Federal Reserve Governor Lael Brainard delivered a clear message in her latest speech: The way things are going, the rate hikes are not going to stop anytime soon. In fact, you should be happy that we haven’t accelerated the pace of hikes. As I said earlier this week, the “pause” story is more about hope than reality. We can’t talk pause until we detect a significant change in the tone of the data.

The theme of Brainard’s speech is an explanation of the neutral policy rate with an eye toward policy implications. It is tempting to say that market participants are the intended audience. I sense this is too narrow. I think this is also a message for her colleagues at the regional banks who argue for a pause at neutral. She is telling them they don’t understand what neutral means. Or at least they need to be more careful about its meaning.

So what does neutral mean? Brainard:

Intuitively, I think of the nominal neutral interest rate as the level of the federal funds rate that keeps output growing around its potential rate in an environment of full employment and stable inflation.

Right – this would be a standard definition. But Brainard wants to emphasize the difference between the short- and the long-runs. First:

Focusing first on the “shorter-run” neutral rate, this does not stay fixed, but rather fluctuates along with important changes in economic conditions…In many circumstances, monetary policy can help keep the economy on its sustainable path at full employment by adjusting the policy rate to reflect movements in the shorter-run neutral rate. In this context, the appropriate reference for assessing the stance of monetary policy is the gap between the policy rate and the nominal shorter-run neutral rate.

Read that carefully. Brainard says that at a full employment economy (like now), the shorter-run neutral rate is the relevant indicator for determining the level of accommodation provided by a particular policy stance. By extension, in the current situation, the longer-run rate is not the relevant metric. In other words, policy might still be accommodative even when pegged at the longer-run neutral rate. Don’t look at the longer-run SEP rate estimates to assess the current policy stance.

We all know the estimates of the longer run rate, 2.5-3.5% as reported in the SEP. So what is the shorter-run neutral rate? Back to Brainard:

Turning to the shorter-run neutral rate, although the estimates are model dependent and uncertain, we can make some general inferences about its recent evolution that are largely independent of the details of specific models. Estimates suggest the shorter-run neutral rate tends to be cyclical, falling in recessions and rising during expansions, and our current expansion appears to be no exception.

Take a moment and appreciate Brainard’s intelligence and foresight. She doesn’t provide a number or even a range. Why not? She has estimates. She just said so. Brainard wisely does not provide that estimate because she knows we will lock onto that number and will not let go. She doesn’t want to lay down that marker because she knows it can change all too easily.

Brainard doesn’t give you a number, but she still gives guidance. That guidance is all about the data:

Last year, the unemployment rate returned to pre-crisis levels, which required real interest rates that were below zero for nearly 10 years. This year, the unemployment rate has fallen further, and job market gains have gathered strength, at the same time that the federal funds rate has increased. This combination suggests that the short-run neutral interest rate likely has also increased. If, instead, the neutral rate had remained constant as the federal funds rate increased, we would have expected to see labor market gains slow. That inference is consistent with the formal model estimates, which indicate that the shorter-run neutral rate has gone up as the expansion has advanced. This is also suggested by the observation that overall financial conditions, as measured by a variety of indexes, have remained quite accommodative during a period when the federal funds rate has been moving higher.

The Fed has been raising interest rates, but that “tightening” has yet to be felt in the economy. Au contraire, the job market has strengthen in recent months and financial conditions remain loose. So it must be that the short-run neutral rate has risen – and arguably risen more than policy rates, which would account for the stronger job market. This, by the way, is what I think the Fed should be doing – talking less about the neutral rate estimates and more about the data. It’s the future of forward guidance.

With some guidelines on the kinds of data we should be looking at, Brainard shift to a discussion of the outlook. It’s an optimistic forecast: “…it seems likely that growth will remain solid.” And while she also shows some mild optimism that there remains room for addition improvement in labor markets, Brainard is clearly concerned about the stability of the inflation outlook:

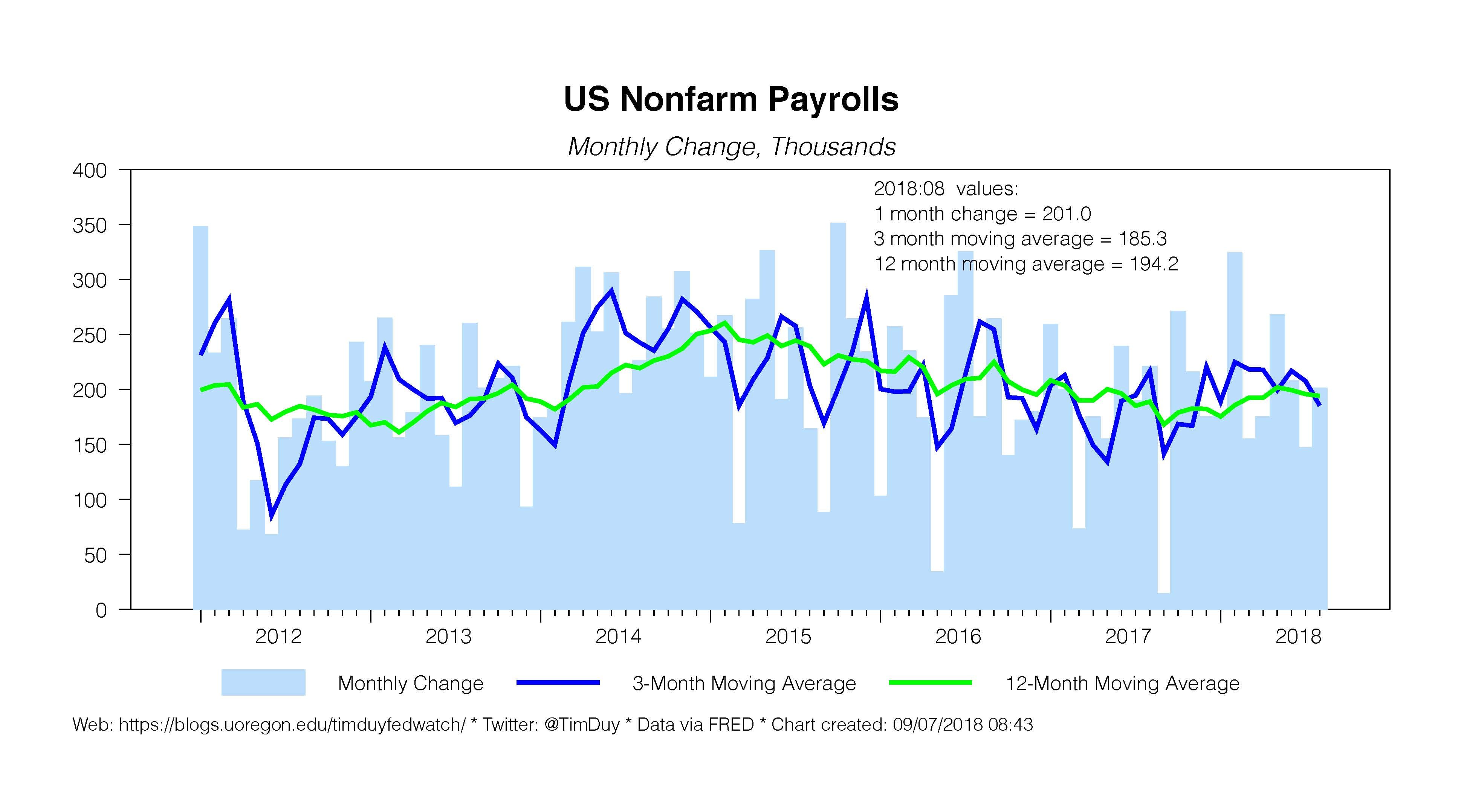

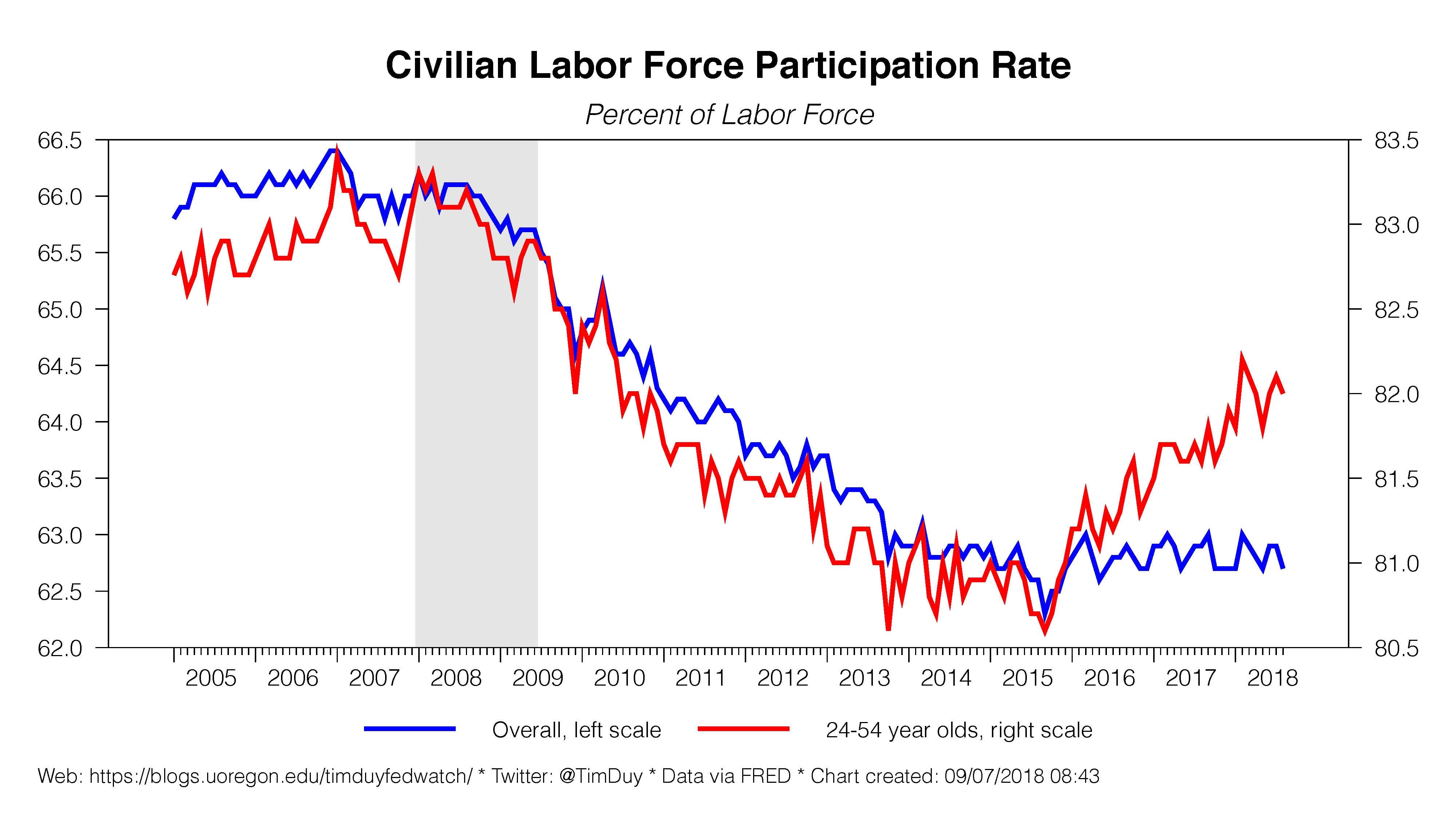

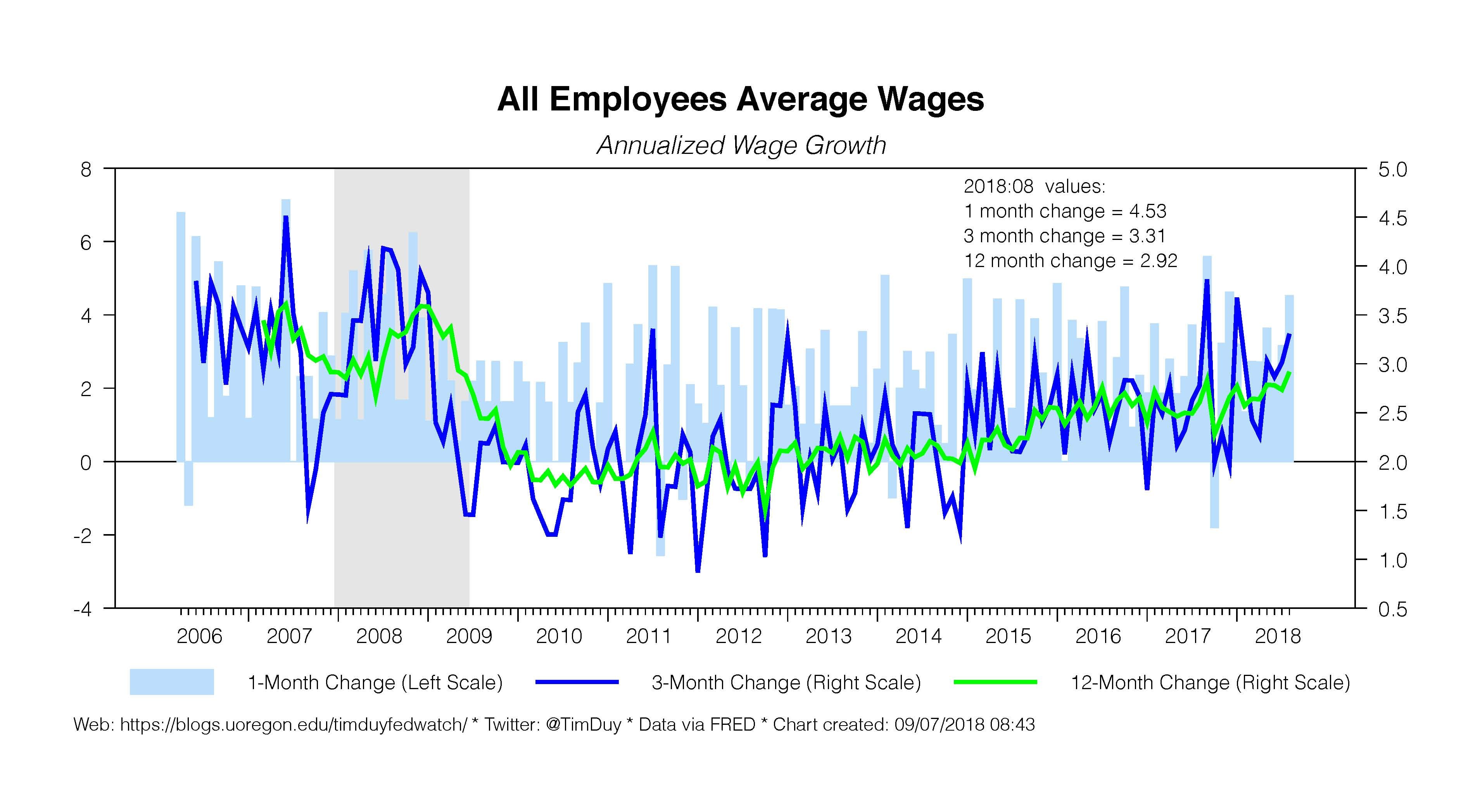

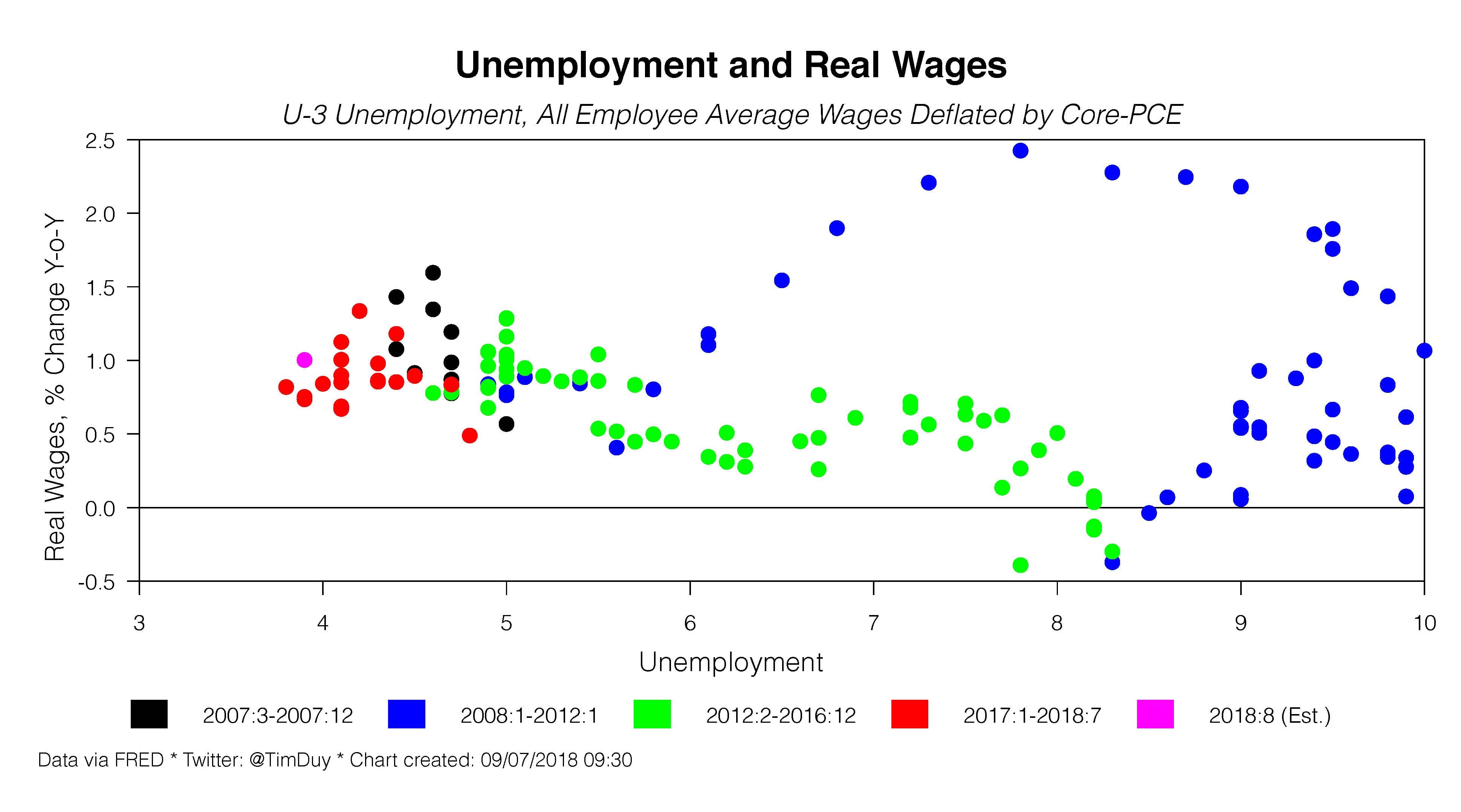

At 3.9 percent, the August unemployment rate was about 1/2 percentage point lower than the previous year. If unemployment continues to decline at the same rate as we have seen over the past year, we will soon see unemployment rates not seen since the 1960s. Historically, the few periods when resource utilization has been at similarly tight levels have tended to see elevated risks of either accelerating inflation or financial imbalances…So far, the data on inflation remain encouraging, providing little signal of an outbreak of inflation to the upside, on the one hand, and some reassurance that underlying trend inflation may be moving closer to 2 percent, on the other…The past few times unemployment fell to levels as low as those projected over the next year, signs of overheating showed up in financial-sector imbalances rather than in accelerating inflation. The Federal Reserve’s assessment suggests that financial vulnerabilities are building, which might be expected after a long period of economic expansion and very low interest rates.

She apparently takes little relief from the stable inflation numbers to date, instead fearing a reprise of inflation or financial instability episodes of the past. And arguably the latter are currently the more relevant concern! What that means for policy is that the rate hikes keep coming:

Over the next year or two, barring unexpected developments, continued gradual increases in the federal funds rate are likely to be appropriate to sustain full employment and inflation near its objective. With government stimulus in the pipeline providing tailwinds to demand over the next two years, it appears reasonable to expect the shorter-run neutral rate to rise somewhat higher than the longer-run neutral rate. Further out, the policy path will depend on how the economy evolves.

No reason to pause at the longer-run neutral rate because that will not be shorter-run neutral. So what about all those Fed regional presidents talking about pausing at the longer-run neutral rate? Maybe we shouldn’t be paying too much attention to them.

Brainard repeats her yield curve story. The summary is that yes, she is aware of the historical implications of the yield curve, but this time is different so it is not an impediment to raising rates. Brainard also throws in the obligatory “data dependence” caveat, but it is clearly biased in a hawkish direction:

While the information available to us today suggests that a gradual path is appropriate, we would not hesitate to act decisively if circumstances were to change. If, for example, underlying inflation were to move abruptly and unexpectedly higher, it might be appropriate to depart from the gradual path. Stable inflation expectations is one of the key achievements of central banks in the past several decades, and we would defend it vigorously.

As I keep saying, the Fed is going to pick recession over inflation. That isn’t changing.

Bottom Line: The rate hikes are going to keep coming until it becomes more evident that growth will ease to what the Fed believes is a more sustainable pace. Don’t count on an automatic pause as rates approach 3%. And don’t expect the Fed to care about the yield curve if the data continues along its recent path.