If You Don’t Have Any Time This Morning

The Fed is leaning toward a rate cut next week. I suspect that they will need to be a little more direct about the conditions that will drive future policy moves; a statement like the last will fuel the perception that another rate cut is in the works for December.

Technical Updates

I have been a bit radio silent this past month, still working through some technical issues with my subscription service. I will be moving some subscribers over to MailChimp soon. Sorry for any inconvenience this down time may have caused.

Key Data

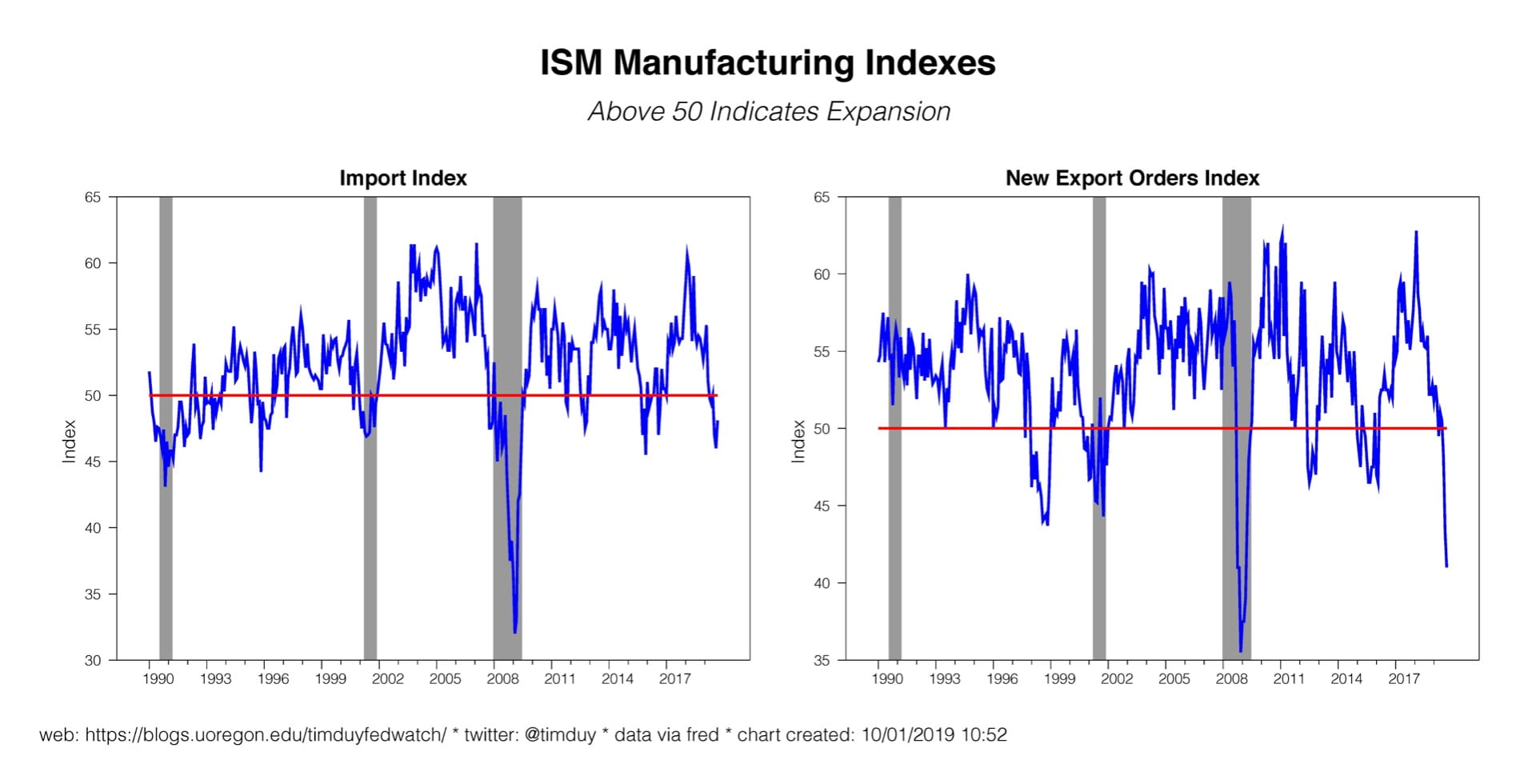

The data flow remains fairly lukewarm, neither demanding another rate cut nor requiring the Fed to hold rates steady. Manufacturing remains the weakest link in the chain. Industrial production dipped 0.4% in September but the GM strike was an extra drag on the data. Excluding autos, industrial production was down just 0.2%. Note that after declining in both the first and second quarters, industrial production posted an annual rate of 1.2% growth in the third quarter. This could signal that the downtrend in manufacturing is bottoming out. Watch the PMI’sgoing forward for signs the numbers are stabilizing around the 50 mark. Some evident stabilization in manufacturing would pull the Fed away from a cut in December (assuming an October hike).

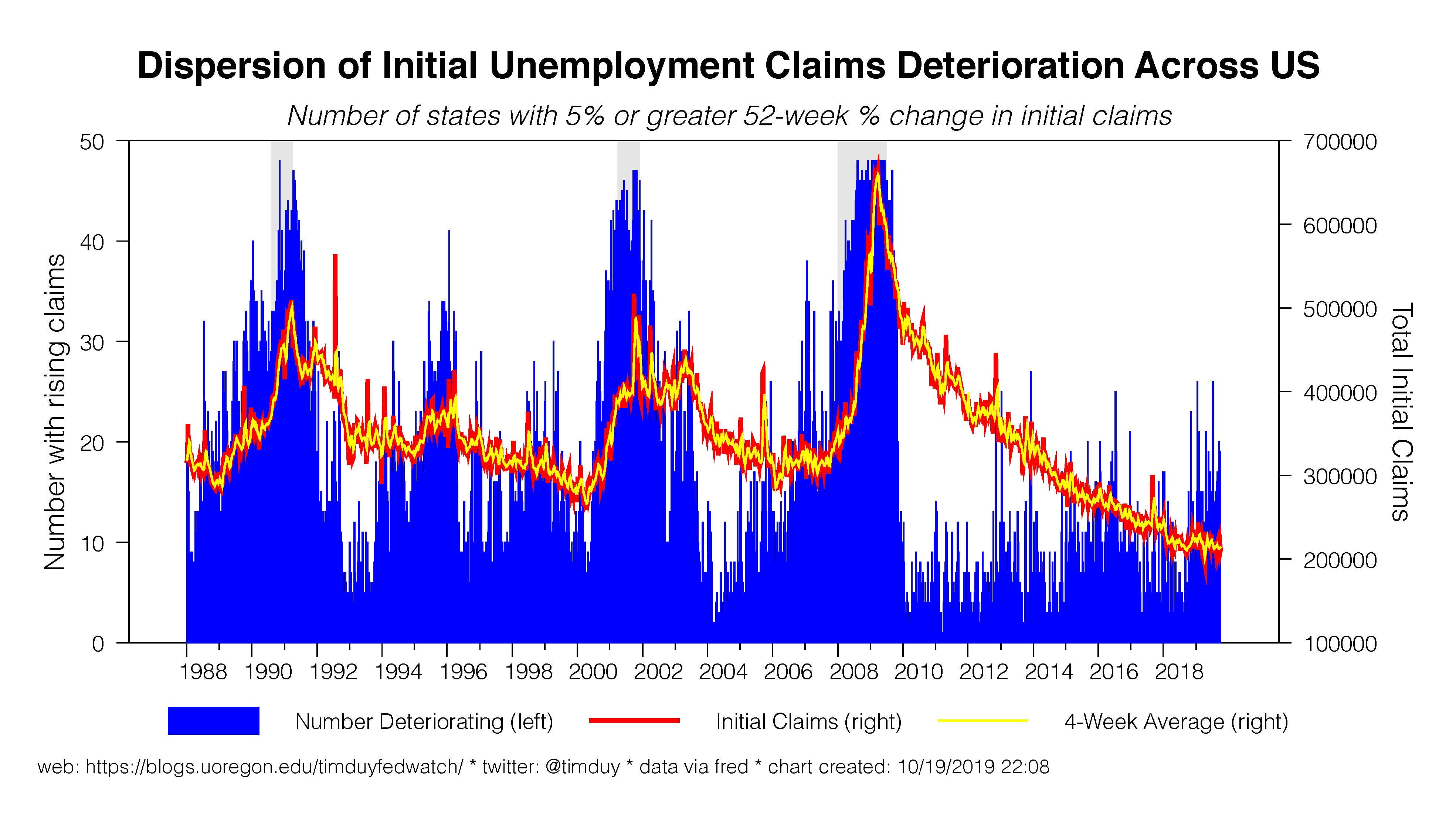

Retail sales came in on the soft side.I am wary about reading anything too negative into the numbers; the volatility over the last year has been unusual, with excessive weakness at the end of 2018, an offsetting jump early in 2019, and a string of unusually consistent solid readings over much of this year. Washing it all out puts the year-over-year pace at a respectable 4.9%, closer to the highs than the lows of this cycle.Note that the Michigan consumer sentiment measure (preliminary) rebounded in October, suggesting that household spending continues to hold up more broadly. I don’t think interesting things are going to happen in consumer spending as long as the labor market remains solid. And while job growth looks to have slowed since last year, initial jobless claims continue to hold at fairly low levels. The dispersion of worsening claims is a bit wider but not so much that they would signal firms will soon engage in widespread layoffs.

I don’t think interesting things are going to happen in consumer spending as long as the labor market remains solid. And while job growth looks to have slowed since last year, initial jobless claims continue to hold at fairly low levels. The dispersion of worsening claims is a bit wider but not so much that they would signal firms will soon engage in widespread layoffs.

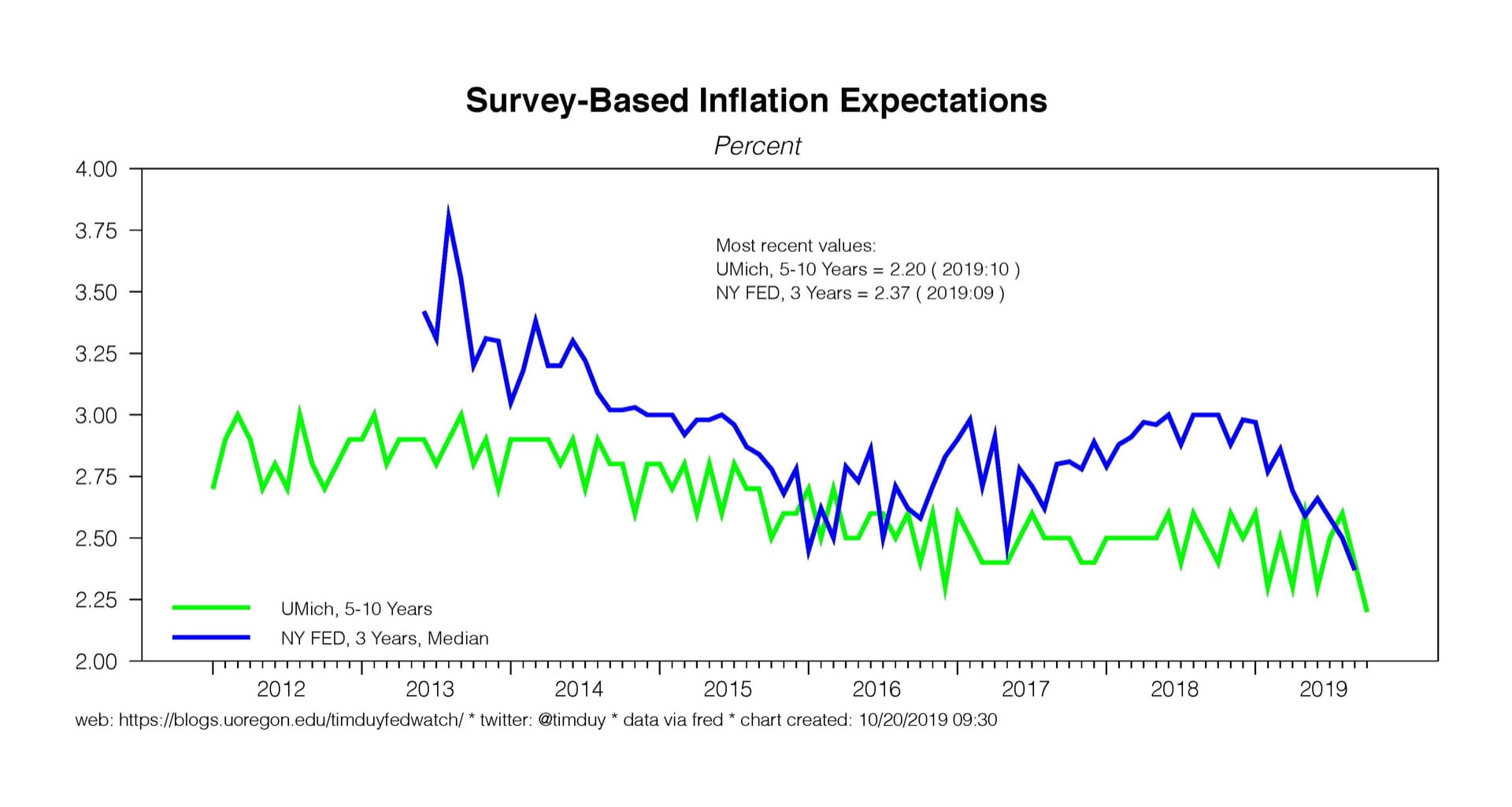

Housing starts declined in September although previous months were revised upwards. The volatile multi-family component accounted for the decline; single-family units have for all intents and purposes rebounded from last year’s swoon. Monetary policy worked as expected in housing, with lower rates stimulating a market that began to look shaky. Also note the builder confidence rebounded in line with housing. Inflation expectations are looking weak with a noticeable downtrend in the New York Fed measure and a record low for long-term expectations of 2.2% in the Michigan estimate. Needless to say, this is not the data the Fed is looking for. The Fed very much needs to keep the economy out of recession if they hope to reverse these trends and stabilize inflation near their 2% target.

Inflation expectations are looking weak with a noticeable downtrend in the New York Fed measure and a record low for long-term expectations of 2.2% in the Michigan estimate. Needless to say, this is not the data the Fed is looking for. The Fed very much needs to keep the economy out of recession if they hope to reverse these trends and stabilize inflation near their 2% target.

Fedspeak

We continue to see mixed opinions on the need for another rate cut in October.There is a contingent that includes Boston Federal Reserve President Eric Rosengren and Kansas City Federal Reserve President Esther George that oppose another cut; both will likely dissent again if the Fed cuts as expected. There is another contingent that is leaning in the direction of holding steady but could likely be convinced to accept another cut. For instance, Dallas Federal Reserve President Robert Kaplan falls in that category. From Nick Timiraos at the Wall Street Journal:

Mr. Kaplan told reporters Friday he had strongly supported the prior two rate cuts well before each meeting but that he was now agnostic about whether the Fed should proceed with a third rate cut in October. “We have a December meeting also,” he said.

“One argument to me is to take a little bit more time, reserve the right to take additional action if conditions merit it,” he said. “It may be wise to take a little time to assess and continue to turn over a few more cards. That’s what I’m weighing.”

The argument here is that the economy is not obviously desperate for a rate cut and therefore the Fed has time to assess whether another cut is actually necessary. Even if you anticipate the need for another rate cut this year, they still have December left to make that move.

Minneapolis Federal Reserve President Neel Kashkari supports another rate cut, but has backed away from calls for a 50bp cut. Via Mike Derby at the Wall Street Journal:

Mr. Kashkari explained that he isn’t pressing for a half percentage point cut now because conditions have changed. When he made that argument, doing a big rate cut then would offered a salutary jolt to the economy. “We’ve somewhat lost the shock opportunity,” he said.

I disagree with Kashkari on this point; moving 50bp when completely unsuspected would have some serious shock value next week. Still, it isn’t going to happen.

There is a large contingent on the Fed, particular the Governors themselves, that have not tipped their hands as to their expectation for this next meeting. Vice Chair Richard Clarida, for example, spoke last week on the economyand repeated the Fed’s mantra that the economy is “in a good place.” Still, I think this is notable:

But despite this favorable baseline outlook, the U.S. economy confronts some evident risks in this the 11th year of economic expansion. Business fixed investment has slowed notably since last year, exports are contracting on a year-over-year basis, and indicators of manufacturing activity are weakening. Global growth estimates continue to be marked down, and global disinflationary pressures cloud the outlook for U.S. inflation.

Clarida says that global growth estimates “continue” to be marked down. I think he would be more comfortable holding rates steady if growth estimates were instead steady. Later, when explaining why the Fed cut rates, Clarida says:

The Committee took these actions to provide a somewhat more accommodative policy in response to muted inflation pressures and the risks to the outlook I mentioned earlier.

Policy is only “somewhat more accommodative.” That suggests that there is room to go before policy becomes sufficiently accommodative to offset the downside risks to the outlook.

Thinking about the current low inflation environment, Chicago Federal Reserve President Charles Evans said:

This leads me to think that the Fed should continue to cautiously probe for the true level of maximum employment. That is, we shouldn’t treat a statistical estimate of the natural rate as a hard barrier that automatically signals an impending problem. Of course, we should also be mindful of the possibility that unwelcome inflationary imbalances could yet emerge. We need to keep both possibilities in mind.

This is something to keep in mind. Even if Evans isn’t jumping on the bandwagon for another rate cut, he doesn’t sound like he is looking for a rapid reversal of the recent cuts absent some evidence that inflation pressures are building. I think that the Fed will be more cautious in the future regarding rate hikes than they were in 2017 and 2018.

Upcoming Data

Fairly light week ahead. Backout period, so no Fed speakers. Existing homes sales on Tuesday and new home sales on Thursday will provide fresh looks on the health of the housing market; I don’t expect there will be any substantial changes in that part of the economy for the time being. Thursday we also see the usual initial unemployment claims report and the final release of Michigan consumer sentiment will come on Friday. Perhaps most important will be the readings on manufacturing. We get Richmond and Kansas City surveys on Tuesday and Thursday, respectively, and new durable goods orders on Thursday. So far, new core durable goods orders have held up well in this cycle, suggesting manufacturing weakness is actually fairly limited relative to the 2015-16 downturn in that sector.

Discussion

Despite generally lukewarm or outright hostility to the idea of another rate cut in the public musings of Fed officials, market participants anticipate with virtual certainty that the Fed will cut rates next week. There is good reason for this certainty: Senior leadership at the Fed has not actively pushed back on market expectations of a rate cut.

I don’t think this means the Fed is being bullied into another rate hike. I think more likely is that the core voting members of the FOMC are leaning toward a rate cut and hence see no reason to push back on market expectations. Why lean toward a rate cut? I see a number of reasons:

- Falling inflation expectations.The Fed has been fairly clear that they would view falling inflation expectations as an impediment to reaching their inflation target. Better then to err on the side of more dovish policy to help firm those expectations.

- Strong dollar.The strong dollar feeds back into the US as lower inflation. The Fed should want to push back against this trend with easier policy.

- Deteriorating global outlook.As Clarida noted, the global growth forecasts continue to fall. The Fed will fear that continued weak global activity will negatively impact the U.S. economy, particularly manufacturing.

- Balance of risks.Although there is arguably some light at the end of the tunnel in the trade disputes with China, the Trump administration has proved too many times in the past that tariffs remain a weapon to be deployed indiscriminately. The Fed cannot take any respite in the trade wars as anything but temporary.

In addition, I think the Fed will want to sustain the momentum provided by past rate cuts. Chair Jerome Powell has repeatedly stated that the Fed’s pivot to a dovish stance has been instrumental in holding up U.S. growth this year. This has been particularly evident in the housing sector. The Fed does not want to give up those gains, and hence should be wary of blindsiding markets by not cutting rates. Such an action would risk another major reassessment of the path of Fed policy, this time in a hawkish direction. That would not serve the Fed any purpose at this point.

Consider also the Fed’s signaling in recent months: Inflation currently is not a barrier to easier policy, falling inflation expectations would pose a challenge to meeting the Fed’s goals, low unemployment provides many benefits that would want to protect by holding unemployment low, and the risks to the downside still dominate the outlook. Unless the data is demanding otherwise, which it is not, the course of action that is most consistent with this signaling is another rate cut that errs on the side of caution.

The core of the Fed will want to get financial conditions sufficiently low that they are confident the economy can overcome the current basket of risks. That argues for another cut next week. Still, the cuts won’t go on forever absent a recession. I think they will have to eventually signal confidence in the stance of policy relative to the risks such that further rate cuts are not necessary without a clear deterioration in the outlook. I see that as a possibility for next week’s statement. In other words, we should be wary of a “hawkish cut.”

Bottom Line: The Fed is on track for another rate cut next week; the core of the FOMC has not been willing to push back on market expectations for a cut, so we can reasonably believe that market participants are correction understanding the Fed’s reaction function. At some point soon the Fed will start signaling that they need more justification in the data to keep cutting.