I am still catching up from Spring Break. First, from my Bloomberg piece this week:

The turmoil in equities continued this week with the S&P 500 Index down about 10 percent from its record high in January. Although the sell-off implies tighter financial conditions, don’t expect the Federal Reserve to change course yet.

Central bankers will need more evidence that Wall Street’s problems threaten to spill over onto Main Street before they abandon plans for further interest-rate increases. Friday’s employment report is more important for the path of rates than recent financial market action.

With this in mind, the consensus for this employment report is a nonfarm payroll gain of 175k (compared to 313k in February), a slight decline in the unemployment rate to 4.0 percent, and a 2.7 percent y-o-y rise in wages compared to last year. Numbers along these lines would be generally consistent with the Federal Reserve’s forecast, which anticipates that continuing solid job growth will push the unemployment rate down to 3.9 percent this year and 3.6 percent next year. Hence, an employment report meeting the market expectation implies the Fed will remain on course to hike rates three or four times this year (recall that the median rate forecast for 2018 is for three hikes, but the bulk of FOMC participants are split between three and four hikes; four should be our baseline at this point).

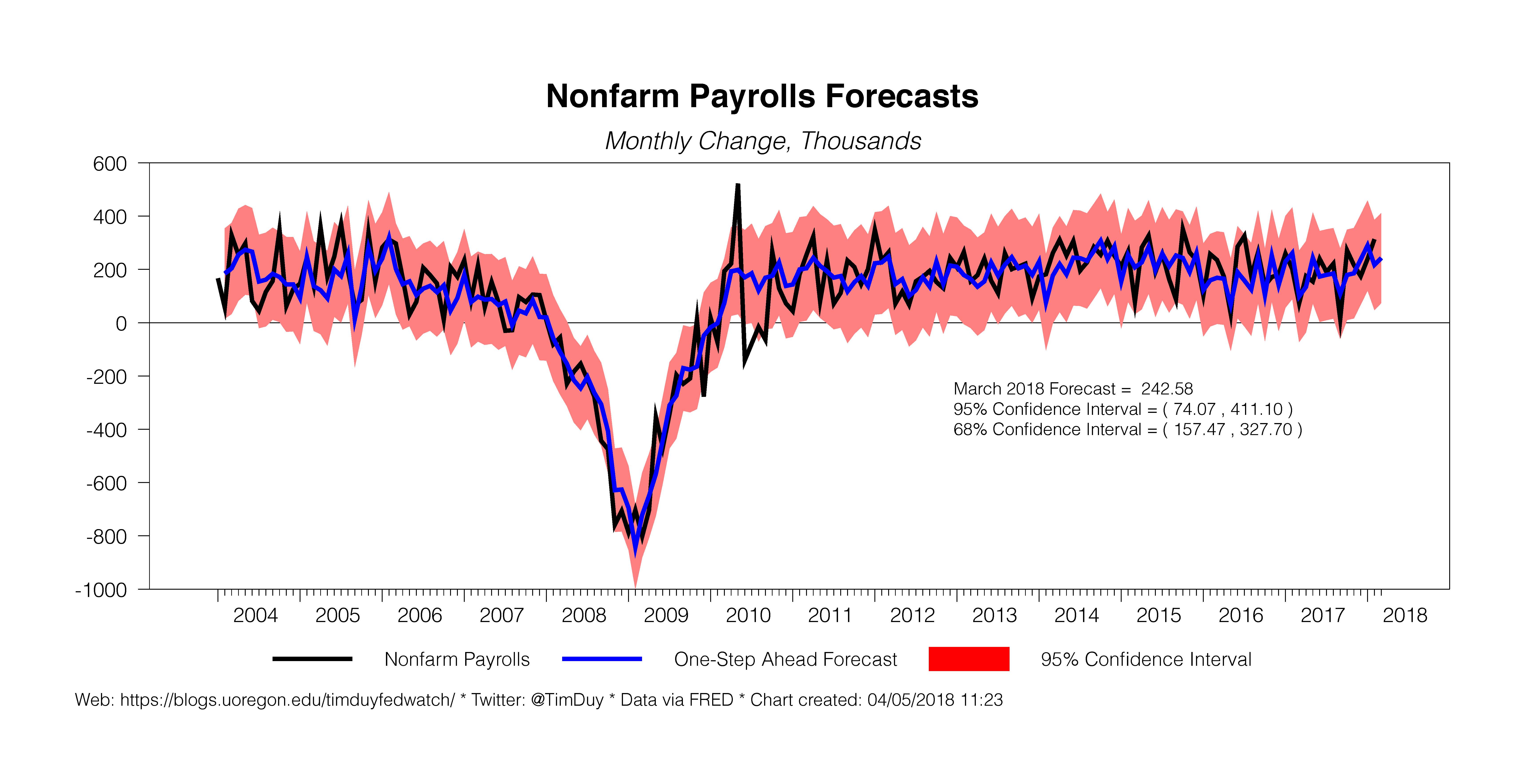

Interestingly, strong ISM employment components and ADP’s estimate of private payrolls, combined with low unemployment claims, leads my model to an above consensus forecast of a 243k gain:

This seems high to me given that the February number experienced a death-related boost; recall also significant March reversals in 2017 and 2015. We should be prepared for the possibility of a sharp downward miss on payrolls. Still, given concerns about headwinds changing to tailwinds when the economy sits near full employment, the Fed will be more sensitive to a stronger than anticipated report than the alternative. A weak number on payrolls would be written off as payback from February.

Importantly, look for signs that the economy has pushed beyond full employment; a stronger than expected wage number would suggest the Fed’s estimate of longer-run unemployment is close to accurate. It wouldn’t necessarily push the Fed to accelerate the pace of rate hikes – the link between wages and inflation is not so straightforward – but would suggest the risk to the forecast is tilted toward more (or sooner) hikes than anticipated.

Finally, the path of monetary may clear further after Federal Reserve Chairman Jerome Powell’s speech Friday. I am hoping for more frequent discussions on the economy from Governors in general and the Chairman in particular than we have had in recent years.

And while we wait, here is a picture of Zion National Park I took while on Spring Break: