As anticipated, the Fed left rates unchanged at the conclusion of yesterday’s FOMC meeting. The statement was little changed but the handful of revisions point to continuing rate hikes. The Fed remains on track for three 25bp rate hikes in 2018. For the most part, the turnover at the Fed combined with ongoing solid data has left the remaining doves sidelined. The low inflation warnings of last year were largely a head fake as the Fed was always positioned to continue raising rates as long as there looked to be continuing downward pressure on unemployment.

Continued here as a newsletter…

The FOMC statement was largely unchanged compared to December. The Fed dropped the hurricane references as they were no longer relevant for the outlook. The Fed revealed additional confidence in the inflation outlook by dropping the reference to low near-term inflation in place of an expectation that inflation will rise this year. The firming of recent inflation numbers likely influenced this change although it was evident in the Fed’s forecast from December.

Risks remain roughly balanced; they did not delete the “roughly.” They are still watching inflation developments, but note that this can cut both ways. Last year it arguably reflected the influence of doves worried about low inflation. Now it could be interpreted as the influence of hawks worried about high inflation. In either case, the Fed remains data dependent.

More curious was the addition of the word “further.” As in:

The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong.

It would be nice to have had a press conference to see if there was any significance to this change. In my view, the reason for this change was to dissuade anyone from thinking the Fed was done hiking rates.

Arguably then you can say this statement is more consistent with the message of the SEP than the last statement. The message of the December SEP was that inflation will climb in 2018 and so too will rates. The December statement was arguably a bit mushy on both points. The January statement thus clarifies the likely path of policy.

So maybe we should read the January statement as an effort to make the statement more consistent with the forecast? And that this was easier to accomplish with some of the more dovish voices rotating off as voting members? Something to get some clarity on in the coming weeks.

In other news, the Fed also updated its “Statement on Longer-Run Goals and Monetary Policy Strategy.” The notable change was the Fed’s estimate of longer-run unemployment fell from 4.8 percent to 4.6 percent. This change makes the statement consistent with the December SEP. I sense a theme here. A bigger takeaway is that the Fed continues to show flexibility in revising their estimates of longer-run unemployment in response to tepid wage growth.

Oh, the FOMC also selected incoming Federal Reserve Chair Jerome Powell to be the chair of the FOMC. But you kind of saw that coming.

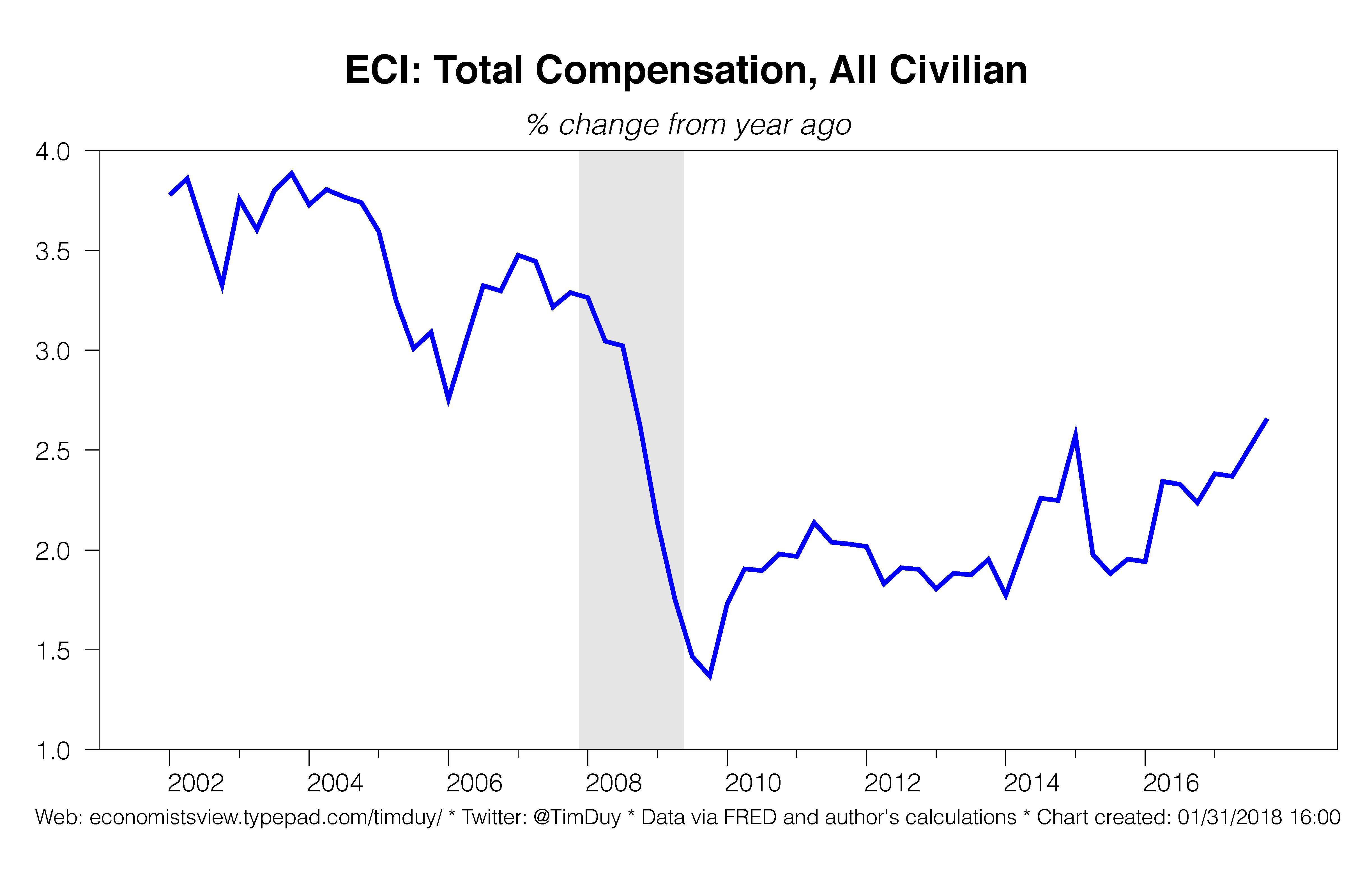

Meanwhile, we still have plenty of data coming up as the week winds down. Today the BLS released the Employment Cost Index for the final quarter of 2017. Total compensation costs for civilian workers was up just 2.6 percent compared to a year earlier. The direction of gains remains up, but the magnitude remains tepid. There is no reason here to believe that labor costs are rising at a rate suggestive that the economy has breached capacity constraints. That argues for continued policy gradualism.

Note that to the extent firms face rising labor costs, they may become increasingly interested in expanding or relocating in lower cost regions. This is another mechanism firms can control costs and keep an lid on inflation. See Pandora for example.

ADP reported private sector job growth of 234k for January. This may induce some upward revisions to consensus estimate – currently a 175k payrolls gain – for Friday’s employment report. (Although that bet didn’t work out too well for the December report). Of course, the current consensus, if realized, would already be sufficient to keep downward pressure on the unemployment rate. The Fed thinks they need to get to something closer to 100k to guide the economy to a sustainable place. I don’t see a reason to think we are getting there anytime soon, and that will keep pressure on central bankers to raise rates.

Bottom Line: The Fed is set to hike rates in March. I continue to believe that the hawkish tilt of the FOMC should entrench forecasts of three rate hikes in 2018 and that it is premature to conclude four or more. I don’t see reason yet to think the Fed is about to conclude they are behind the curve if they retain the current projected policy path.