I don’t know what to tell you. Seriously. Our government just seems to want to inject additional risk into an already troubled situation.

In some ways, it’s all straightforward. We deliberately brought the economy to a stand-still. We got behind the curve on the Covid-19 virus and really didn’t have much of a choice but to shut it all down. The immediate outcomes were fairly predictable. Employment dropped sharply and household spending plummeted. We know the former already via initial jobless claims and employment reports and we get another round of negative news on that front this Friday. Last week we saw how deeply spending plummeted in April. Not pretty:

Still, not unexpected. The entire point of the shutdowns was to choke off activity by keeping people at home. And there was something of a plan to deal with the economic fallout, albeit a bit of a haphazard plan. That plan too was in some ways simple: Pump income into households via a variety of mechanisms to, in simple terms, keep the money flowing in the economy. And that too was successful, at least at a macro-level. Transfers more than compensated for lost wages and salaries:

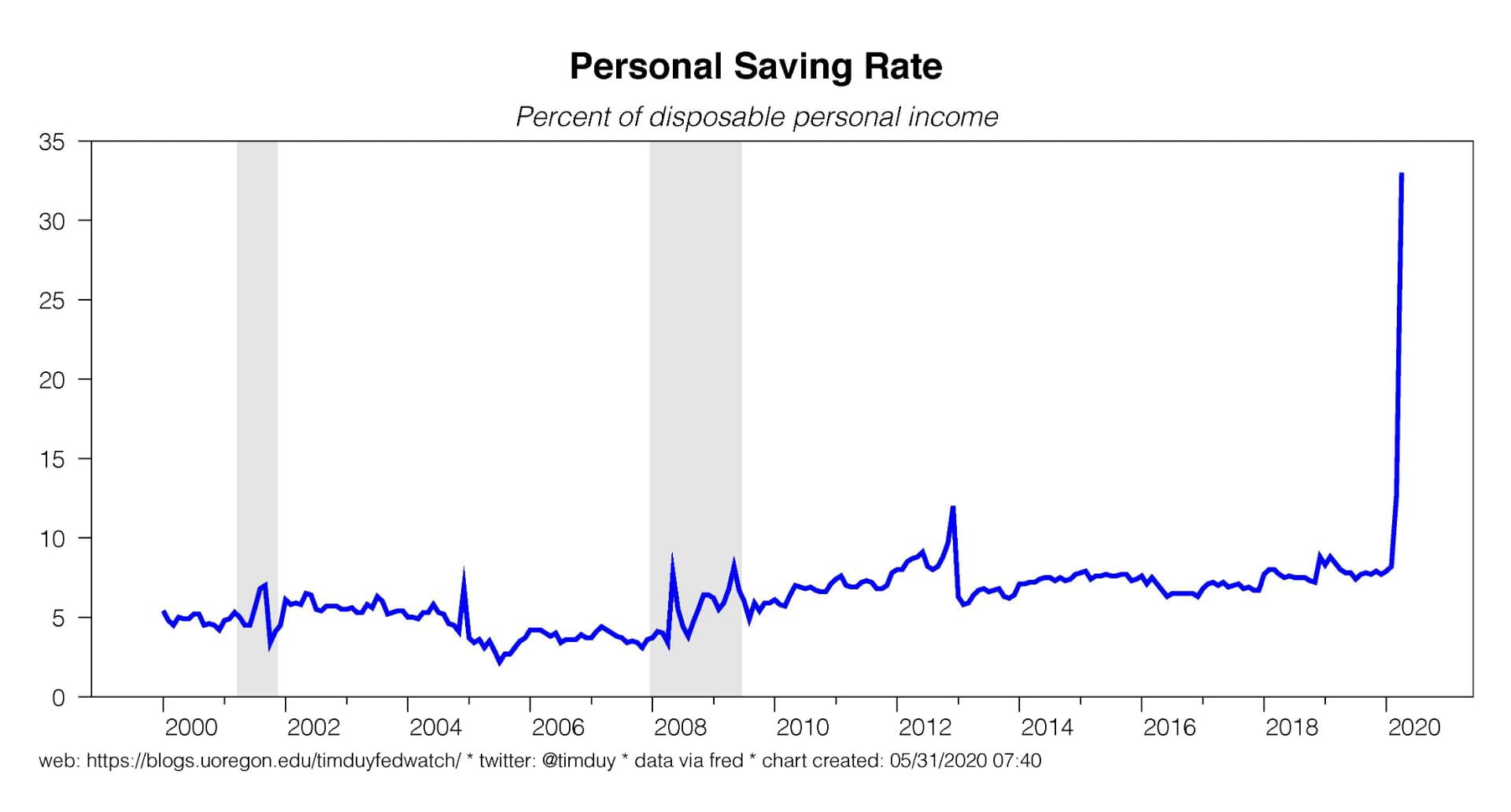

What happens when you drop a slug of money on the economy that can’t be spent? The savings rate surges:

Again, this is at a macro-level; at a micro-level, the unequal and slow distribution of money, particularly as associated with unemployment insurance, has left many struggling to bridge a gap in their finances. That said, many will receive benefits in excess of their incomes. It’s not a perfect plan in any sense, but not the worst especially considering how quickly it was implemented.

As we begin to see a reawakening of the economy, activity will jump higher. Not jump back to February, but it will bounce. Some sectors will some back quickly; I expect health care employment, for instance, to regain jobs quickly as elective procedures return. You can even see the bottoming-out of the economy starting to form in the ISM manufacturing numbers:

Of course, while the initial phase of the recovery may feel a bit thrilling, the recovery will most like lose speed soon thereafter. Too much of the economy will continue to be suppressed to some degree to allow for a fuel recovery. Moreover, firms that went out of business during the shut downs by definition won’t be restarting quickly.

Consequently, the economy will continue to need federal support to transition into whatever the post-Covid economy looks like. It is imperative to keep the money flowing to households during the transition. The Republicans, however, are trying to back away from fiscal support sooner than later and look to be trying to limit the size of the next package to something under $1 trillion. Senate Majority Leader Mitch McConnell is also claiming it will be the last bill. I continue to believe (hope?) that this is more posturing than anything else. I would think the Republicans have enough problems heading into the fall that they wouldn’t want to rip the rug out from under the economy. Something bigger than McConnell’s current position seems likely.

Sadly, even the Democrats are beginning to line up with the deficit hawks as a bipartisan group of House members already looks to curtail the national debt. There is no need for this. It sets up expectations that the government will more likely than not allow only a partial recovery of the economy. There is no reason to have this discussion before the economy has regained its footing. It’s simply counterproductive.

Oddly, I would like this to be the last major federal support package because I would prefer that it be open-ended with provisions that phase out support as the economy improves. What we will likely get instead is package that limps along the economy enough to keep the deficit hawks claiming there is no need for more. Enough to keep the economy growing yet it becomes a fight to get more down the road. It’s the kind of fiscal outlook consistent with a persistent output gap such as that of the CBO’s new estimate. The CBO predicts it will take a decade before output regains levels of the pre-Covid projections.

OK, so let’s just assume that we get another blast of fiscal support. It won’t be a $3 trillion bill, but it will probably be more than a $1 trillion. At the same time, the Fed is keeping the pedal to the metal with low interest rates, asset purchases, lending programs, and increasingly clear guidance that policy rates will be zero for a long time. Overall, a generally supportive set up for financial markets in the near term. Not great, but good.

Problem is that this story feels more vulnerable this week. The rise of unrest across the nation, and the lack of leadership to quell that unrest leaves a big question mark over the outlook. The best-case scenario is that the riots soon revert back to continuous, massive, but peaceful protests. The worse-case scenario is that President Donald Trump acts on his threat to use military force to end the riots.

I would prefer not to think about such possibilities, yet here we are. Aside from the obvious additional damage to the nation’s social fabric, widespread use of military force domestically would I suspect inflame the situation further, worsen consumer activity, and slow the progress of recovery. In addition, it would intensify partisanship in Congress and delay the next fiscal support bill. Moreover, the large crowds and the shutting down of testing facilities also raise the question of a surge in Covid-19 cases in the weeks ahead; if the virus gained another foothold, we would find cities and states forced to retreat on plans to reopen.

Needless to say, widespread military action against U.S. citizens coupled with a resurgence in Covid-19 cases would be … bad. The psychology could turn against equities quickly, just as it did in March.

Bottom Line: On a certain level this shouldn’t be that hard, at least from a macro-policy perspective. Keep pumping money into the economy to support incomes as you build out the public health infrastructure to contain the virus while gradually ramping back up the economy. We just can’t fully commit to that program. That lack of commitment leaves us with a few more downside risks than I would like.