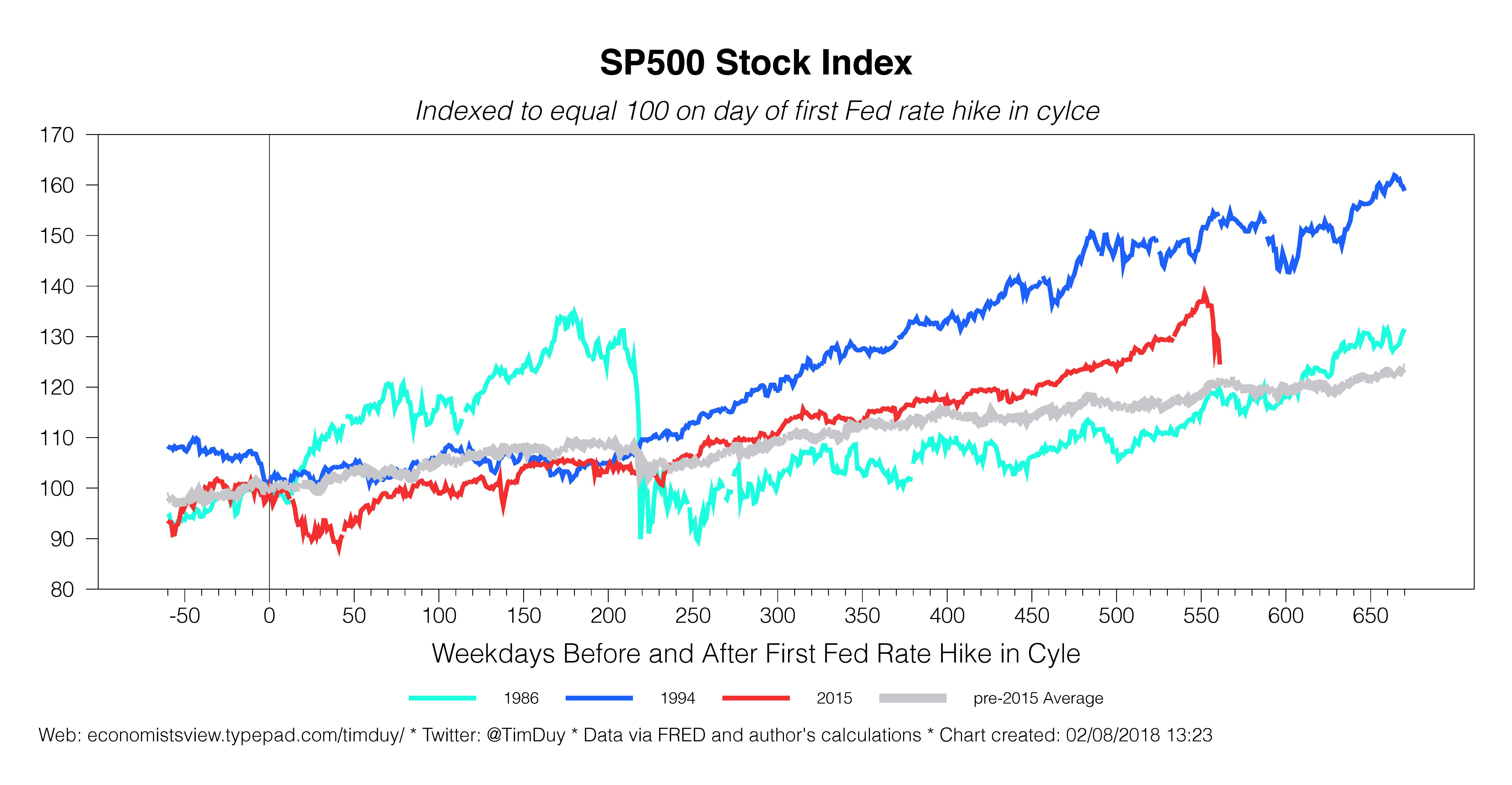

The equity market resumed its slide on Thursday, taking the Dow and S&P500 down by 4.2% and 3.8%, respectively. Since the downturn in equities began, Fed officials have largely stuck to the party line – more rate hikes are coming. This should not come as a surprise. The magnitude of the declines still falls well short of that necessary to induce the Fed to change course, especially in the context of the recent pace of gains. That means that until losses deepen, market participants are on their own.

Continued here as a newsletter…

My baseline interpretation of recent events: The US economic expansion not only continues unabated, but is currently riding a cyclical upturn. The momentum from that upturn looks to continue long enough for the Federal Reserve to realize its policy rate forecast for 2018 – and into 2019 as well. This message began to sink in last fall, showing up, for example, in a steady rise in 2 year yields. The reality of the situation set in more deeply after the solid January employment report with its surprise wage gain.

That alone should have been enough to encourage market participants to see that the economy was in some sense “normalizing” as the scars of the financial crisis healed, allowing the Fed to continue to raise interest rates. Adding to this environment is a tax cut and now a spending bill that look to widen the structural US deficit. Fiscal policy is thus set to add further fuel for an economy that is arguably already pushing up against full employment. The prospect of an overheated economy tilts the odds in favor an even more aggressive monetary policy stance.

In short, interest rates needed to adjust to this new outlook. Note that this has long been built into the Fed’s forecasts, which assumed that neutral rates would rise as the financial crisis moved further into the rearview mirror. This appears to be what is happening.

In the meantime, equity prices continued to rise relentlessly – the pace clearly had a frothy feel to it. A correction was likely to occur, and I argue that the sooner it occurred, the better off we will be in the long run. The employment report seemed to be the trigger for that correction.

Recent price action between bonds and equities suggests to me that market participants are incorporating all of this information and in the process grinding out a new equilibrium that takes longer-term interest rates up a notch and equity prices down a notch. This makes sense to me in the context of an economy that has shifted into a mature phase. As the US economy moves closer to full employment, the constellation of prices in the economy will shift. Wall Street is a place where that shift happens.

Within the context of this adjustment, however, lies a signal extraction problem. It is difficult to differentiate between a readjustment of pricing and a crash. Hence, there is a tendency to step aside until the dust settles. That tendency tends to exacerbate market turmoil. It takes some time for this kind of thing to sort itself out.

In the meantime, monetary policy makers appear to believe that they have already solved the signal extraction problem. St. Louis Federal Reserve President James Bullard called this “the most predicted selloff of all time.” New York Federal Reserve President William Dudley – the man of “more” or “less” compelling fame, also sees the turmoil as a nonevent:

“This wasn’t that big a bump in the equity market,” Dudley said at a moderated question-and-answer session in New York on Wednesday. “The stock market had a remarkable rise over a very long time with extremely low volatility,” he said, adding: “My outlook hasn’t changed just because the stock market’s a little bit lower than it was a few days ago. It’s still up sharply from where it was a year ago.”

Dallas Federal Reserve President Robert Kaplan described the volatility as possibly a “healthy thing.” San Francisco Federal Reserve President John Williams reiterated his position on the economy:

I am optimistic about the economy, but I expect continued moderate growth, with no Herculean leap forward. So given that the economy’s performing almost exactly as expected, you can expect policymakers to do the same.

He added:

For the moment, I don’t see signs of an economy going into overdrive or a bubble about to burst, so I have not adjusted my views of appropriate monetary policy. So my message to those concerned about a knee-jerk reaction from the Fed is that, as always, we’ll keep our focus on the dual mandate and let the data guide our decisions.

This is clearly intended to tamp down fears that the Fed will suddenly accelerate the pace of rate hikes. While I think the risk is weighted towards more than three hikes this year, I also think that such a policy shift requires some real change in the medium-term forecast. Changes in the near-term forecast did not affect the path of policy last year. The same seems likely to be the same this year. And if anything, the market turmoil enforces the current forecast and reduces the risk of a fourth hike.

Bottom Line: After many months of calm, we are now experiencing a painful readjustment. I think that pain is likely to continue until we sort out a new set of prices in the economy. The Federal Reserve looks set to allow that adjustment to continue unimpeded. They even seem to have expected the adjustment. For now, central bankers expect to maintain a gradual pace of rate hikes; it will take a much deeper correction – or evidence the correction to date is sufficient to trigger systemic damage in the financial markets – before they alter that that plan.