Matthew Boesler at Bloomberg brings us this:

Policy makers have acknowledged getting labor markets wrong in the recent past, and say they’ve learned from community outreach this year that many Americans haven’t felt the benefits of the economy’s long expansion.

All this rethinking has bolstered the case for keeping rates low at times when prices aren’t rising much — like the past quarter-century or so. And if the new ideas take hold, America’s next economic upswing may be overseen by a Fed that’s less inclined to raise rates in response.

This is an important development that has gained substantial traction this year. Indeed, it is likely already having a policy impact; I believe it was one reason for the Fed’s dramatic pivot this year. The Fed recognized the benefits of sustained low unemployment and were unwilling to risk losing those benefits to fight phantom inflation when the risks to the outlook were rising. Hence they lowered both interest rates and the expected path of rates. In comparison, in December of last year central bankers were still eyeing rate hikes for 2019 and beyond.

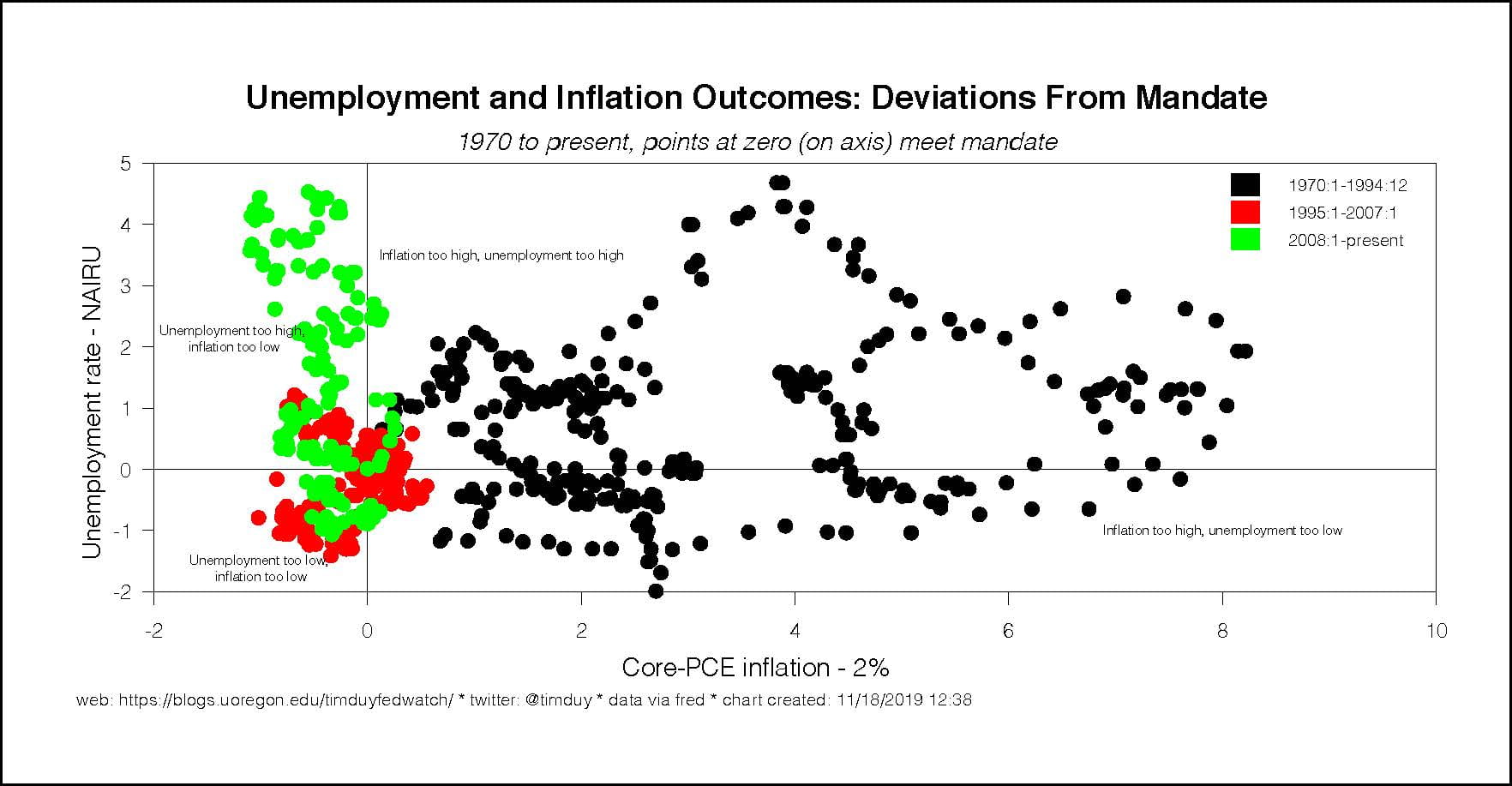

I have long argued that the Fed has a tendency to favor high unemployment over high inflation. Consequently, in the post-1995 period in particular the economic outcomes have been subpar, with unemployment unacceptably high during much of that period:

Realistically, since 1995 inflation has never been sufficiently high to cause concern. Moreover, the lower left-hand quadrant arguably doesn’t make any sense; if inflation is too low and unemployment too low, then more likely than not the estimated natural rate of unemployment is simply too high.

Persistently excessive unemployment has its costs. Not only does the period of low unemployment not extend long enough to spread its benefits to the most challenged sections of the labor market, but it also tips the scales toward employers when it comes to wage bargaining. Workers who are always fearful of losing their jobs have little incentive to derive a hard bargain for higher wages.

Boesler credits Minneapolis Fed President Neel Kashkari with leading the charge on this issue, arguing that the Fed policy does have a role in distribution outcomes. And he is not wrong; indeed, Kashkari tendency toward dovishness has proven more correct than not since he came on board. His concerns about inequality helped prompt him to launch the Minneapolis Fed’s Opportunity and Inclusive Growth Institute and has now found its new leader in the highly-respected economist Abigail Wozniak.

The implication for policy of a broad acceptance of idea that the Fed may have contributed to inequality in the past is that the Fed is likely to be much more cautious when raising rates and respond to economic weakness much more quickly. In other words, this adds another reason to expect rates will remain lower than what we might have thought the Fed’s reaction function would suggest.

There will be two immediate criticisms of such a more dovish direction. The first is that lower interest rates contribute to inequality by boosting asset prices. This I think is just a silly complaint. The ultimate inequality comes from not having a job or having a job with no bargaining position. The Fed should focus first on the employment situation and I don’t see the problem in the related positive impact on asset prices. Wouldn’t we expect higher asset prices if another percentage point or two of the labor force was consistently employed rather than being without a job and income or that the risk of recession was lower?

The second complaint is that lower rates will contribute to asset bubbles and financial instability. This I think is an overwrought concern. I think investor psychology has a greater role than interest rates in creating and sustaining asset bubbles and trying to pop a bubble likely requires recession-inducing levels of interest rates. In addition, note that literally decades of low interest rates has yet to recreate the property and equity asset bubbles that Japan experienced in the 1980’s. If it were so easy, Japan would have made it happen by now.

Bottom Line: The Fed edges more dovish with each year that passes without the inflation outbreak so-long feared. It’s another reason to expect that both interest rates will tend to surprise on the low side and, if the Fed increasing errs against recession, expect that equities will surprise on the high side.