Markets continue to power forward on expectations that the worst is over for the economy. Yesterday the S&P 500 closed just under 3,000, regaining a level last seen at the beginning of March. That show of confidence in the economy works now but two big risks still lurk ahead that could derail the recovery: A resurgence of the Covid-19 pandemic or policy fatigue. Either could put us back where we started.

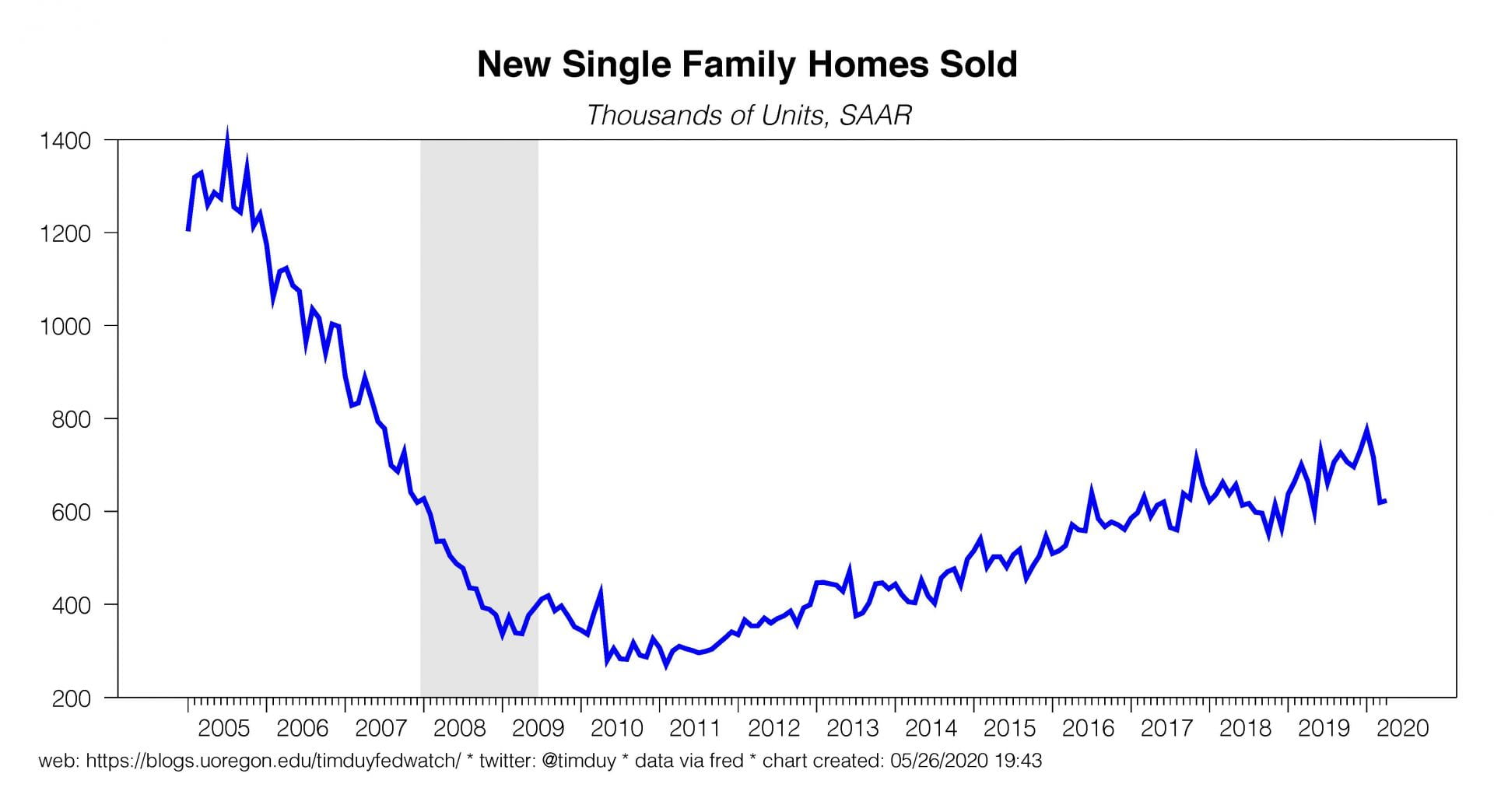

As I have written before, this isn’t your usual recession. We deliberately closed down the economy and the data sank in response. That data will start turning around soon after the lockdowns ease. In fact, the data was turning in the background even with lockdowns still in place. New home sales were up in April to 623,000, gaining 0.6% compared to expectations for a 23.4% decline. Think about the magnitude of that miss; housing doesn’t want to go into the recession many expected for the sector, and the economy typically follows housing. For those still stuck in 2009, it’s worth remembering that housing simply can’t fall as much as it did in the last recession. There’s just not enough room to fall:

Similarly, the Conference Board reported consumer confidence basically held steady in May, down just a notch to 86.6 from 86.9. The expectations component actually rose from 94.3 to 96.9. And why shouldn’t it? In April many parts of the economy hit bottom by definition. Once restaurant activity falls to zero, you have nowhere to go but up.

This isn’t a Great Depression yet but instead a Great Suppression. There was nothing “broken” in the economy in February in the sense of massive imbalances that threatened to be unwound over the course of years. With nothing broken, the economy wants to get back to work and will as soon as we let it. You may not like the level the economy is at when that happens, but market participants will like seeing the light at the end of the tunnel.

Sometimes, however, that light at the end of the tunnel is an oncoming train.

When I look into the second half of the year, I see two major threats that concern me. The first is the possibility of policy fatigue. Market participants might become victims of their own success if the Wall Street rebound delays or weakens the next coronavirus support package from Congress. The Fed isn’t the concern this time. Federal Reserve Chair Jerome Powell and his colleagues learned their lesson in the last recession – don’t signal a policy retreat until the recovery is very well established.

A key reason the economy hasn’t slipped into a depression is that enhanced unemployment benefits keep pumping money into people’s pockets even with the unemployment rate surging to 14.7%. The stimulus checks and payroll protection program are providing a boost as well. The economy won’t have time to heal before those enhanced benefits expire; an extension is needed to smooth the transition into recovery (aid to state and local governments is also critical). We might not – and probably won’t – get the same firms coming back as we had going into the economy, but if households have money to spend, they will support a new, post-virus range of businesses. If they don’t have money to spend, the economy will get locked into a substantially lower equilibrium.

The second threat is that states are rushing into reopening despite lack the necessary public health infrastructure to combat a renewed surge of Covid-19 infections this fall. I worry that most states will create systems that are the bare minimum capable of responding to only the best-case scenarios. We need systems capable of responding to the worst-case scenarios.

For example, China reportedly tested almost seven million people in Wuhan in just 12 days and uncovered 206 asymptomatic cases as authorities responded to the possibility of a second round of infections. Optimally, we should be building systems of similar capacity here in the U.S. Ultimately, it’s the virus that’s the problem, not the economy. Fix the former and the latter will have room to recovery. Ignore the virus at your own peril.

Bottom Line: The first of these two hurdles we have to clear is fiscal support. If Congress comes through with another round of money before the end of July when enhanced unemployment benefits expire, markets will likely find support into the fall. And if the public health infrastructure evolves to the point that we can manage or prevent future outbreaks, we will be well on the road to actual recovery. That’s the optimal scenario and the one market participants are apparently betting on. Of the two risks, I am more worried about another surge in the fall that forces another round of shutdowns. That would delay any market reckoning until sometime after the summer.