhelmed systems were likely more vulnerable to fraud as well.

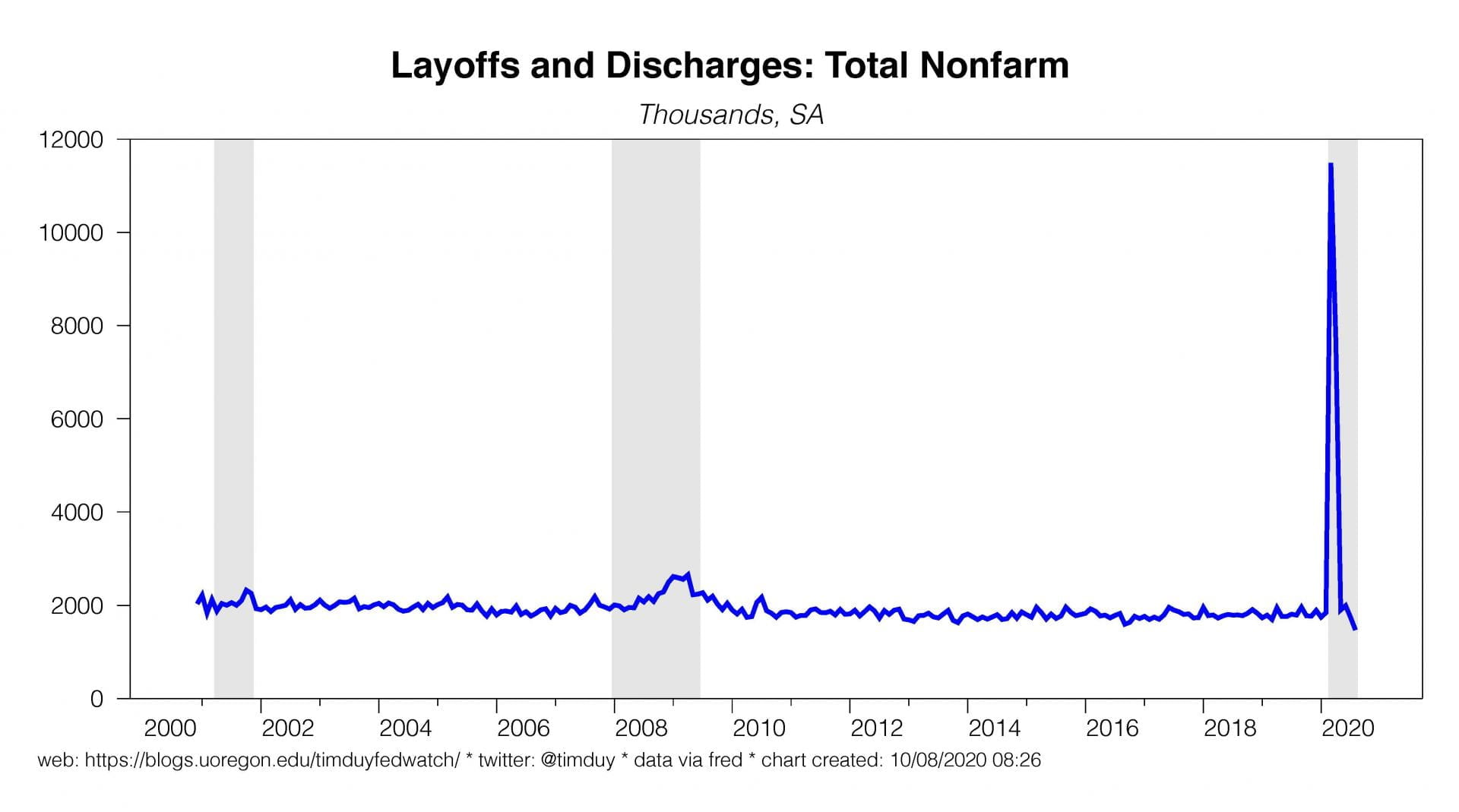

What really struct me this week was this red flag from the JOLTS report:

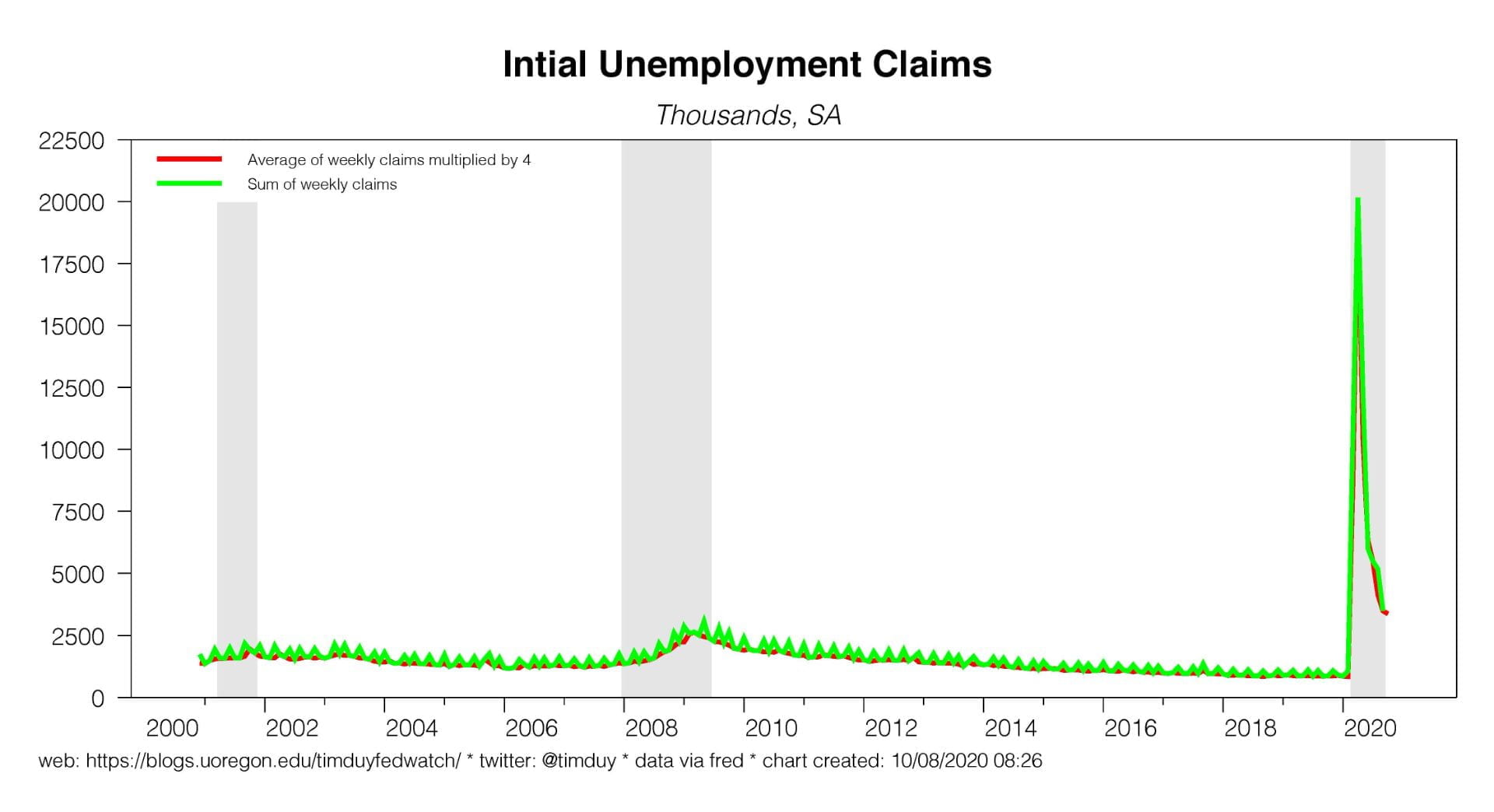

How can layoffs and discharges have collapsed to pre-pandemic levels despite the persistently high level of initial claims? Let’s compare the two series. JOLTS is monthly while claims are weekly. To reconcile the two, I first took the average of claims over the month and multiplied by 4 and then compared it to the sum of weekly claims. The sum of weekly claims is noisier but the resulting two series are qualitatively identical:

For ease of exposition, I decided to use the smoother series.

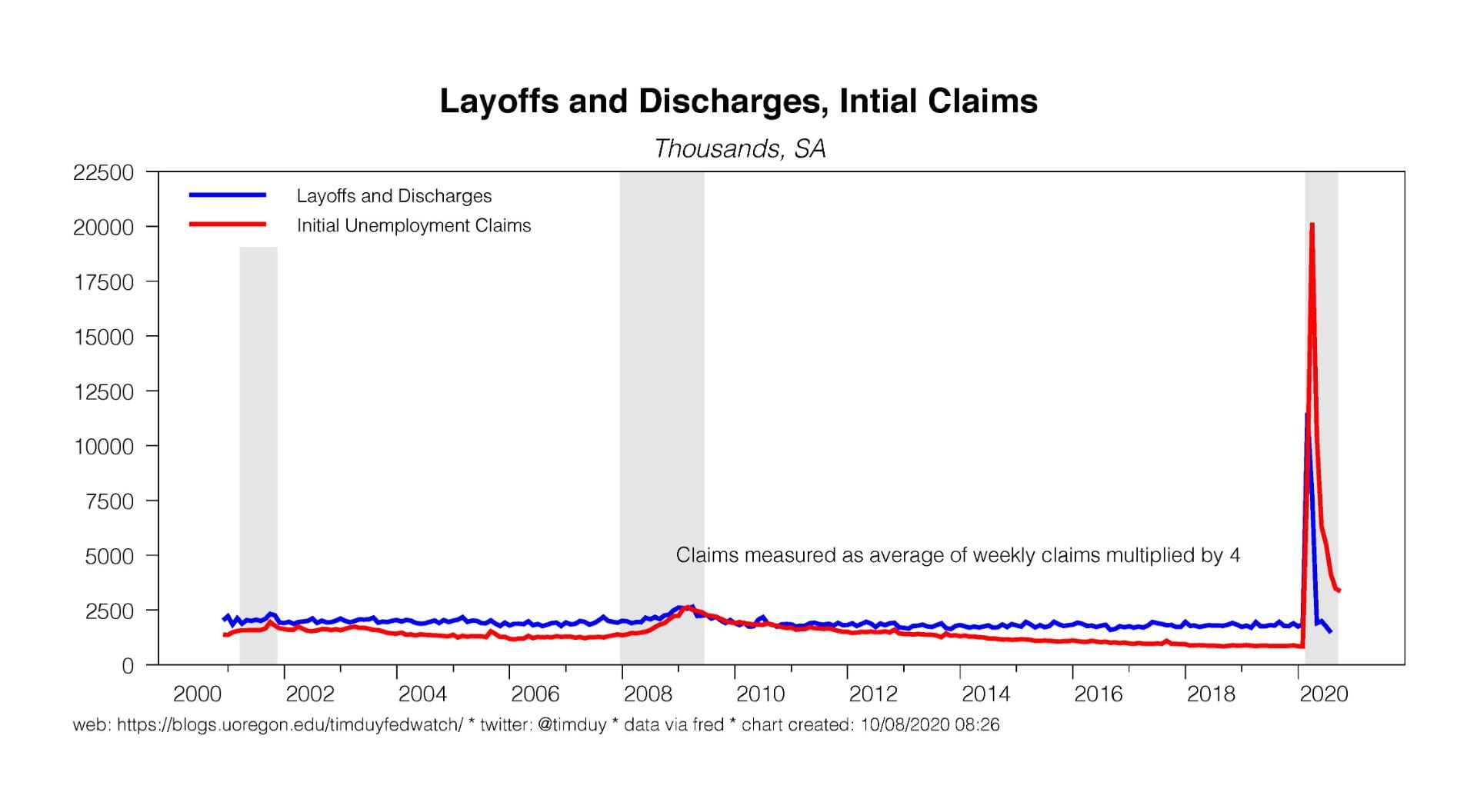

Prior to the pandemic, the initial claims and layoffs/discharges were closely aligned:

Layoffs and discharges closely align with initial claims during recessions but deviate away from recessions (discharges not related to layoffs are a larger proportion of separations outside of recessions). During the pandemic, however, claims have surged above layoffs and discharges:

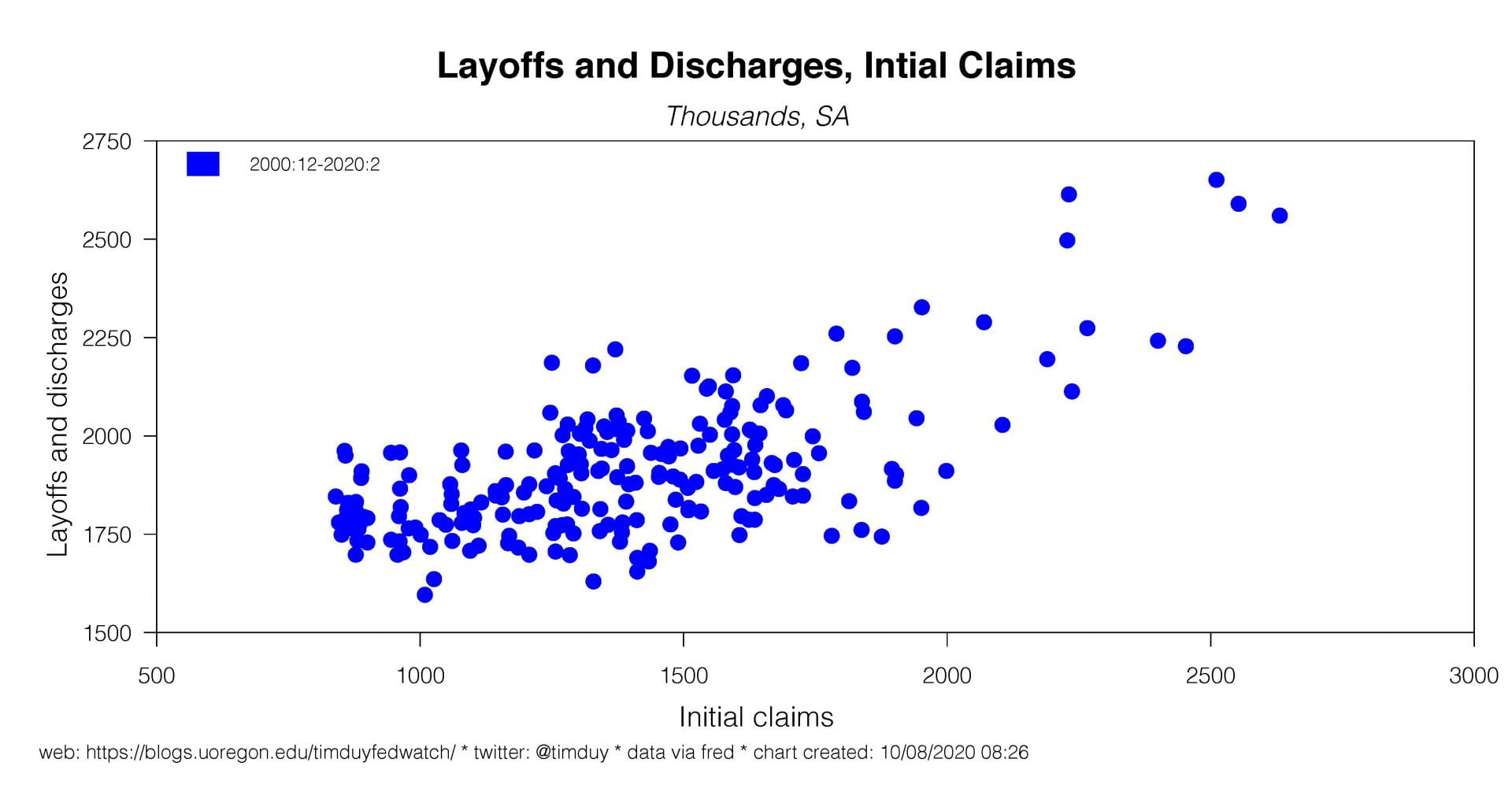

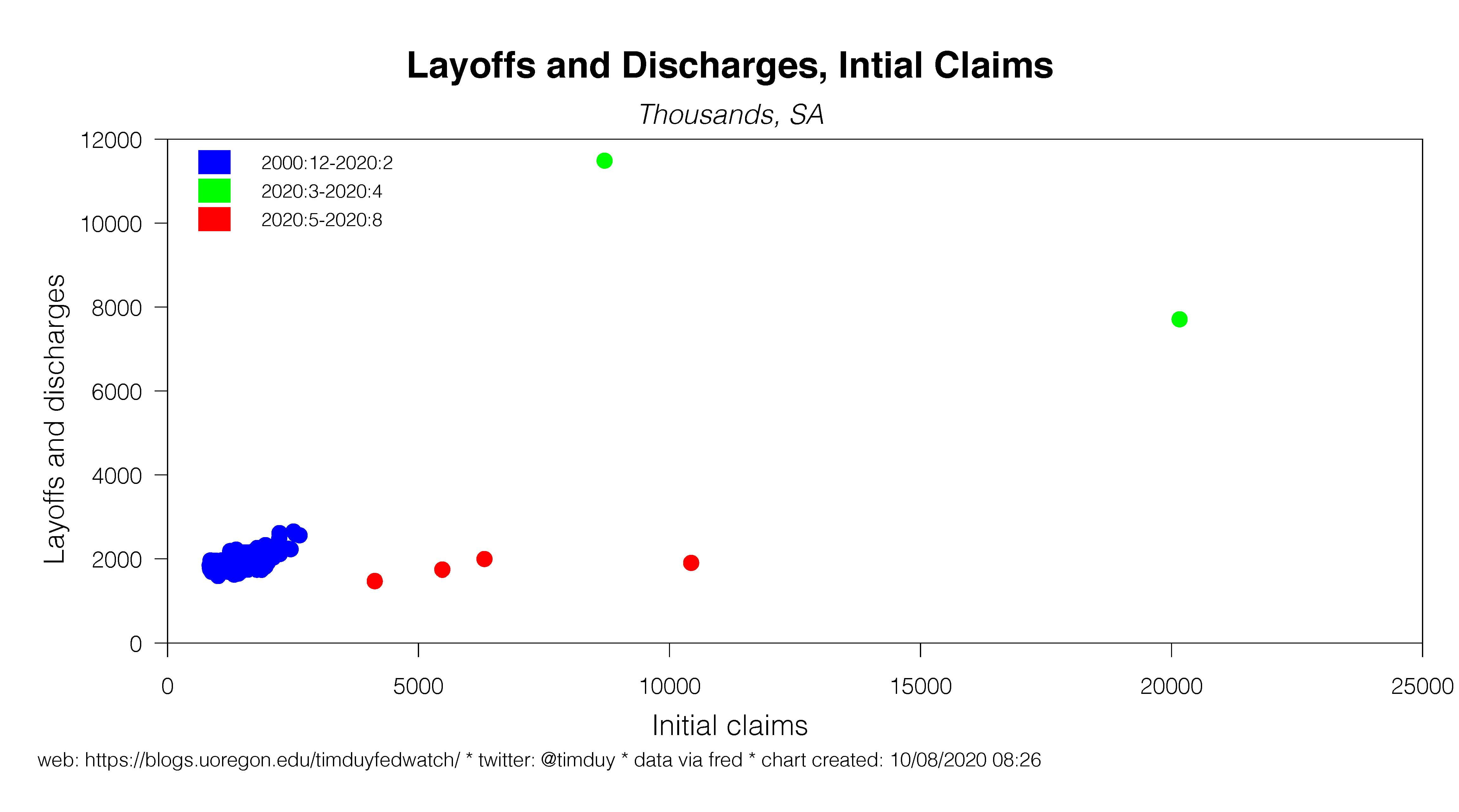

For a different view, consider the pre-pandemic scatterplot:

versus the post-pandemic scatterplot:

Initial claims are just way too high relative to the level of JOLTS discharges and layoffs. Which series are you going to believe? True, the JOLTS data may have some pandemic-related challenges. Still on net, I think you have to give the benefit of the doubt to the BLS economists on this one as we have plenty of reasons to believe the claims data is corrupted.

Needless to say, the layoff and discharges series is telling a wildly different story than the claims data. It is a story that doesn’t match the conventional wisdom. For what it’s worth, I believe there is a strong institutional incentive for forecasters to not deviate from the conventional wisdom. A younger forecaster can more easily be outside the conventional wisdom relative to an older more experienced forecaster. If you are wrong, you are just young and inexperienced. If you are right, you just made your career. As forecasters age, they tend to drift toward the consensus for safety. Better to be wrong together than wrong alone. I also sense that in the current environment a forecaster might also be under social pressure to signal their political inclinations via their forecast.

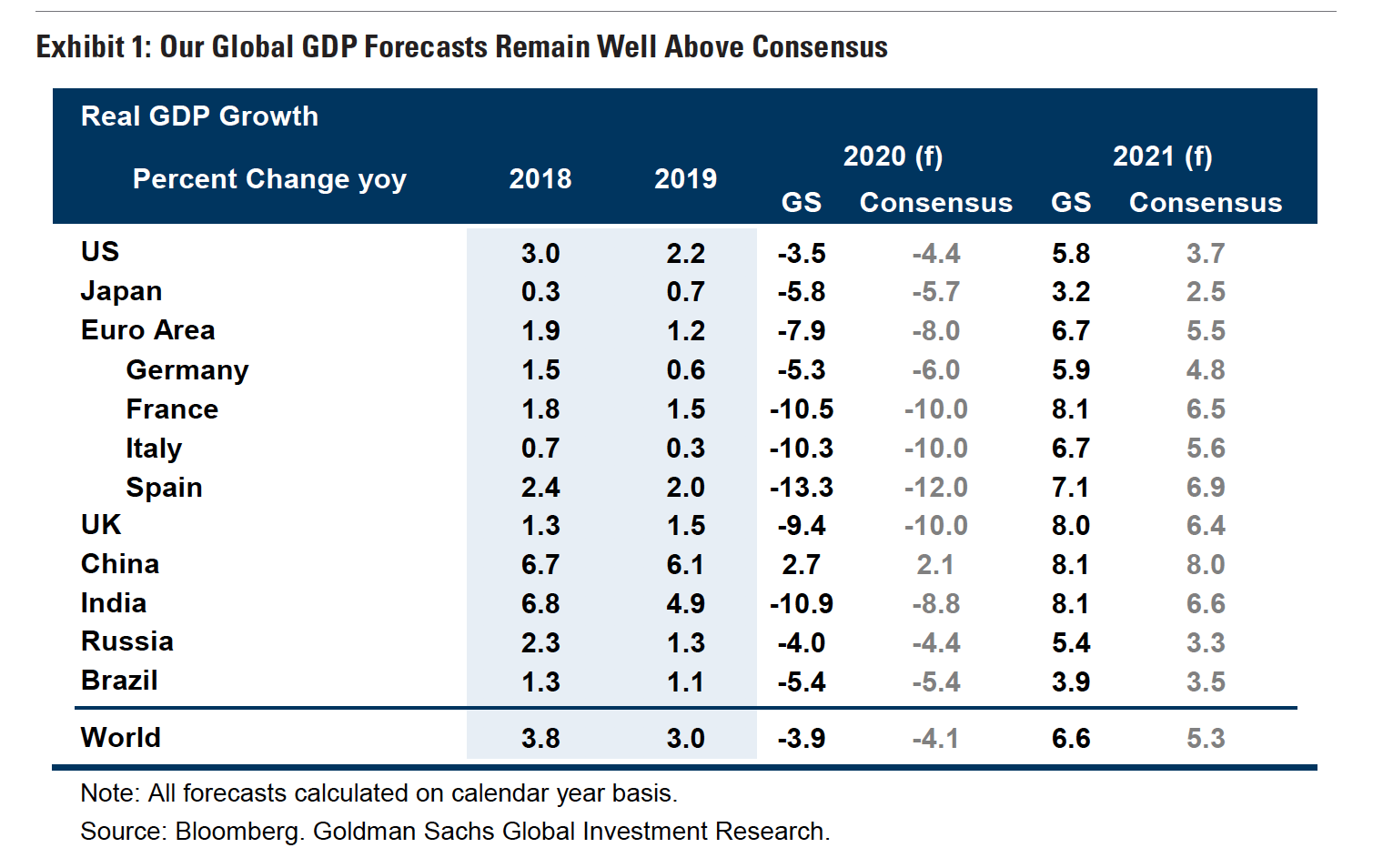

One exception to this rule right now is Jan Hatzius at Goldman Sachs, whose 2020 and 2021 growth forecasts are decidedly above consensus:

Bottom Line: I think we should be much more skeptical of the initial unemployment claims data. If you switch your analysis to the the layoffs and discharges series, the world looks very different. A lot of the conventional wisdom is tied to the claims data. The claims data lets you view the current environment as a repeat of the last recovery. If the claims data is deeply corrupted, the conventional wisdom is just plain wrong. I keep saying the same thing: This isn’t the 2007-09 recession or the 2009-2020 recovery. It’s something different.