The Federal Reserve reaffirmed its commitment to support the U.S. economy through the crisis and during the subsequent recovery. Federal Reserve Chair Jerome Powell and his colleagues will not declare victory prematurely. They have yet to even consider the pull back from the extraordinary level of monetary accommodation they are providing. We are just nowhere near that outcome yet so there is no point in asking about it.

The day began with an unsurprisingly weak reading on the economy. The collapse in March was sufficient to drag first quarter GDP growth down to a recession-level contraction of 4.8%:

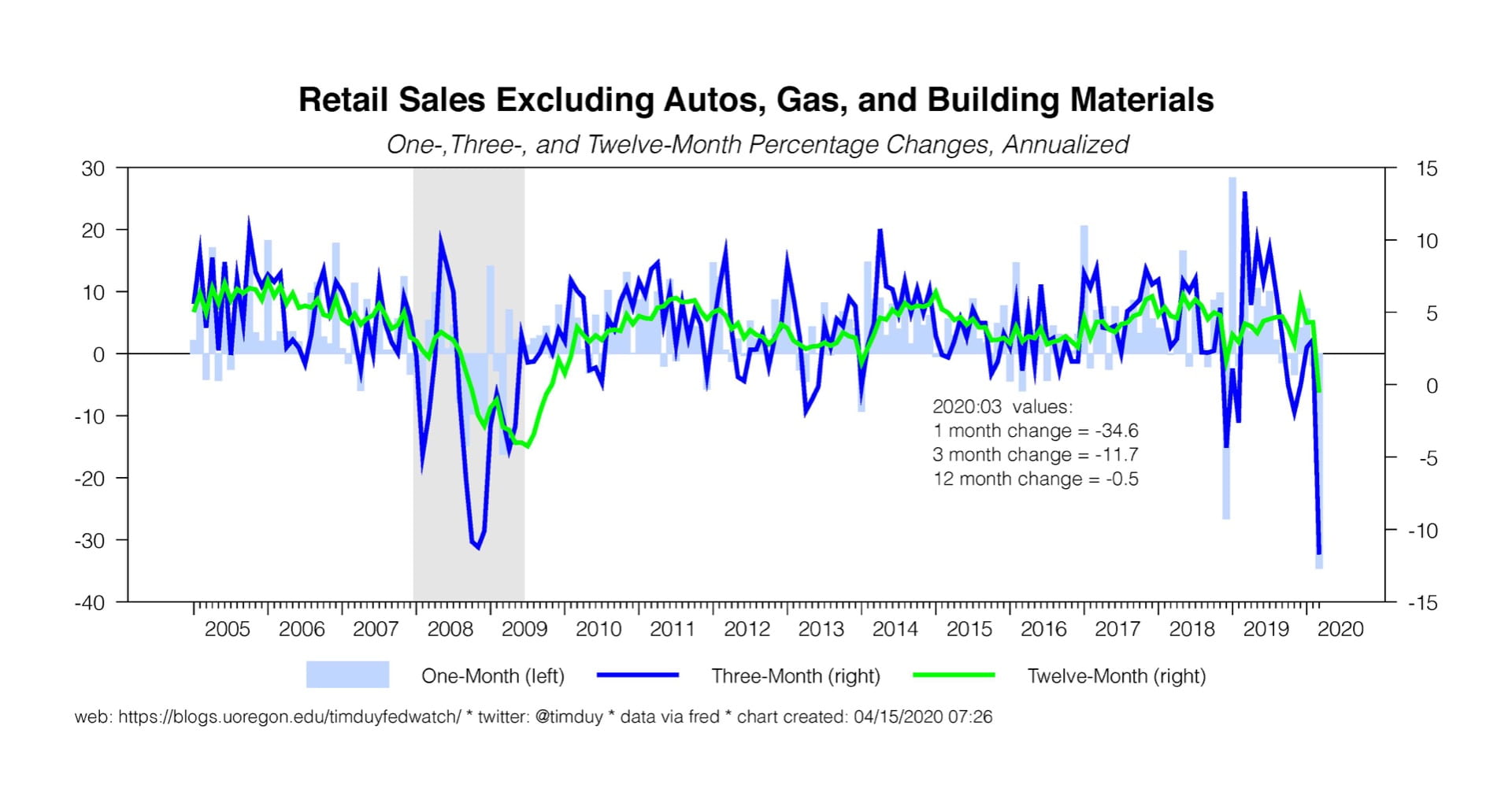

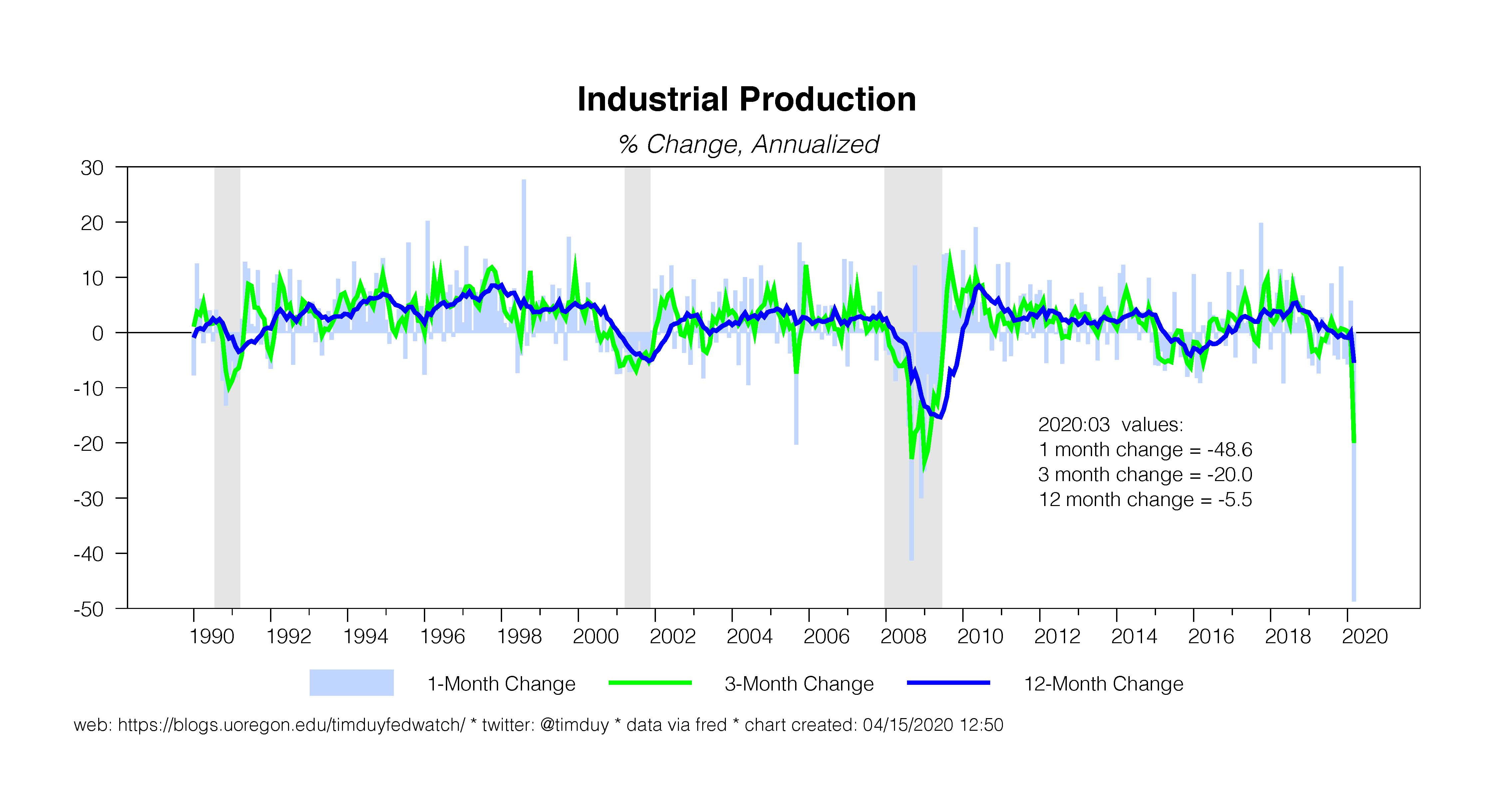

Note that this is an annualized pace, which is something to keep in mind when we see the unimaginably bad numbers for the second quarter. Consumer spending took the biggest hit, subtracting 5.26 percentage points from GDP growth:

Health care, transportation, recreation, and food services and accommodation all took particularly large hits. Health care may seem like a surprise but reflects the cancellation of elective procedures and services. The service side of consumer spending contributed to 4.99 percentage points of the drag on GDP. In recent years, the service-dependent nature of the U.S. economy increased its resilience to the traditional manufacturing shocks associated with recessions. That dependency is a liability this time around as Covid-19 strikes directly on service-type activities.

The Fed has an appropriately bearish view of the situation:

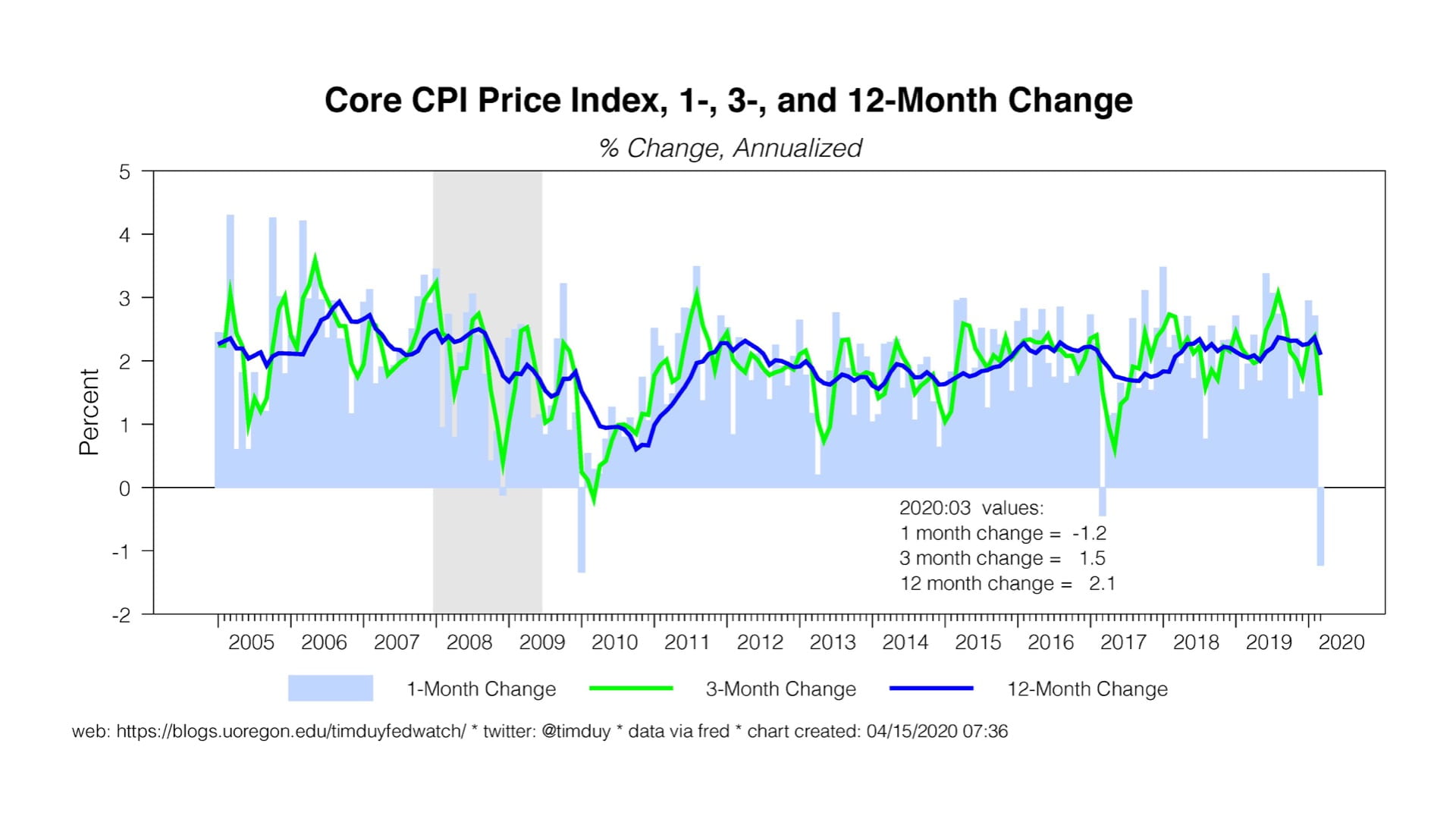

…The virus and the measures taken to protect public health are inducing sharp declines in economic activity and a surge in job losses. Weaker demand and significantly lower oil prices are holding down consumer price inflation. The disruptions to economic activity here and abroad have significantly affected financial conditions and have impaired the flow of credit to U.S. households and businesses.

The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term…

I think the important element of this outlook is the risks “over the medium term.” Powell explained those risks as related to the virus and possible future outbreaks, the damage to the supply side of the economy (loss of job skills, closure of firms), and the global drag. Powell is looking forward to a “square-root” shaped economy with a bounce later this year as restrictions ease but with a high-likelihood of slow growth thereafter.

Importantly, Powell emphasized that the Fed would not retreat from its current policy stance until he and his colleagues were confident that the recovery would be sufficient to meet their goals. In other words, they aren’t yet thinking about when to pull back from the lending programs, when to scale back the balance sheet, or when to raise interest rates. Powell is intent not to make the mistakes of the Bernanke Fed, which began talking about reversing QE almost as soon as it began (to be fair, the politics and experience were not in the Fed’s favor at the time). Stop asking about it. I am going to lose it the next time I hear a financial journalist asking Powell when the Fed is going to raise interest rates.

Powell also emphasized the need for ongoing fiscal policy to support the economy and while he retains concerns about the sustainability of the debt over the long-run, such concerns were irrelevant now. It was a clear message to Congress and the President: Don’t drag your feet on more economic support. In music to my ears, Powell added that the economy was fine before the virus and the downturn wasn’t anybody’s fault. In other words, he has some thoughts about your moral hazard concerns.

It is worth considering that this whole situation would likely have gone sideways six times over if Trump had gotten his apparent wish and ousted Powell in late 2018. And, I suspect, gone sideways ten times over with a Judy Sheldon as Chair.

Bottom Line: The Fed has pulled out all the stops to support the economy and will continue to use every tool at their disposal to minimize the tail risks to the outlook and support the recovery. Powell and his colleagues have not declared victory; they anticipate a long road ahead. Here’s the thing: Powell gets it. He understands the enormity of the situation. He isn’t going to stand by and let it all fall apart without a fight. And he isn’t going to walk away after the first round.