Click for newsletter version!

The April employment report lent further support to the Fed’s gradual approach to rate policy. There is little reason to doubt that central bankers will hike rates at their June meeting while indicating more will be coming in the second half of the year. The report deepened the mystery of low wage growth, putting the Fed in the familiar place of again being overly pessimistic with regards to the unemployment forecast. Meanwhile, central bankers continue to signal they will allow inflation to overshoot their target.

{kind=link}

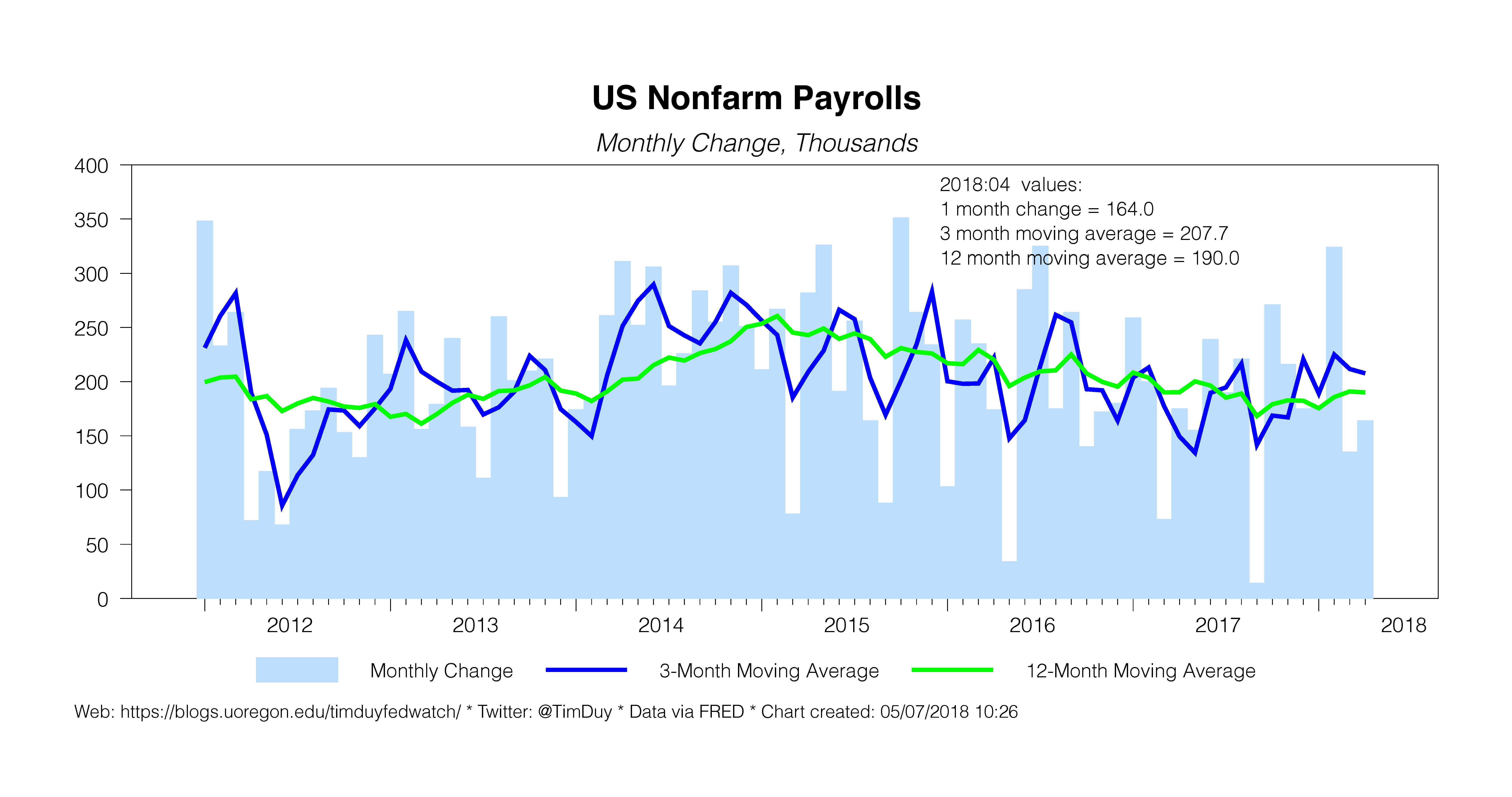

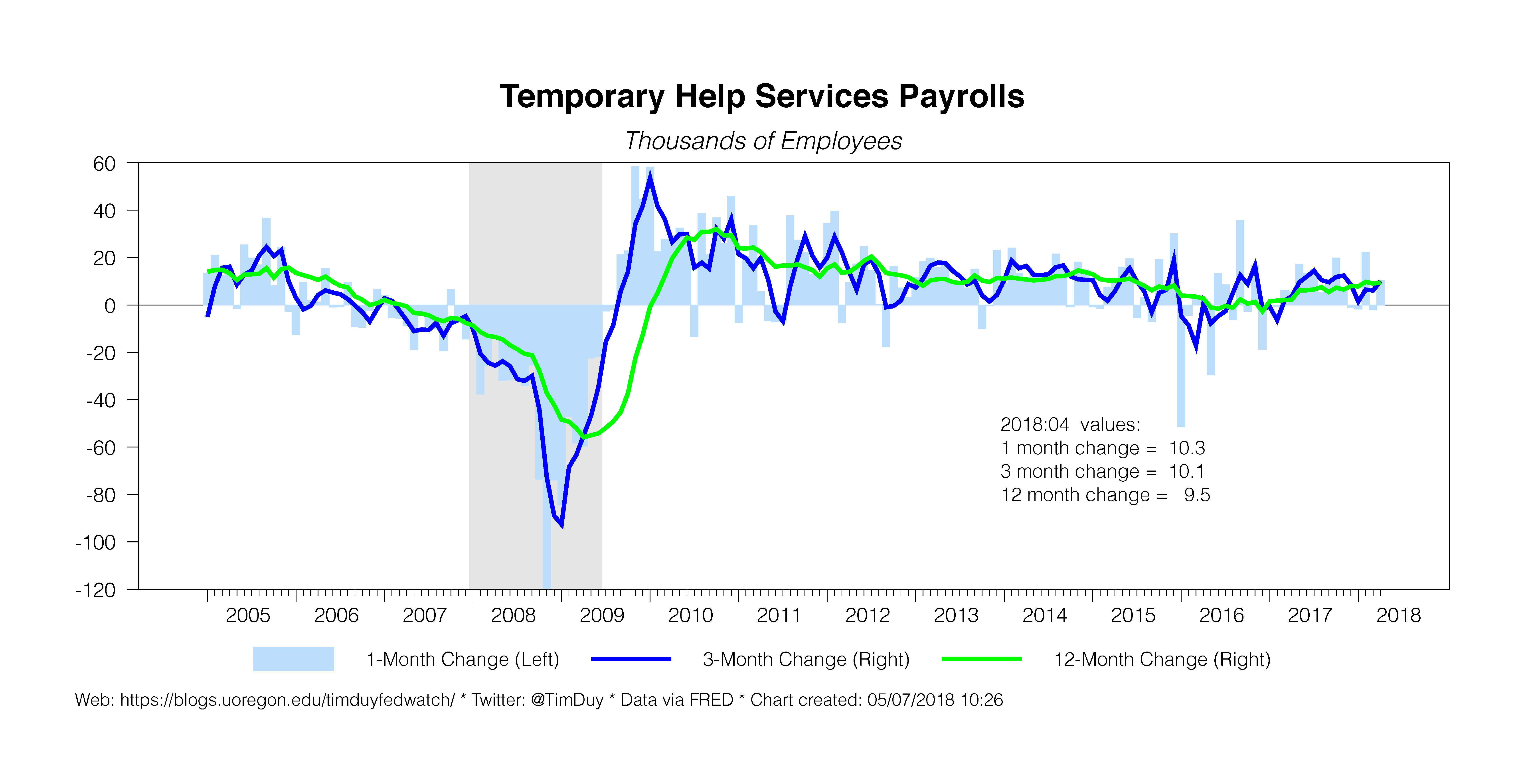

Nonfarm payrolls grew a below-consensus forecast 164k in April while the previous two months were revised up by 30k. The twelve-month pace is holding just below 200k and solid growth in temporary help numbers suggest these numbers are sustainable going forward.

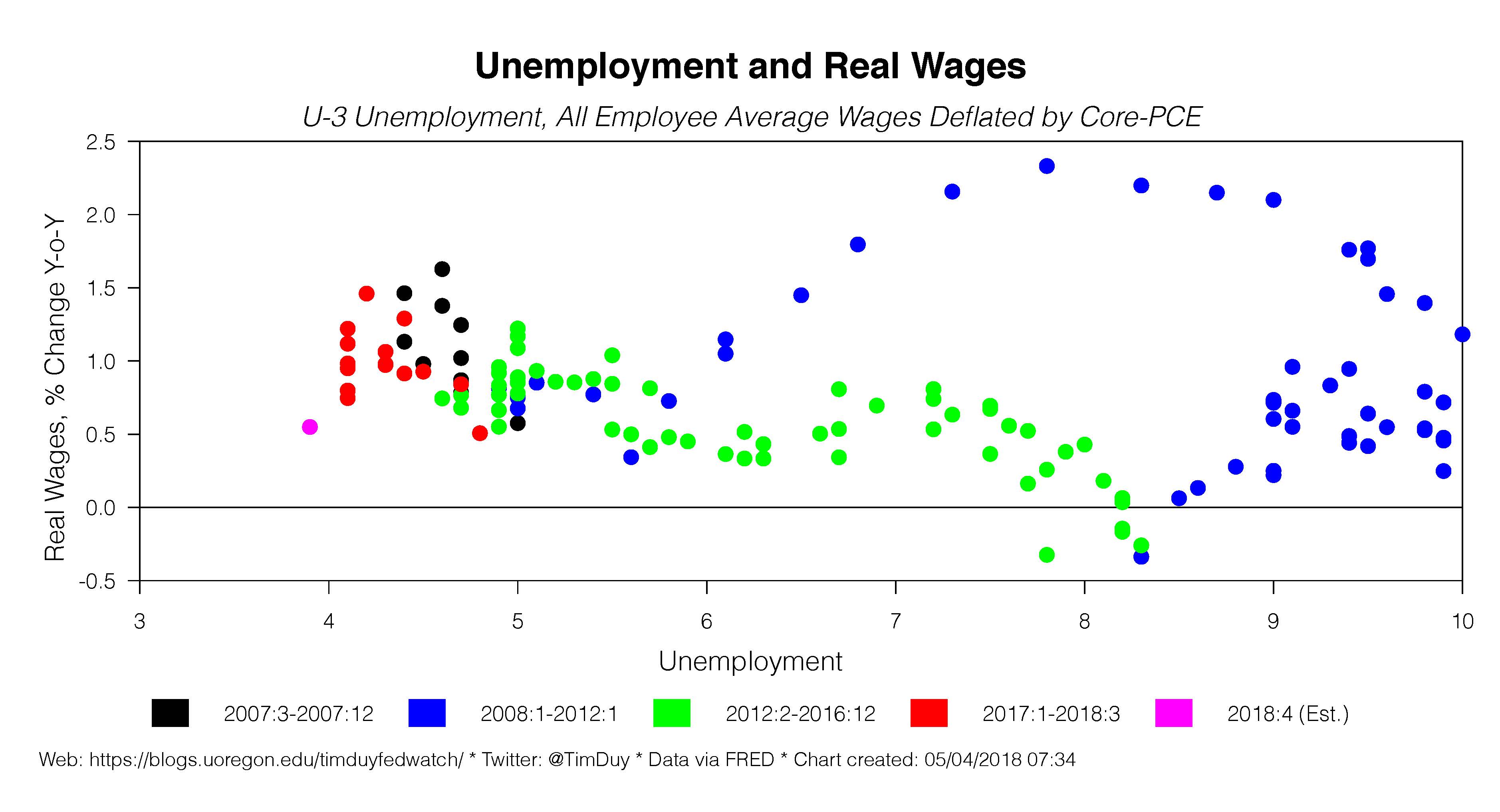

The pace of job growth finally caught up to the unemployment rate. After months at 4.1 percent, the unemployment rate dropped to 3.9 percent, a level last seen in December 2000. The Fed was not expecting to see 3.9 percent until the end of this year; with the overall economy looking sufficiently strong to sustain this pace of job growth, they will almost certainly edged down their unemployment rate forecasts at the next FOMC meeting.

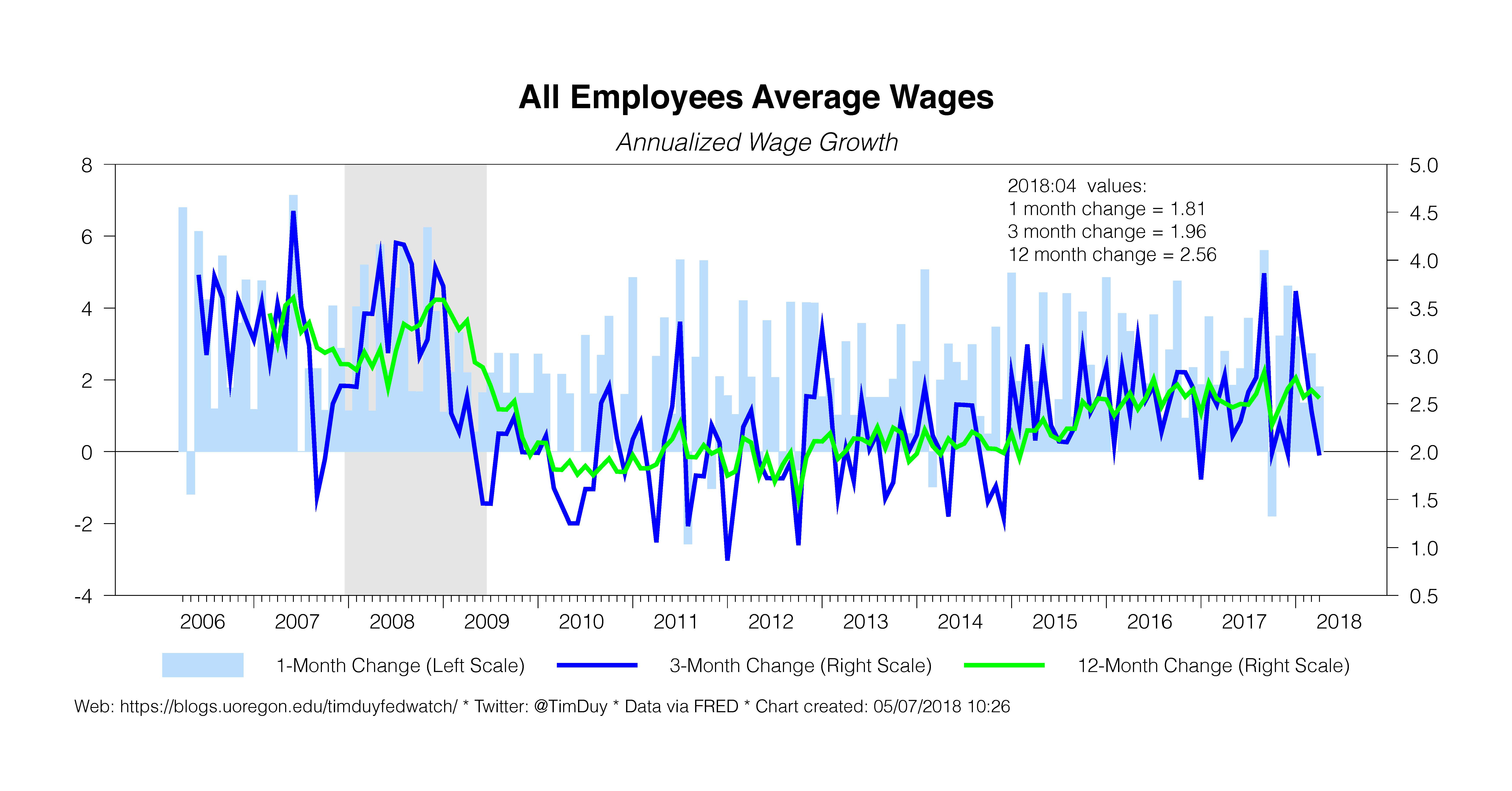

Even though unemployment pierced the 4 percent mark, wage growth continues to disappoint. The monthly gain annualize was just 1.8 percent, while the change from a year ago was 2.6 percent. With inflation rising back to the Fed’s 2 percent target, these numbers suggest real wage growth is decelerating. This strikes me as unsustainable in the face of already low and still falling unemployment rates. Consequently, I anticipate wage growth will tick up higher in the months ahead.

Still, just enough wage growth to match the combination of inflation and productivity growth, let’s say a combined 3 percent, doesn’t suggest the economy is overheating. By extension, the economy thus has not yet pushed past full employment. The Fed’s estimate of a 4.5 percent natural rate of unemployment thus still seems too high and likely to fall in line with downward revisions to the unemployment rate forecast next month. Alternatively, they can hold the longer run natural rate estimate steady with the explanation that it is temporarily depressed. Or they can hold the natural rate estimate steady and raise interest rate projections accordingly.

My current thinking is that they will not look to raise rate projections again just yet. They need to see stronger wage growth to confirm the economy is operating above full employment and to see such overheating reflected in higher inflation. And not just a few basis points of higher inflation, but something significantly more. Via Bloomberg, Atlanta Federal Reserve President Raphael Bostic told reporters:

“We’re fluctuating around the 2 percent target. I am comfortable with that. To the extent we have seen some upward pressure, we don’t have the ability to stop trends on a dime. Some overshoot is fine.’’

This will be the dominant thinking among central bankers for the time being. I think they will be comfortable allowing their near-term inflation forecasts drift higher if need be – up to as high as 2.5 percent even – if those forecasts revert back to target over the medium run under current rate projections. This gives also will give them quite a bit of leeway to accept lower unemployment. Given the flat Phillips curve, even very low unemployment doesn’t generate inflation worth getting upset about.

Bottom Line: Assuming the current path of activity continues and that the Phillip’s curve remains flat and doesn’t have a “hockey stick” moment, I expect the Fed to remain on kind of autopilot. They will tolerate modest overshooting of inflation and instead focus on their forecasts. Those forecasts suggest that the path of expected tightening will suffice to return inflation to target over the medium term. They need to see genuine threats to that forecast before deviating to a new policy path. They will likely raise rates once a quarter until the yield curve flattens out. At that point, policy becomes more complicated – especially if the lagged impact of monetary policy has yet to show up in slower economic activity.