Click here for newsletter version!

First, an excerpt from my latest on Bloomberg Opinion:

The Federal Reserve this month is widely expected to raise interest rates for the eighth time in the current hiking cycle that began in December 2015. Get ready for tensions within the Fed to spill over into the public as monetary policy moves closer to estimates of the neutral rate.

The Fed staff will likely push harder for policy makers to follow a model-based approach with fairly hawkish implications that would result in rates rising beyond what is considered a neutral level. Although Fed Chairman Jerome Powell doesn’t look married to the Fed’s models, he hasn’t provided a great deal of alternative guidance. That means policy will become less predictable in 2019.

Second, that said, policy is pretty predictable for the rest of this year. The Fed will hike rates in September, they will most likely hike rates in December, and at the December meeting they will likely signal they are not yet ready to pause. The continued strength of the US economy provides the simple reason the Fed will push forward with rate hikes in the near term. Indeed, the August labor report provides more evidence that the economy continues to charge forward despite the uncertainties induced by the Trump Administration.

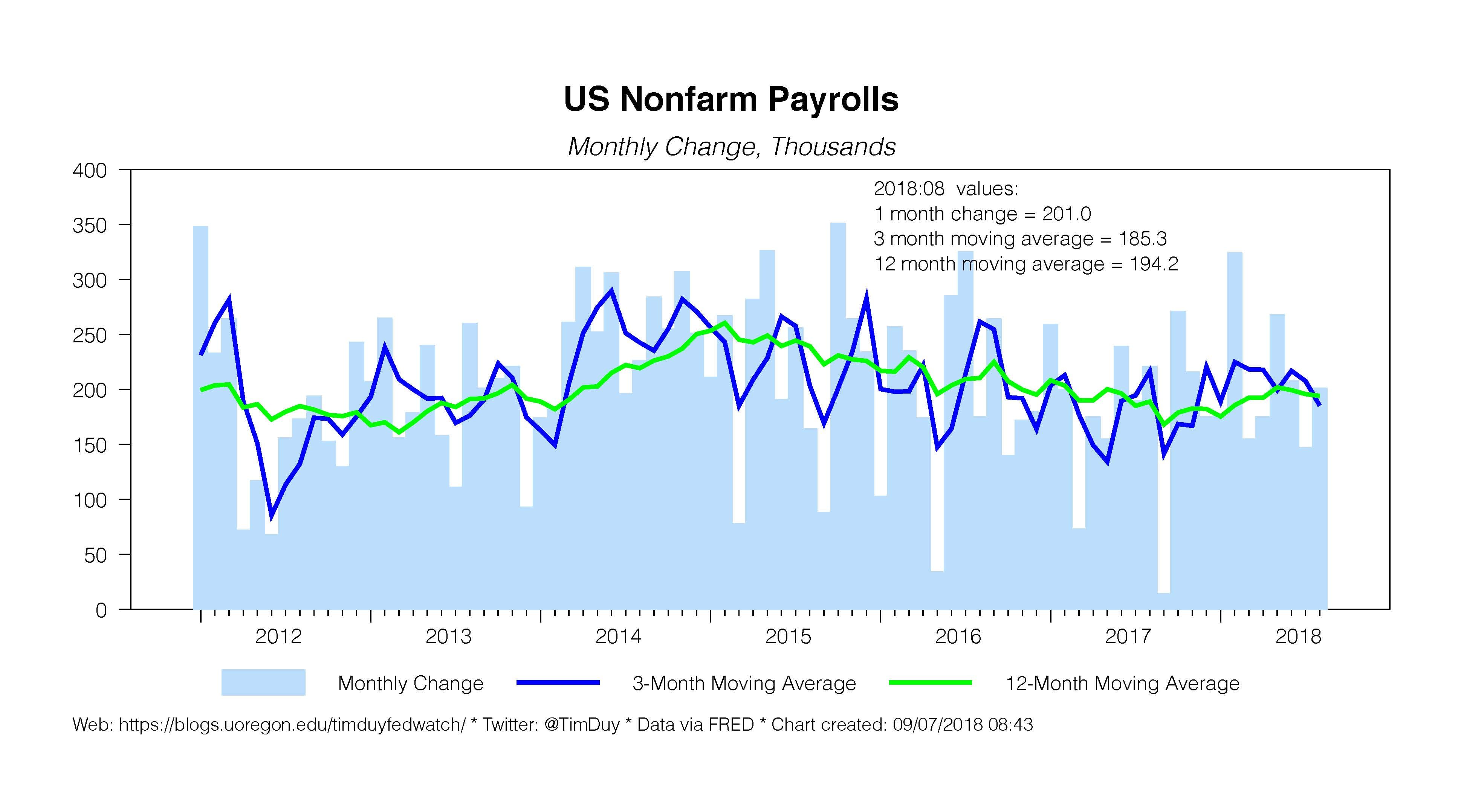

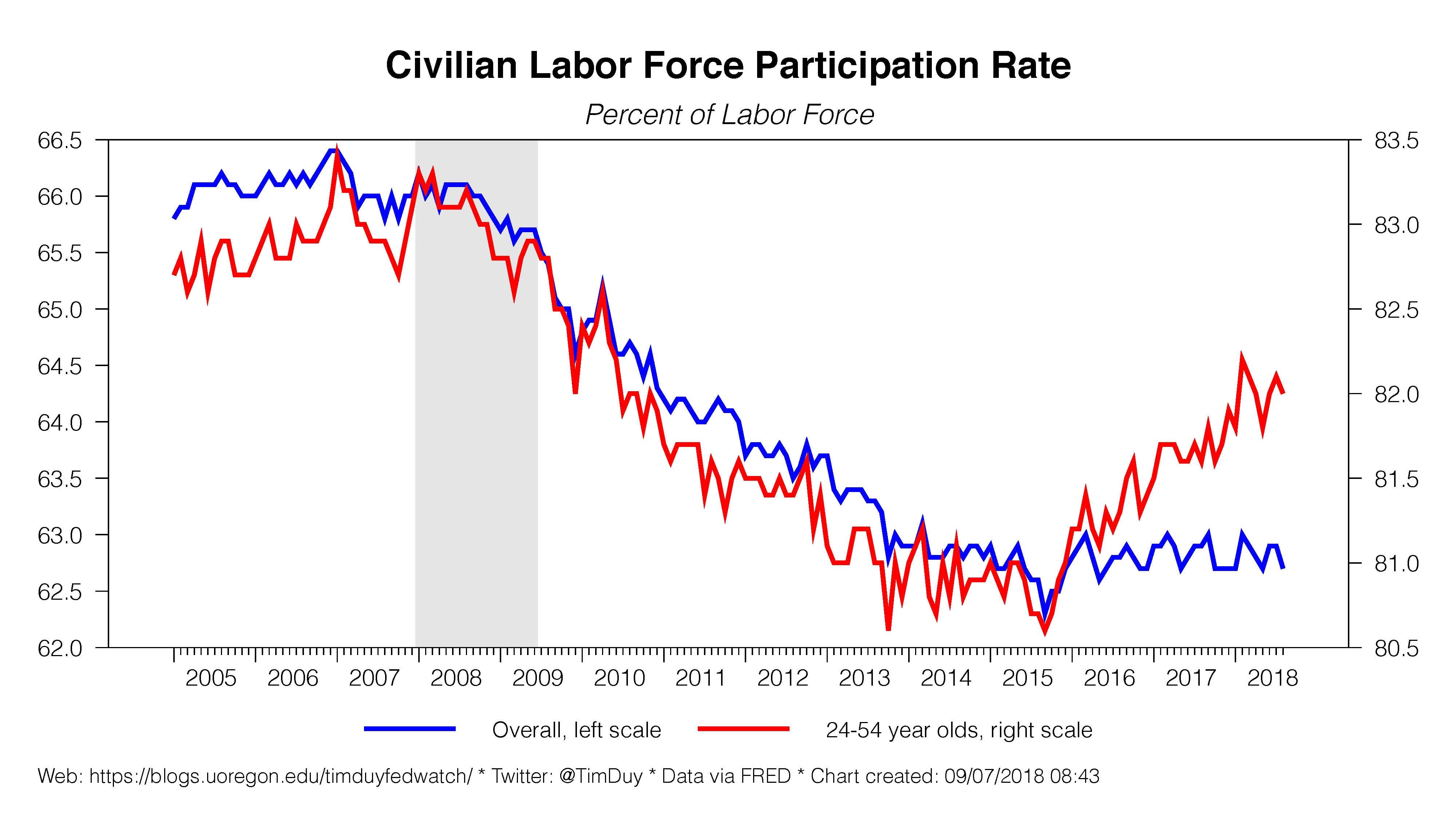

Firms added 201k employees to their payrolls in August, pretty much the same pace as the last three months and the last twelve months. The unemployment rate held steady at 3.9%; the number of unemployed fell but the number of persons in the labor force did as well. The labor force participation rate continues to hover in a familiar range. The Fed will see this as reason to believe that the pace of job growth remains sufficient to push the unemployment rate still lower, keeping fears of overheating alive.

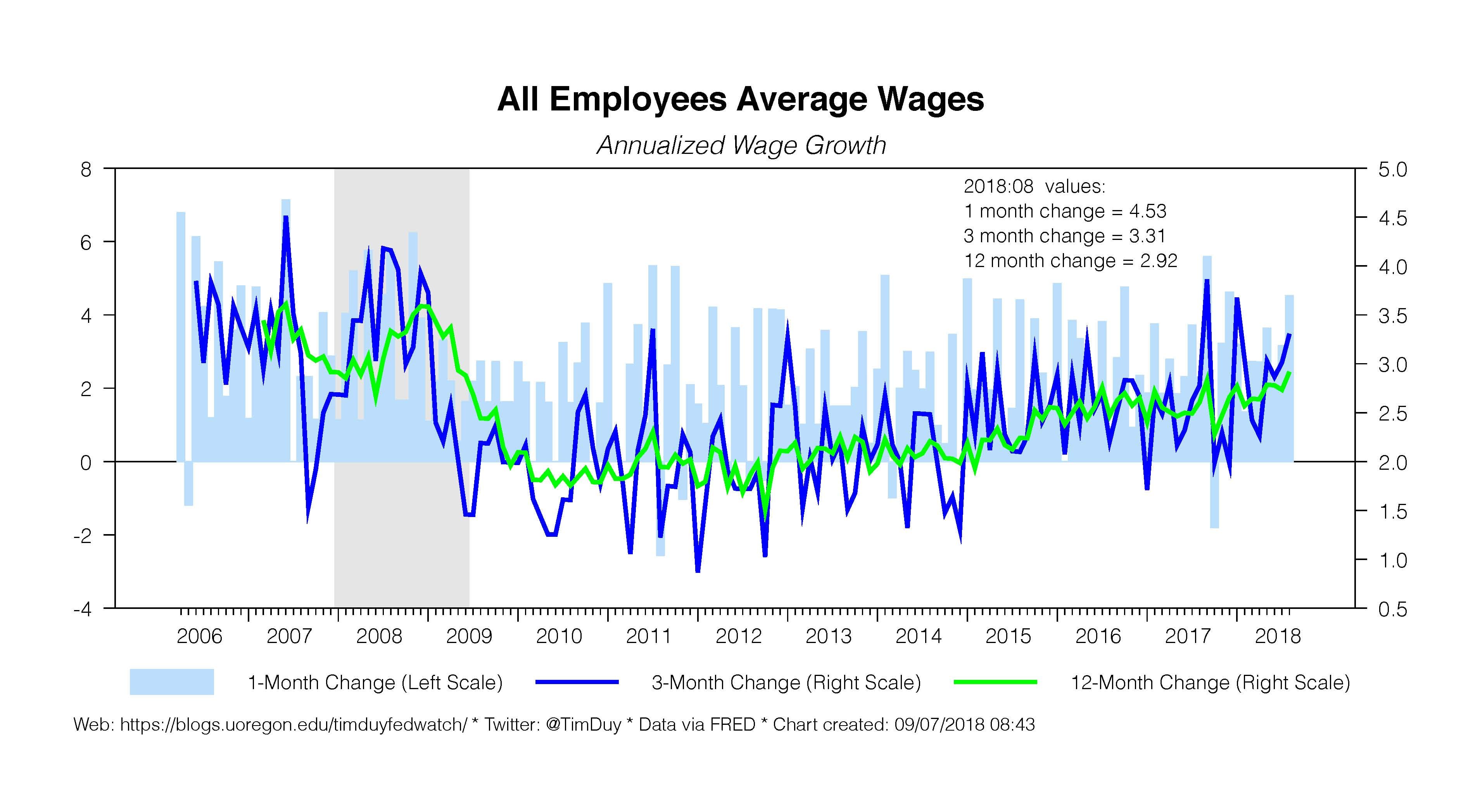

Attention fell heavily on the wage number as average wages rose to a cycle high of 2.9% year-over-year. This extends the trend of slow but steady increases in wage growth and will provide the Fed reason to believe that the economy is working as it should.

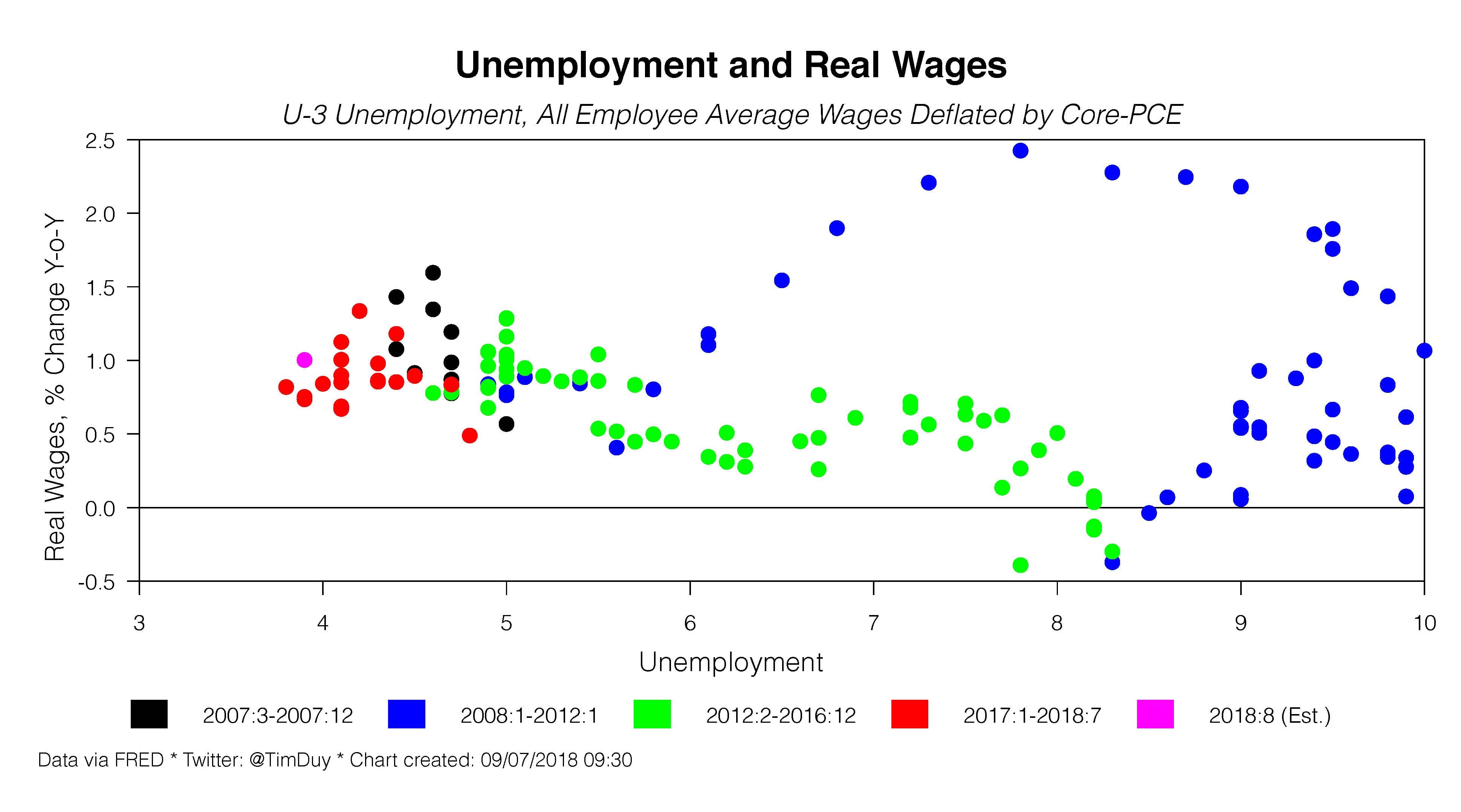

Note that the wage gains shouldn’t really be a surprise – wages had to rise to keep pace with inflation. Using core-PCE as a deflator (which I think it more appropriate than headline because it likely more accurately reflects expectations and abstracts away from some wild swings in recent years), real wage growth is hovering around its pre-recession level, say 1%, probably not too far from trend productivity growth.

A baseline expectation is that in a normal labor market, wage growth will be in the vicinity of real wage growth plus inflation (on average, headline and core inflation are very close over time). Assuming trend productivity remains constant near 1%, further labor market tightness should yield one of two outcomes – either real wages rise at the expense of profits margins or nominal wages and inflation rise in a lockstep pattern. The Fed would likely welcome the first outcome but would be unhappy with the second.

Looking forward, temporary help payrolls guide us to anticipate continuing overall job growth. It ain’t over yet – and that’s what keeps the Fed hiking until they get closer to their estimates of neutral policy.

Third, a little Fedspeak last Friday. Dallas Federal Reserve President Robert Kaplan said the job report confirms what I just said above. Via Fox Business:

“That tells me that over the next nine to 12 months, we ought to be raising the Fed fund rates probably at least three more times, maybe three to four times, to get to that neutral rate,” Kaplan said during an exclusive interview with FOX Business’ Edward Lawrence. “Everything that’s in this job report today just causes me to reaffirm that view.”

Kaplan doesn’t think trade concerns are materially impacting the economy yet and thus doesn’t provide a reason to pause in the near term. He also says that the fiscal stimulus will fade over the next two years and that he is watching for how demographic shifts expected to weigh on labor force growth will impact the economy over the next two years. Note that Kaplan has in the past stated his preference for a neutral-then-pause strategy.

Separately, Cleveland Federal Reserve President Loretta Mester described the jobs report as strong and justifying continued gradual rate hikes to push policy to a neutral level (see Bloomberg here). She adds that the economy has more “underlying momentum” than she believed in June. Watch for the impact of stronger growth on the “dots.” While we are all looking for the pause, maybe some of the Fed anticipates more rate hikes than currently expected.

Chicago Federal Reserve President Charles Evans released a speech originally prepared for his cancelled appearance in Argentina (never waste good copy!). After describing the economy and policy as returning to something more normal, the dove turns to a hawk:

Given the outlook today, I believe this will entail moving policy first toward a neutral setting and then likely a bit beyond neutral to help transition the economy onto a long-run sustainable growth path with inflation at our symmetric 2 percent target.

Yep, this is what the models are telling them to do. This will be the crux of the debate next year as the models demand more tightening. What I find most interesting is the adherence to these models even though, as Evans says, they will sustain the economy in the zone where the zero lower bound is likely to be an issue once again. One would think the Fed would continue to adjust policy accordingly in a dovish direction but increasingly is looks like many policymakers intend to 1.) fall back on old models and 2.) accept the likelihood of a return to the zero bound and be ready to use unconventional policy as needed. That strikes me as hawkish – the Fed said policy normalization is underway, and they mean it.

Bottom Line: Expect the rate hikes to keep coming. No reason to pause this year. In some sense, expecting a pause even after policy rates hit neutral is more hope than anything else.