The jobs report gives the Fed cover to retain a gradual rate path. To be sure, the rapid pace of job growth will leave them nervous about an unsustainable pace of growth. But the flat unemployment rate remains consistent with their forecasts. In addition, low wage growth indicates the economy has not pushed past full employment. If inflation remains constrained, the Fed would be pretty much on target for this year. That suggests the three-hike scenario should remain in play. But increased confidence in the outlook and risk management concerns will push up enough “dots” in the next Summary of Economic projections toward four hikes for this year.

Continued here as a newsletter…

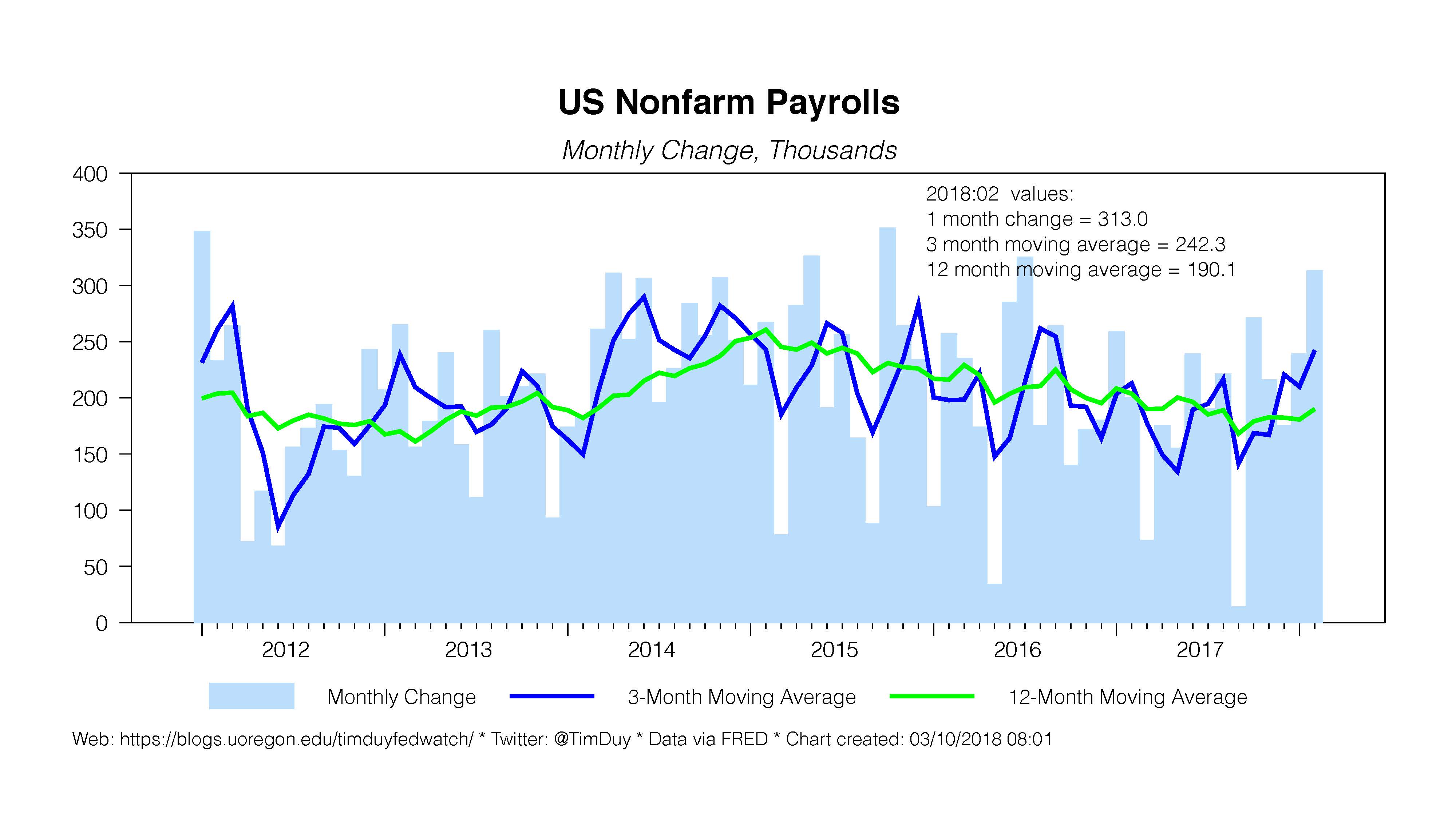

Nonfarm payrolls grew by in February while previous months were revised upwardly. The three-month moving average is 242k while the twelve-month average is 190k. These are solid numbers for an economy this deep into an economic expansion, the result of the acceleration of activity over the past year. Job gains continue to exceed the rate at which central bankers believe will eventually be the rate of labor force growth when secular factors dominate cyclical behavior. That time, however, continues to be postponed. The unemployment rate held steady again at 4.1 percent; my concerns that unemployment would soon shift downward continue to be just concerns and not reality. Instead, growth in prime-age labor force participation continues to support overall labor force participation. If this trend continues, then we would expect that the unemployment rate will generally track in line with the Fed’s forecast despite growth well in excess of long-run potential growth.

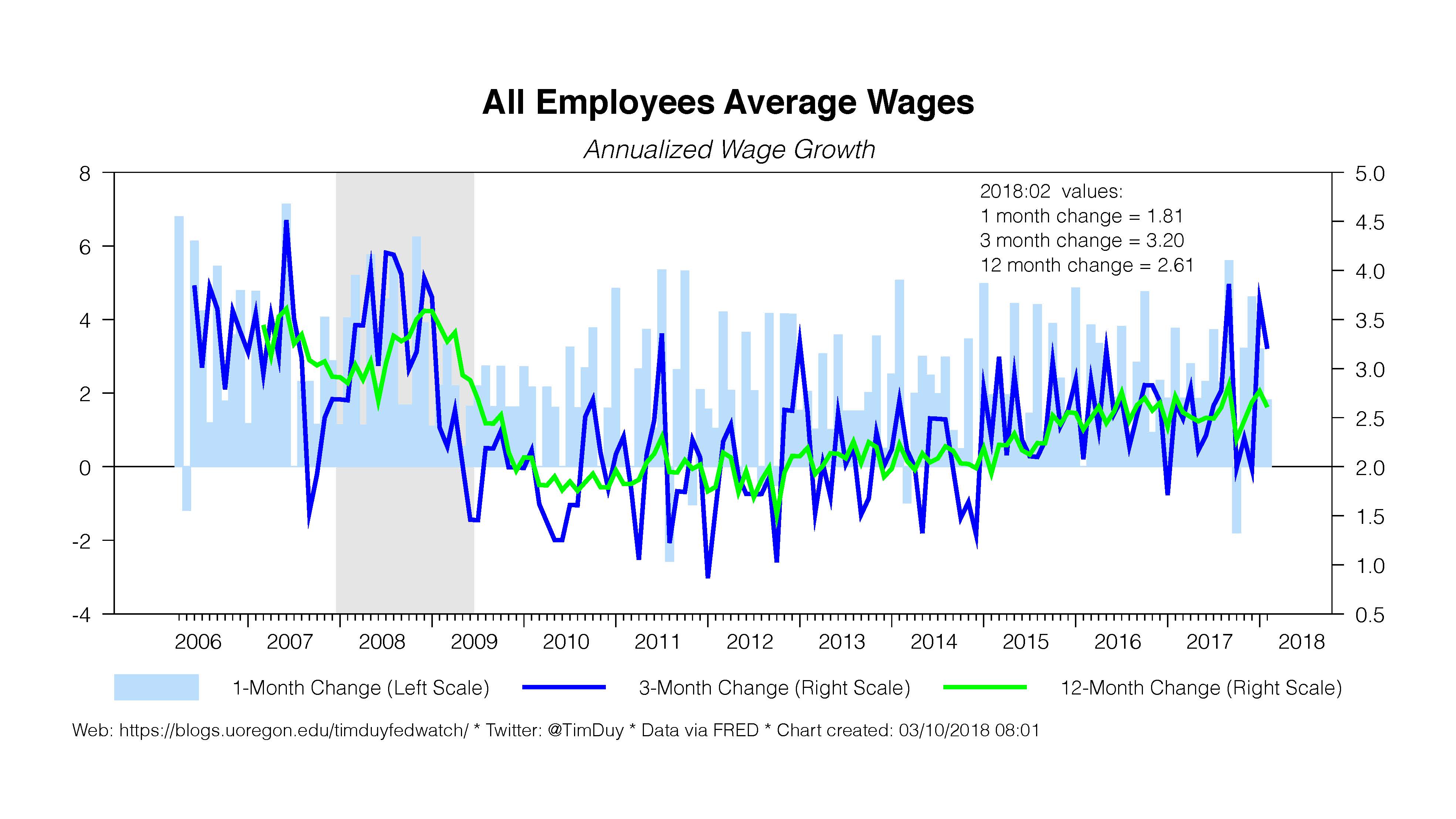

Job gains continue to exceed the rate at which central bankers believe will eventually be the rate of labor force growth when secular factors dominate cyclical behavior. That time, however, continues to be postponed. The unemployment rate held steady again at 4.1 percent; my concerns that unemployment would soon shift downward continue to be just concerns and not reality. Instead, growth in prime-age labor force participation continues to support overall labor force participation. If this trend continues, then we would expect that the unemployment rate will generally track in line with the Fed’s forecast despite growth well in excess of long-run potential growth. More generally, the recovery of prime-age participation (alone with still relatively high levels of other underemployment indicators) suggests that the economy can sustain further cyclical gains without overheating. In other words, the economy might be quite a bit farther from full-employment than indicated by Federal Reserve estimates of the longer-run unemployment rate. Weak wage growth also argues against the full-employment hypothesis. Wage growth decelerated in February, quelling hopes for a more sustained acceleration.

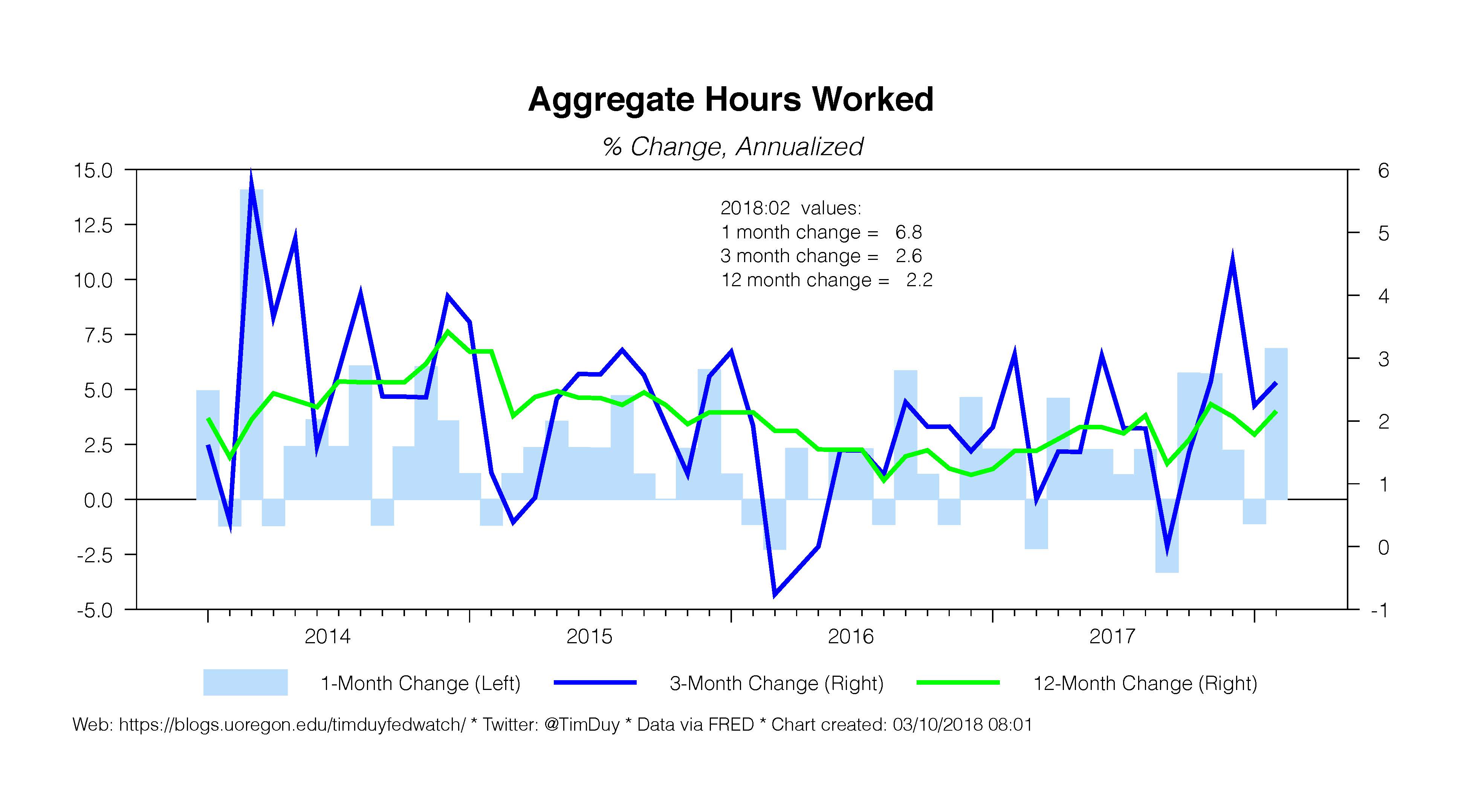

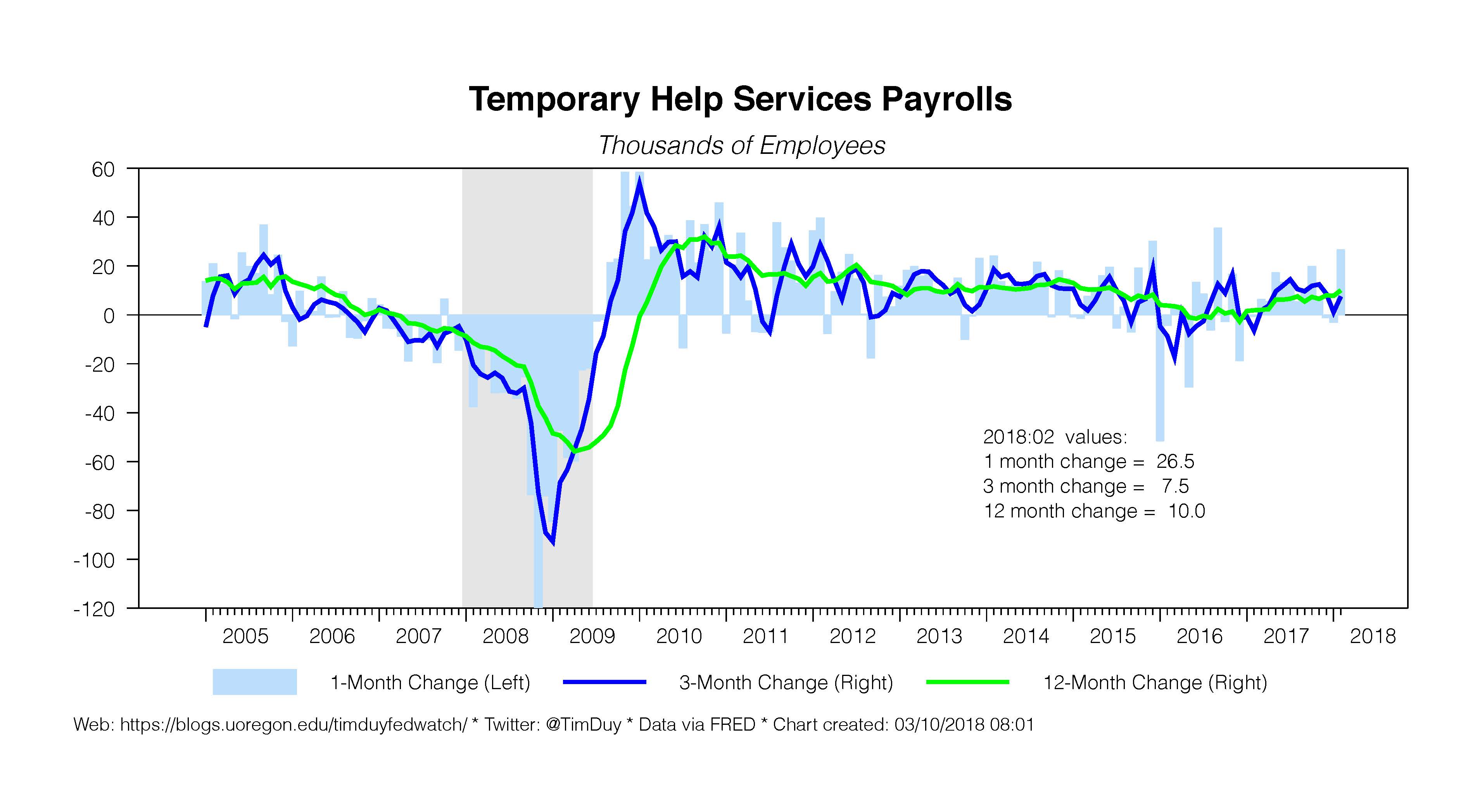

More generally, the recovery of prime-age participation (alone with still relatively high levels of other underemployment indicators) suggests that the economy can sustain further cyclical gains without overheating. In other words, the economy might be quite a bit farther from full-employment than indicated by Federal Reserve estimates of the longer-run unemployment rate. Weak wage growth also argues against the full-employment hypothesis. Wage growth decelerated in February, quelling hopes for a more sustained acceleration. Although wage growth decelerated, hours worked jumped, which will help support overall compensation and provide a base for continued consumer spending. In addition, a jump in temporary help payrolls indicates this labor market isn’t about to hit a wall anytime soon.

Although wage growth decelerated, hours worked jumped, which will help support overall compensation and provide a base for continued consumer spending. In addition, a jump in temporary help payrolls indicates this labor market isn’t about to hit a wall anytime soon.

The Federal Reserve should be comforted by this report as it argues in favor of the gradual rate hike approach. If labor supply is responding positively to a higher pace of economic activity, the Fed should worry less about overheating despite the solid pace of wage growth. Moreover, continued tepid wage growth should weigh down on their estimates of full-employment. This report simply doesn’t indicate that the natural rate of unemployment is as high as the Fed believes.

This report should, like recent inflation numbers, reassure the Fed of its 2018 forecasts. That will induce those policymakers most skeptical of the inflation outlook to revise their below-consensus rate estimates higher, bumping up the lower dots. In addition, with their forecasts looking likely to hold, those at or above consensus would be expected to hold their estimates steady. There will, however, be upward pressure to rate even those dots.

Risk management concerns will drive the upward pressure on rate projections. The Fed tends to believe the economy has more likely than not achieved or surpassed full employment (regardless of that pesky wage, inflation, and labor force participation data). They also see headwinds changing to tailwinds that threaten to sustain stronger growth for longer than expected that pushes the economy deeper into a danger zone in 2019 and 2020. Finally, the last two cycles left central bankers wary that a hot-economy will reveal itself in financial instability rather than inflation. All together that suggests they will want to project a slightly tighter policy and be prepared to move more aggressively if needed. This will reveal itself in the next Summary of Economic Projections.

Bottom Line: Recent employment reports combine to tell a story of an economy that can sustain a faster pace of growth without pushing past capacity boundaries. That argues for leaving the Fed’s expected policy rate path intact. But Federal Reserve Chairman Jerome Powell’s testimony pointed to “avoiding overheating” as a policy objective while Federal Reserve Govenror Lael Brainard discussed at length the shift of economic forces from headwinds to tailwinds. She drew a comparison to 2015-16, when the Fed sharply reduced the pace of hikes relative to the projected rate path. Together, these discussions suggest the Fed sees a shifting balance of risks to the outlook. They will try to manage the risks accordingly, bumping up estimates of future rates while leaving open the option to switch to a more sharply more aggressive path if needed.