It’s worth reiterating this point I made yesterday:

Given the long lead times, we can pretty much guarantee that we are not yet at the peak of this cycle and hence incoming data will likely remain solid albeit not spectacular. The same good data flow could help prop up equities until the recession comes closer into view. The upshot is that an inverted yield curve does not mean a recession is right on top of us.

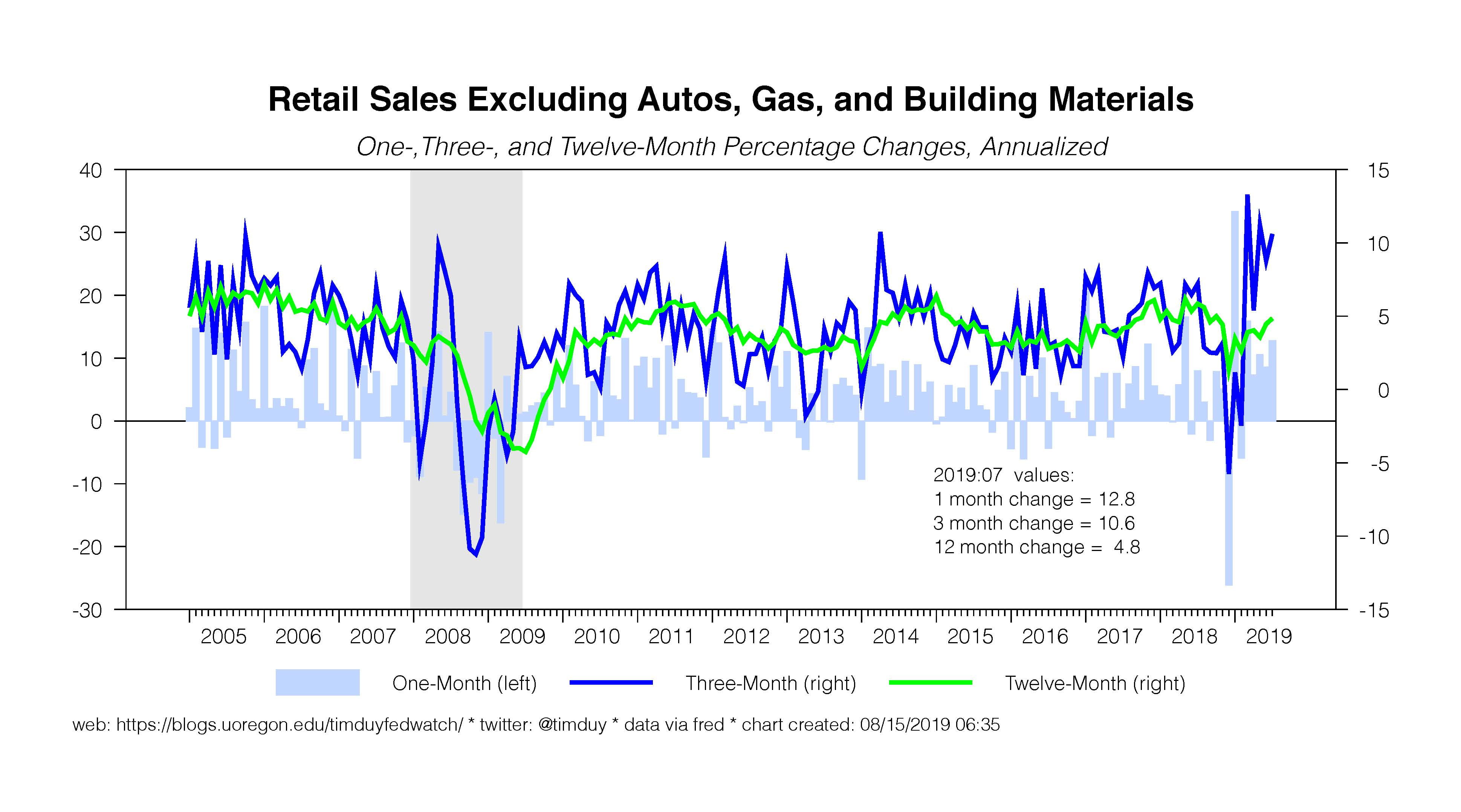

Today’s data is a perfect example of this point. Retail sales came in above expectation, proving once again the foolishness of betting against the US consumer:

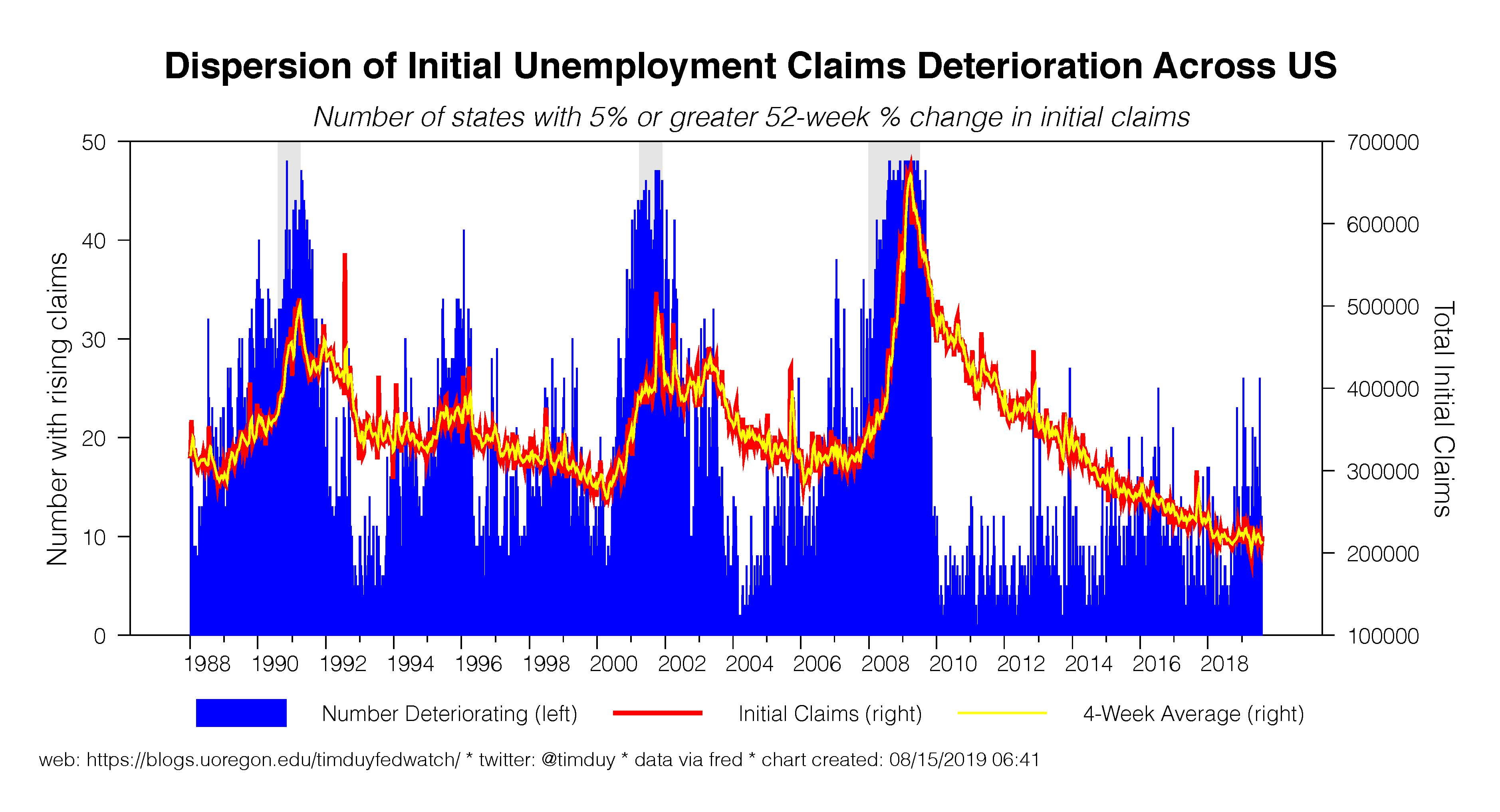

and initial jobless claims remain low:

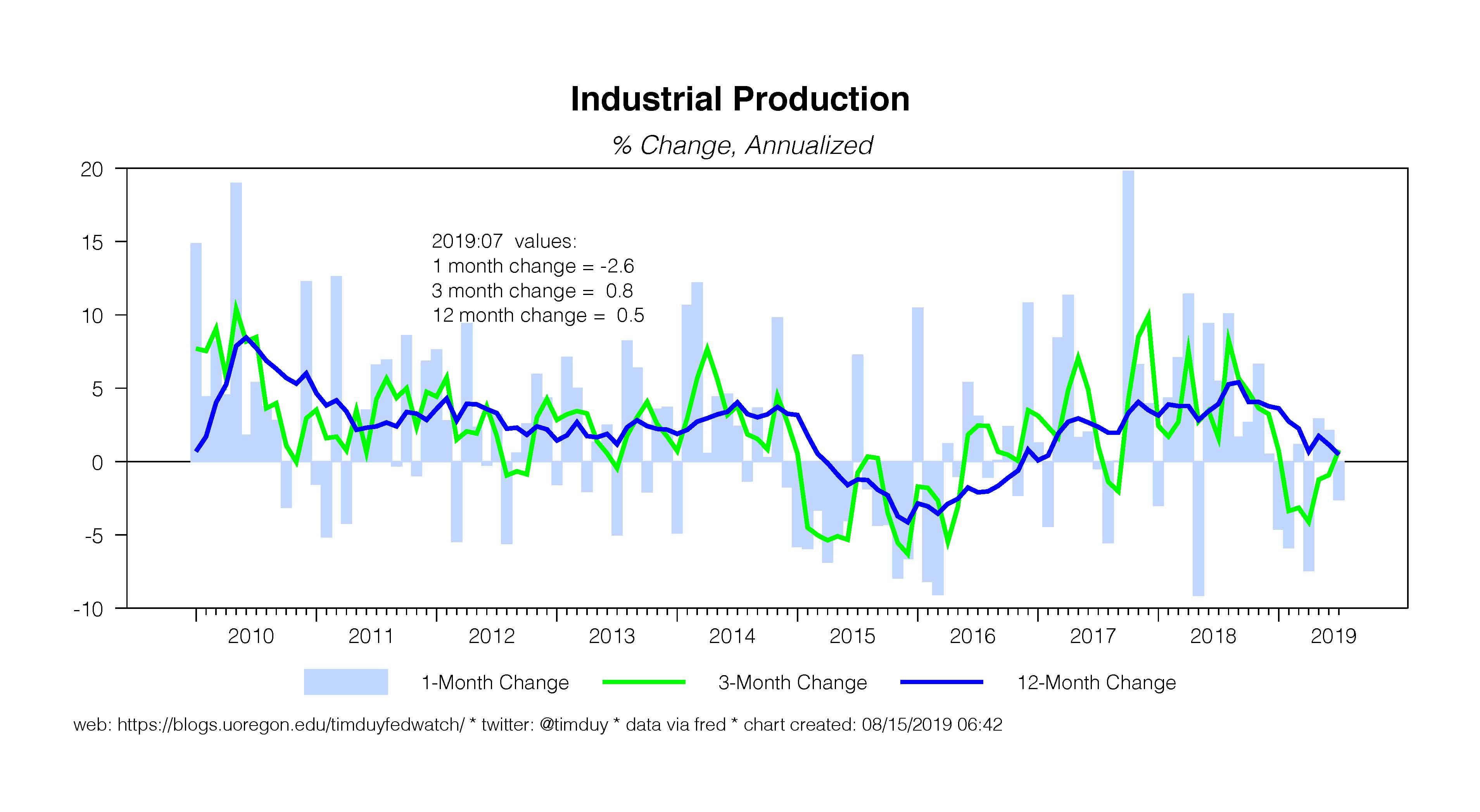

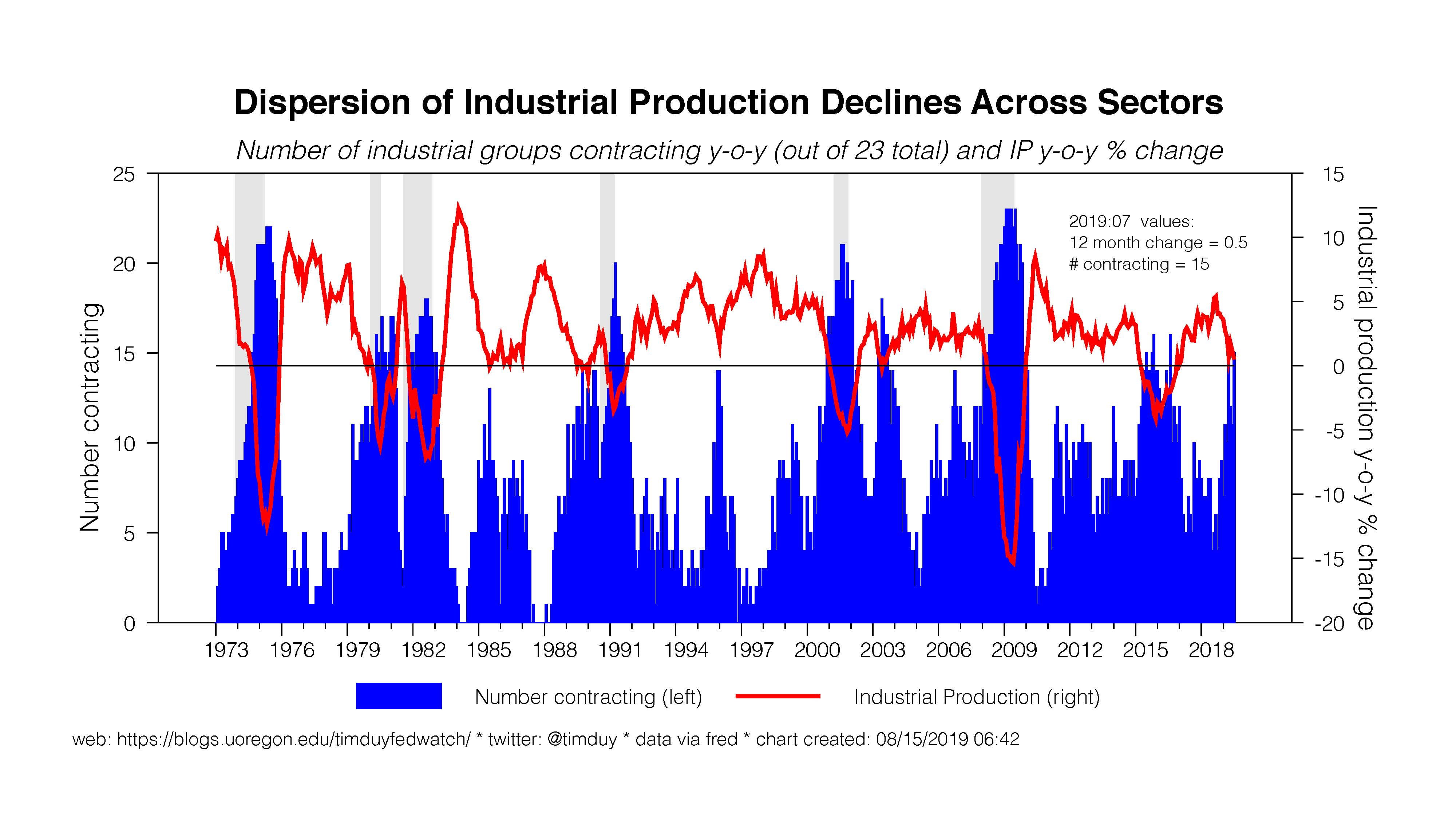

Until the job numbers turn in force, households will keep spending. Yes, manufacturing is on the weak side:

But this is completely expected and so far is mimicking the behavior of 2015-16 much more so than what you might expect in a recession. Moreover, while both the Empire and and Philadelphia business surveys came in well-above expectations, suggesting that the threats to manufacturing may be overstated. Also, I think we are learning that manufacturing might not be the signal it once was as the sector becomes a smaller share of the economy.

A generally positive tone to the data should not be unexpected; the inversion of the yield curve was never going to signal an immediate deterioration in the data flow. It is exactly that lag between signal and recession that has traditionally kept the Fed biased toward tightening after the yield curve inverts. This time the behavior of the Fed is very different. Time will tell if this means the Fed effectively kills the yield curve as a recession indicator.

Bottom Line: It remains too early to see a recession in the data. It’s reasonable to worry about the pessimistic signal from the yield curve but even if it does foreshadow recession, a recession call now is likely still too early.