Fed policymakers from around the nation once again descend upon Washington D.C. to ponder the path of monetary policy as the economy eases down from the fiscal-stimulus boosted pace of 2018 to something more consistent with what the Fed believes to be sustainable growth. The expectation is that the Fed will leave policy rates unchanged and will reiterate their intention to remain “patient” while awaiting the data that will guide their next move. Still, there will be plenty of excitement even if rates hold steady. More important will be the new set of forecasts, which will likely shift to reflect the “patient” stance adopted at the January FOMC meeting. In addition, I anticipate the Fed will announce a plan to wind down the balance sheet runoff.

Incoming data generally continues to support the Fed’s plans to hold rates steady. In my eyes, there are clear signs the economy continued to slow in the first quarter but the pace of the deceleration remains inconsistent with recession. New orders for core-durable goods, for example, edged higher:

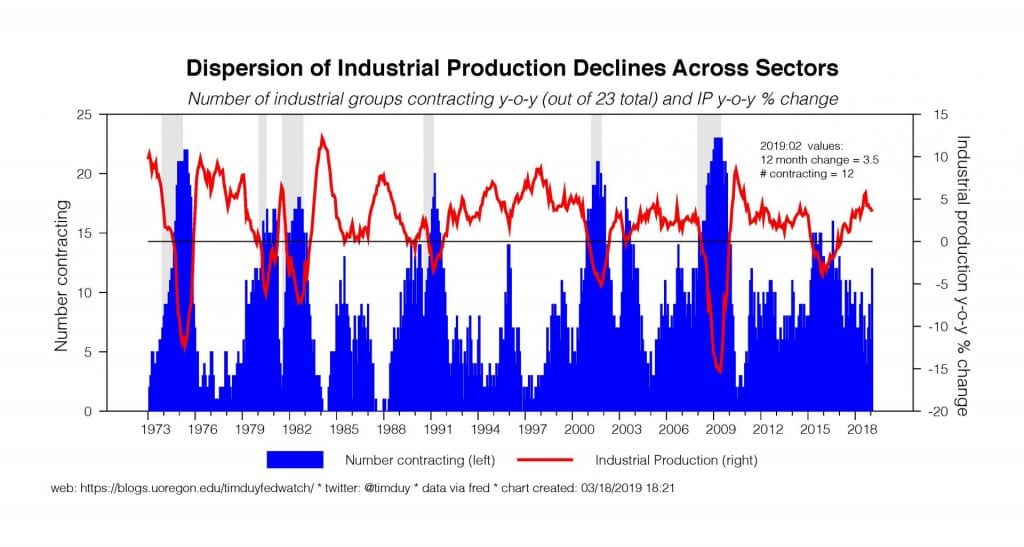

The gains did little to reverse the recent declines, but given the experience of the past two recessions, we would have expected a much sharper decline if the economy was decelerating rapidly. The same can be said for industrial production, which slid during in January and gained only a touch in February. The pace over the past year has decelerated:

In addition, the number of sectors contracting rose higher as would be expected in a slowing economy. Remember though that during a recession, typically the declines in industrial production are deeper and the dispersion across sectors is greater. We also should not ignore the lesson of 2015-16, during which a manufacturing shock remained fairly well contained. In short, the numbers again suggests softening, not recession.

Core retail sales rebounded from the dreary December number (again, as expected in a still growing economy):

My expectation at this point is that when the recent volatility passes, retail sales stabilize closer to the 2015-16 pace than the 2017-18 pace.

Initial unemployment claims edged down last week:

Here again, the modest rise in claims and widening of deterioration across states is consistent with a slowing economy, but the overall pace of worsening still remains short of recessionary.

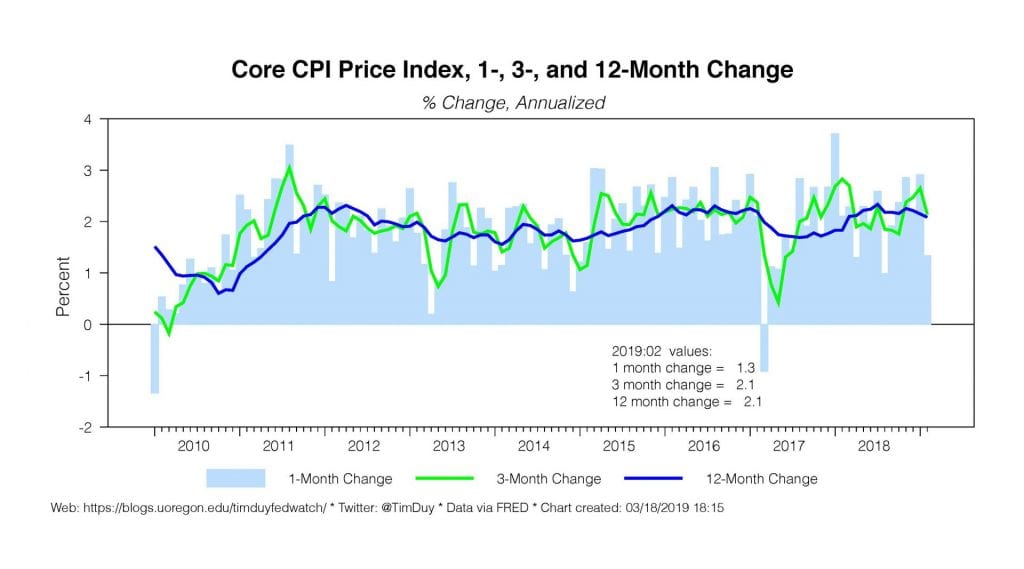

Soft inflation numbers certainly caught the Fed’s attention:

I suspect the above data will support a downgrade in the median growth forecast for 2019 to something closer to 2%, close to the median longer run forecast of 1.9%. That would mean the economy would fall to its sustainable growth rate about a year ahead of what the Fed expected in December.

With growth downshifting, inflation soft, and rising concerns about deteriorating inflation expectations, the Fed has the opportunity to sharply pull down the expected path of rate hike and wipe out the two 2019 rate hikes expected at the December meeting. This would be consistent with recent communications and I suspect that the Fed would not want to whipsaw markets with a set of projections that was markedly different from what the mantra of “patience” they have been chanting all up and down Wall Street and Main Street.

A shift downward in the dots is the expectation; the risk is that the gap between longer run unemployment and forecasted unemployment remains wide enough to keep a sufficiently large subset of FOMC participants thinking that they still need to snug rates higher that the median dot calls for another hike this year. More interesting to me, however, is the possibility that at least one dot anticipates a rate cut in 2019. I would not be surprised if one FOMC participant thought a slowing economy with already soft inflation numbers would more likely that not justify a rate cut by the end of the year.

Bottom Line: I expect the Fed will revise their projections to reflect the dramatically more dovish tone taken since the ill-fated December rate hike. Such a move also appears consistent with incoming data. Moreover, Fed speakers have given little reason to believe that market participants have taken an overly dovish view of policy. Altogether, that means the dots will reveal a marked downshift in the expected path of rate hikes. If we don’t see that, we will be pondering the cause of yet another communications divide between central bankers and market participants.