Like so many of us, I have found the events of the last several weeks overwhelming and difficult to process. Eight weeks ago I was literally bored with the economy, six weeks ago it was hard if not impossible to process the possibility of deliberately shutting down the economy because of the destruction that would surely follow, and now I am trying to sort through the wreckage of that economy.

The speed and size of the shock was truly from the far, far left-hand side of the distribution. The entirety of a “normal” downturn – the careful analysis of data, the debate over the business cycle implications, the anticipated monetary and fiscal policy responses – that would occur over the span of a year or years occurred in the span of only a few weeks.

No doubt this dramatic turn of events has left it difficult for me to write. I am not inclined to write simply to write. I am not inclined to write simply to attract attention to myself. I am not inclined to pretend I am an epidemiologist. I am not inclined to make bold predictions about how “everything in the future will be different.” And perhaps most importantly, I am not inclined to write when I don’t feel that I can add value.

Adding value when stumbling around in the dark is challenging. Or at least it is hard to for me to see what value is being added. That has, again at least for me, been particularly difficult because any analysis remains predicated on the evolution of the Covid-19 pandemic. And how that evolves is still a mystery. Yet, another challenge is managing your tone, especially if writing in the space between market participants and public policy. The information relevant to one audience might be anathema to the other.

That was a long preamble to highlight my uncertainty about the evolution of the economy over this cycle before I attempt to answer this question: Where are we now? Answering that means we need to move through a difficult conversation. Did the economy already hit bottom? It’s best to leave the room after asking that question. Throw the grenade and walk away.

To begin with, we have to assume something about the path of the pandemic. Although some states are experimenting with reopening now, most states will find such exuberance premature (although it will be an opportunity to learn what works and what doesn’t). As a baseline, it’s reasonable to think that most states edge toward reopening by the end of June.

By the very nature of this recession, it is fairly clear that some sectors have bottomed out. Undeniable, really. We can argue about whether or not zero is really the lower bound for interest rates, but zero is a lower bound for the leisure and hospitality industries. Same for non-emergency medical care. Same for hair stylists. You get the idea. We flipped the switch on large parts of the economy and those parts went dark. Nowhere to go but up.

Hence, we will see a bounce in some portions of the economy as restrictions are eased. Has to happen. It’s the only mathematical possibility. There will be some pent-up demand that will be released. Running through the numbers this way gets you to the forecasts for a Q3 jump in growth after a Q2 collapse.

Past experience tells me that people get very upset when you say things like this. Policy wonks rightly worry that a turning point in the economy will lessen pressure on Congress (I am not so much worried about the Fed right now). And then there is a non-trivial segment of the financial community that are only happy if everything is burning down.

I think somehow the idea of a bottom is often interpreted as announcing an “all’s clear” for the economy. That, however, is certainly not the case. The raw GDP numbers will not tell the whole story. The “bounce” is an artifact of GDP accounting. Behind the scenes will be a huge tug-of-war between opposing forces as the economy grinds out a new equilibrium. The second and third order effects of the initial shock will be passing through the economy even as the first order impact is partially reversed. As an end result, the economy might turn, but it is turning from an extremely low level and the rate of future growth is uncertain.

The lagging nature of the data flow will further complicate our understanding of when the economy reaches a bottom. There are really no leading indicators for this recession. We knew the economy was in recession before the confirming data began trickling in. We know it is already unimaginably bad. We know it will continue to be unimaginably bad even after the economy bottoms just as the incoming data remained strong even as the shutdowns began.

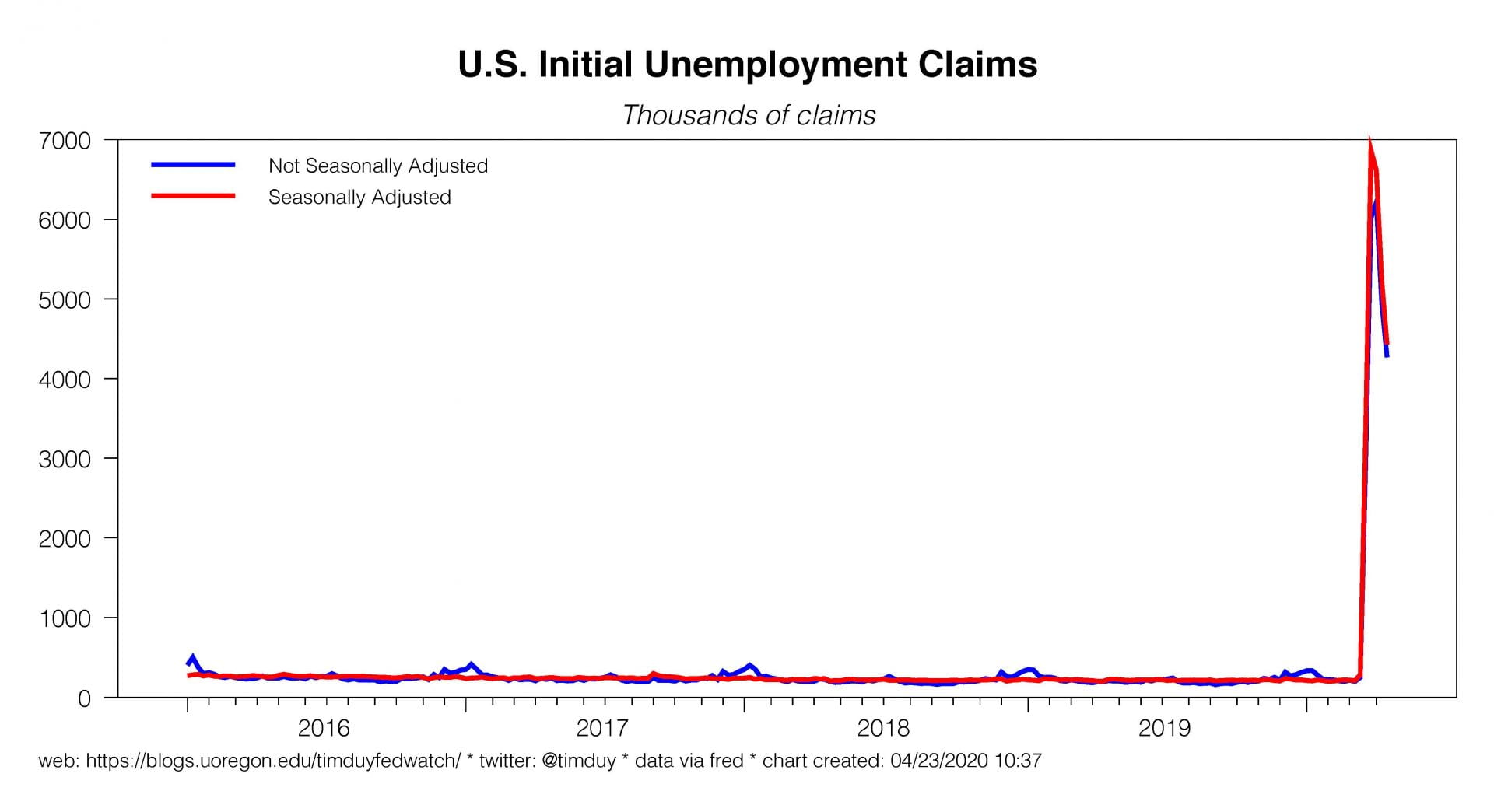

In effect, the compressed nature of the front end of this cycle heightens the traditional “level versus direction” conflicts. The initial claims data reveal this conflict. Claims have declined for three consecutive weeks, from “beyond apocalyptic” to just “apocalyptic.” Claims are terrible but less terrible and being less terrible seems important. Less terrible is a precursor to better.

“Better,” though, for much of the economy remains a long ways off. Reopening the economy will prove much less easy than shutting it down. Broadly speaking, there are three main impediments to a rapid recovery. First, we can’t open up the economy entirely; social-distancing measures will be reduced, not eliminated. Second, consumers will venture out only cautiously (ultimately, we decide when the economy reopens, not the government). Third, we still don’t yet know the full extent of the persistent damage caused by the shutdowns, which firms close, which employer and employee relationships are severed.

The amount of damage to the economy, as well as the magnitude of the second and third order impacts, depend on the effectiveness of federal fiscal support. That has been something of a mixed bag largely due to the timing of moving money out the door. But it’s coming, and it is nontrivial. The PPP loans are making their way into the economy and the pot has been refilled. Continuing unemployment claims rose to just shy of 16 million, but at roughly $1,000/week after the $600 federal boost we get to $16 billion/week or $64 billion per month. That’s real money supporting the economy.

Still, PPP and the enhanced UI will not be sufficient to entirely support the economy (it’s support, not stimulus). We still need expansive aid to states and local governments to cover severe budget shortfalls; such aid will help mitigate the second and third round impacts of the shutdowns. Republicans in Congress are reportedly balking at additional aid with claims that we need to worry about the deficit and complaints about the fiscal irresponsibility of states. Neither claim is relevant at this point. States and local governments should be held blameless just as individuals and firms: The goal is to provide a bridge to the other side of the shutdowns to minimize damage to the economy. I suspect Congress will eventually reach this conclusion, but the possibility that they don’t should be on our list of downside risks.

Most importantly, Congress needs to pivot to viewing this crisis as temporary to a situation that is likely to need to be managed on a long-term basis, both from public health and economic perspectives. We need to be thinking of how to handle the economic fallout for regional outbreaks in the future and creating a public health infrastructure to manage the virus. These are the sorts of actions that will enhance the resiliency of the economy until a treatment or vaccine emerges.

Bottom Line: The economy may bottom in a mathematical, GDP sort of way this quarter, with a subsequent pop in the third quarter. This should not be confused to a “bounceback” or a “V-shaped recovery.” We are past that point. That was an options for a two-week shutdown and rapid reboot. This is a months-long shut down with a slow reboot. The economy will need ongoing fiscal support through that process for it to be successful (monetary policy support too but I take that as a given). And even with that support, the recovery will be slow and choppy (see the challenges of recovery in Wuhan). I suspect what will be most different in the near future is not so much “what” we do but “how” we do it. Efforts will center on trying to resume as much of our past behavior as possible while learning to live with the virus.